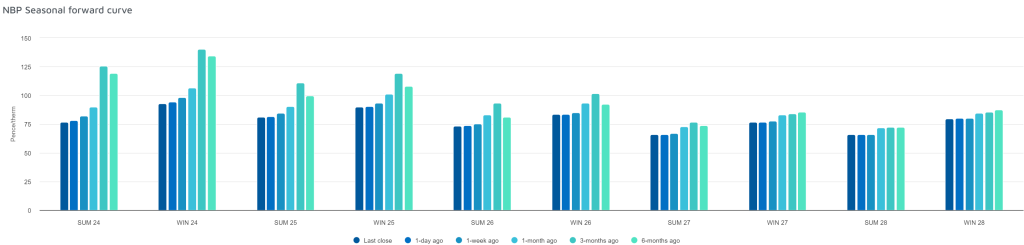

Seasonal Forwards are down on the Day/Week/Month/3-Months/6-Months (see chart).

Markets opened down across the board this morning despite a short system (demand outstripping supply).

Down the curve, bearish pressure persists against a backdrop of historically high storage for the time of year, Norwegian flows at capacity, more than sufficient LNG send-out and arrivals, and favourable temperature forecasts for the end of January.

Of course, market participants continue to eye Middle East tensions warily, but key drivers remain overwhemingly bearish.

On the supply side, the Dutch have re-engaged the Groningen gas fields following last year’s closure in anticpation of colder temperatures in NW Europe over the coming weeks.

In short, markets remain soft – with clients increasingly opting make the most of the unexpected opportunity to secure improving values for the front two seasons (when compared to what was on offer during the summer months!)

Monthly Day-ahead averages are on target this month to achieve 81p/therm (or 2.75p/kwh).

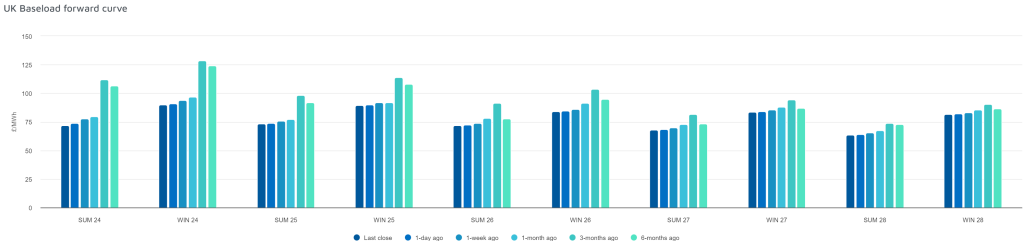

ELECTRICITY & CARBON ALLOWANCES

Seasonal Forwards are down on the Day/Week/Month/3-Months/6-Months (see chart).

Looking to the continent, European short-term delivery saw little change yesterday (or today) – temperatures, wind outputs and nuclear availability are marginally up on the week.

Down the curve, electricity and carbon prices continued to slowly ease (alongside the gas) as weather forecasts were (once again) revised to be milder and windier by the end of January – eclipsing any support we’ve seen from the cold, still conditions over the past week or so.

Consensus is building amongst market participants that prices are likely to go lower – given the muted reaction from bulls to recent wintry drivers.

Both speculators and Industrials are net short carbon according to the COT (Commitment of Traders Report) – if the sell-off picks up momentum, we could see a retest of the lows posted 8th Dec ’23.

Back in the UK, our generation mix at the time of writing is 59% gas-for-power; 29% renewables; and 10% low carbon (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £79/mwh (or 7.9p/kwh).