Markets have traded sideways today – it would be fair to say key drivers are well-balanced.

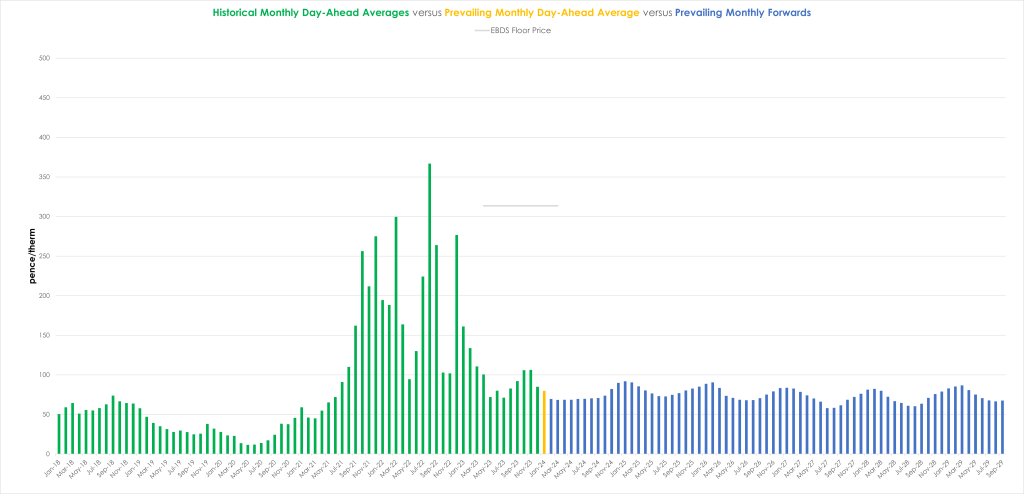

Notably, this month’s Day-Ahead average (so far) is at a significant premium to the remaining monthly Forwards of Winter-23, and those of Summer-24 (see chart).

Again, it would be fair to claim that monthly Forwards reflect market participant’s belief that the remainder of Winter-23 should pass without a hitch…

Norwegian flows remain at capacity and LNG arrivals are in rude health – offsetting any inevitable storage withdrawals.

Whilst it’s freezing right now, conditions are expected to warm up by the weekend.

Consensus is building that Europe will reach the end of Winter-23 with still over 50% of storage left in the tank.

Despite the cold spell, prices have remained under pressure given robust supply dynamics and historically high European storage levels.

By the weekend, warmer , wetter and windier conditions are likley to exert further bearish pressure with Summer-24 on the horizon.

Geo-political risk persists in the form of Middle East escalations and lingering worries over suppy disruption via the Red Sea.

Monthly Day-Ahead averages are on target this month to achieve 80p/therm (or 2.7p/kwh).

ELECTRICITY & CARBON ALLOWANCES

Looking to the continent for signals, short-term delivery electricity prices dived yesterday (alongside the gas and carbon markets) off the back of growing confidence that next week will bring wetter, warmer and windier conditions – limiting storage withdrawal and gas-for-power burn.

Whilst several Forward contracts are technically oversold, more downside is surely inevitable.

The likelihood of further downside is heightened if European demand remains subdued against a backdrop of improving renewables outputs.

Carbon is dropping off – pressured by the softening of the wider energy complex and speculators shorting the market.

Consensus is building that UKAs may go as low as £30/tonne next week.

Back in the UK, our generation mix is actually bullish at 53% fossil fuels (inc. 3% coal).

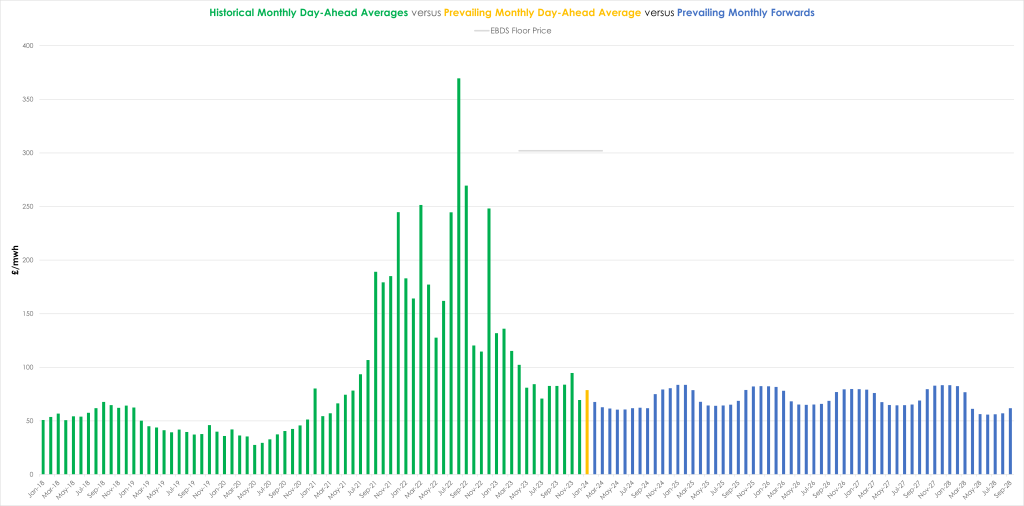

Monthly Day-Ahead averages are on target this month to achieve £79/mwh (or 7.9p/kwh).