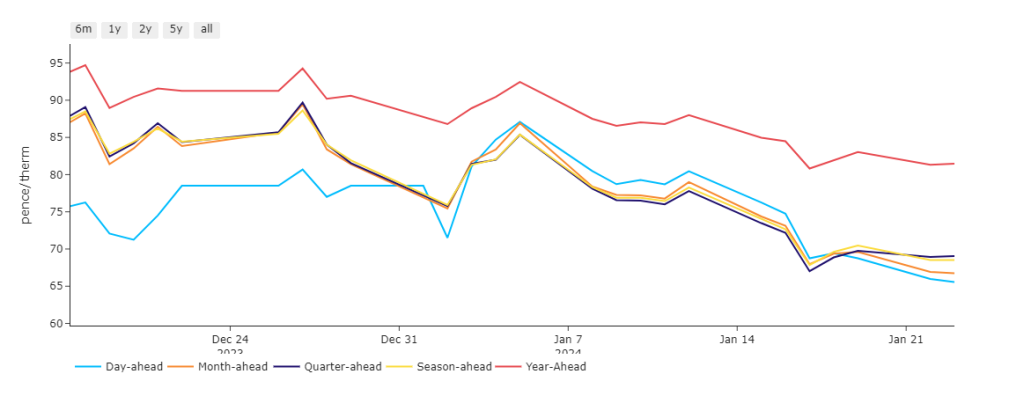

Notably, in-line with the onset of warmer/windier conditions, Day-Ahead prices have fallen back below Month/Quarter/Season-Ahead (see chart).

The divergence between short-term delivery and Year-Ahead is also growing more pronounced as we draw closer to summer conditioning.

Prices were up marginally at this morning’s open off the back of a slightly short system (demand outstripping supply) – though demand remains well below seasonal norms.

On the supply side, Norwegian flows have dropped off 7% and LNG sendout is a little below recent levels.

At the time of writing, near-term delivery contracts continue to drift northwards – most likely a natural correction of oversold conditions following days of bearish momentum.

Further down the curve, contracts are a little firmer this afternoon versus yesterday’s close.

Contributing factors (other than bears catching their breath) include Qatar delaying LNG exports to Europe in response to the risk to vessels traversing the Red Sea.

Monthly Day-Ahead averages are on target this month to achieve 77p/therm (or 2.6p/kwh).

ELECTRICITY & CARBON ALLOWANCES

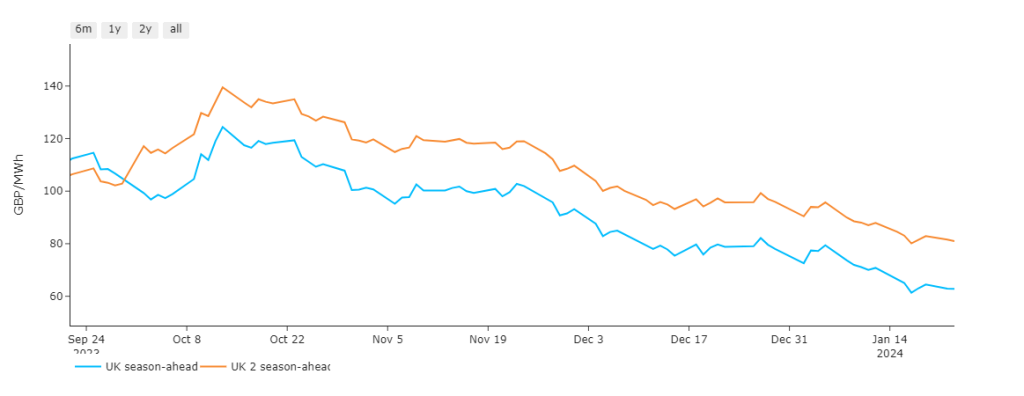

Season-Ahead and 2-Seasons-Ahead have fallen uniformly since mid-Oct ’23 – reflecting an orderly return to summer/winter price variances (see chart).

Looking to the continent, European near-term delivery prices fell yesterday off the back of higher renewable outputs/temperatures, but were partly offset by expectations of temporarily lower French nuclear availability.

Prices today are finding support in forecasts of falls in wind outputs/temperatures – though both drivers remain above seasonal norms.

Following recent falls, electricity markets are starting to feel rangebound/balanced.

With strong gas storage and nuclear availability, weather remains the key driver at the moment – so expect pronounced reactions from market participants should forecasts be subject to changes.

Following losses over the past three weeks, carbon markets exhibit risk of a short-squeeze, given the net short position of speculators according to the COT (Commitment of Traders Report).

A short squeeze occurs when price moves suddenly and sharply higher, forcing traders who hold a sell position to quickly buy to cover potential losses – and in so doing, causing a trend reversal.

Back in the UK, our generation mix is very bearish – 52% renewables and 19% gas-for-power burn.

Today’s UKAs (UK Carbon Allowances) achieved an auction settlement of £32.61/tonne.

Monthly Day-Ahead averages for UK electricity are on target this month to achieve £74/mwh (or 7.4p/kwh).