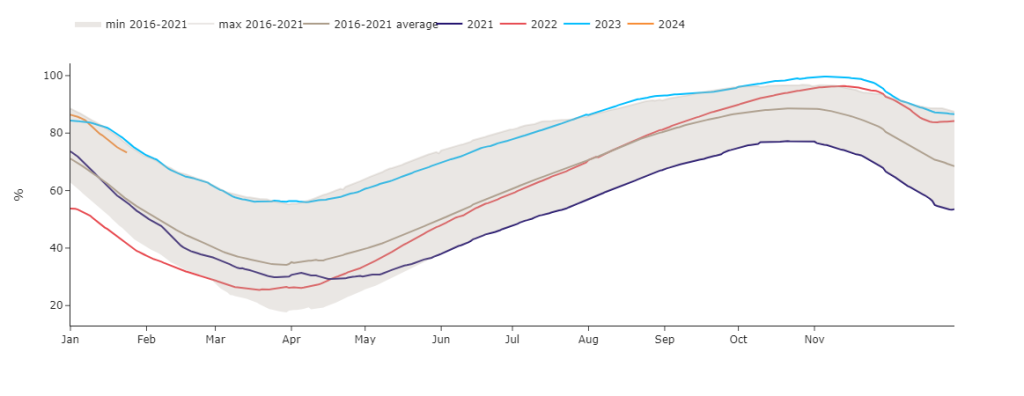

Notably, European storage remains toward the upper envelope of the 8-year range (see chart).

At this morning’s open, near-term delivery contracts are down off the back of high wind outputs (limiting withdrawals intended for gas-for-power burn).

Nonetheless, the UK gas system is still marginally short (demand outstripping supply) following unscheduled maintenance at Barrow terminal which has been extended until Sunday – with UKCS (UK Continental Shelf) flows consequently down 13%.

UK demand is, however, gradually falling with the onset of increasingly mild and windy weather (reducing heating demand).

Temperatures are likely to remain above seasonal norms for the coming weeks, sustaining bearish pressure (with the sharp-end of Winter-23 surely now in the rearview mirror).

Accordingly, Summer-24 prices are increasingly soft given expectations of high storage left in the tank at winter’s end.

Geo-political risk persists in the form of Middle East escalations and lingering worries over supply disruption in the Red Sea/Suez Canal (limiting downside).

Monthly Day-Ahead averages are on target this month to achieve 76p/therm (or 2.6p/kwh).

ELECTRICITY

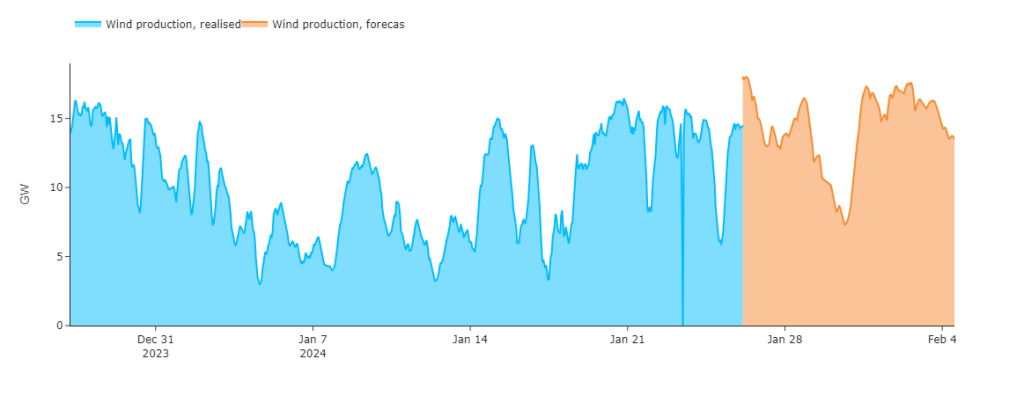

Our generation mix is very bearish with renewables at 63% and gas-for-power burn at 6%.

Wind outputs are strong and forecast to remain so until early Feb (see chart).

Looking to the continent, European near-term delivery dropped yesterday, weighed by forecasts of weaker demand and improving renewables outputs.

Improving French nuclear availability and temperatures across NW Europe around 6°C above seasonal norms early next week will likely keep markets under pressure.

Red Sea risk notwithstanding, market softness can be attributed to comfortable supply/demand dynamics – robust supply, high gas stocks and demand destruction.

UK electricity monthly Day-Ahead averages are on target this month to achieve £73/mwh (or 7.3p/kwh).