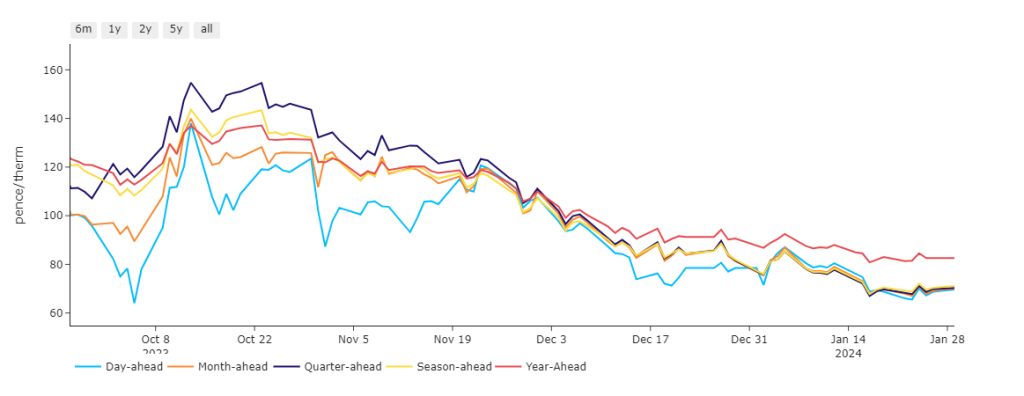

Day/Month/Quarter/Season-Ahead are at parity, and at circa. 15% discount versus Year-Ahead (see chart) – reflecting low short-term risk (favourable supply/demand dynamics) and higher risk in the mid-term (potential conflict/escalations/insecurity across the Middle East, Ukraine and Taiwan).

At this morning’s open, prices were marginally down versus yesterday’s close despite a short UK system (demand outstripping supply).

Nonetheless, demand is still running below seasonal norms with above average seasonal temperatures limiting heating demand, and wind outputs forecast to improve over the coming days (limiting gas-for-power burn).

Confidence in storage levels pervades underlying sentiment with consensus building that European storage will end Winter-23 with more than 50% still left in the tank.

The Freeport LNG terminal in Texas expects Train 3 to be out of service for about a month due to an electrical fault.

Train 3 has the capacity to produce about 0.7 billion cubic feet of LNG daily (equivalent to supplying around 5 million homes).

China’s property sector is starting to show signs of strain with Evergrande Group’s liquidation having been announced (raising further questions about China’s wider economy and associated demand).

Favourable weather conditions into early February are expected to keep a lid on any meaningful upside caused by geo-political risk across the Middle East.

Monthly Day-Ahead averages are on target this month to achieve 75p/therm (or 2.5p/kwh).

ELECTRICITY & CARBON ALLOWANCES

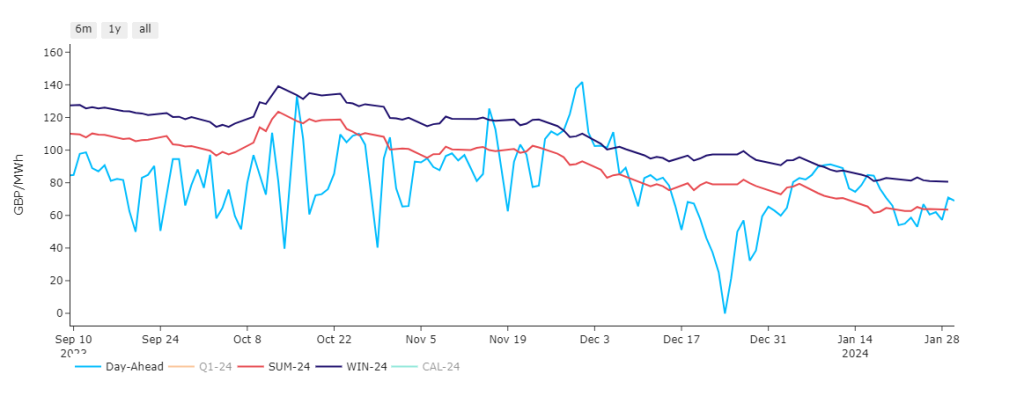

Day-Ahead is couched between Season/Ahead and 2-Seasons-Ahead (see chart) – reflecting a tight trading range, and prices at a steady equilibrium with Summer-24 now on the horizon.

Looking to the continent, near-term delivery prices are trading sideways with renewable generation forecast to gradually increase throughout the week.

A strong pressure gradient over Europe will bring south-westerly flows, enabling wind generation to get close to record levels at the beginning of next week.

French nuclear generation has been much higher than this time last year, allowing an easing of supply tensions – though due to outages, availability is forecast to drop over the coming weeks.

On the carbon market, market participants seem confident that a retest of €61/tonne is on the cards.

UKAs (UK mandatory carbon allowances) last year traded at an average discount of more than 40% to their European forerunner and counterpart (EUAs) – as such, market participants are asking for structural change to close the gap…

Back in the UK, our generation mix at the time of writing is increasingly neutral with 43% gas-for-power burn and 23% renewables.

UK electricity monthly Day-Ahead averages are on target this month to achieve £72/mwh (or 7.2p/kwh).