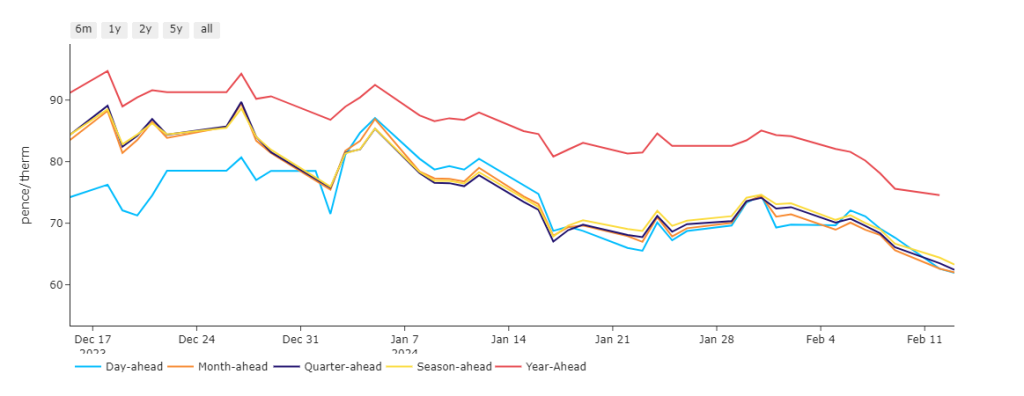

Notably, Day/Month/Quarter/Season-Ahead are at parity and at a 16% discount versus Year-Ahead – reflective of a bear trend with momentum behind it, and a summer of soft prices on the horizon (see chart).

Near-term delivery prices are knocking on the door of support established by the lows of June ’23 (when Month-Ahead printed 55p/therm).

Key drivers remain overwhelmingly bearish with demand below seasonal norms (limiting withdrawal) against an increasingly benign backdrop of temperatures expected to stay above seasonal norms (and consensus building that the much touted February cold snap is unlikely to materialise).

Drivers across the wider energy complex are further contributing to bearish momentum with Europe’s coal stocks plentiful, and carbon testing historical lows.

LNG supply has been instrumental in replacing the loss of Russia’s exports into Western Europe.

Going forward, we may find that China’s switch from coal to gas will drive competition for global LNG exports – which may support LNG prices in the long run.

But for now (with Summer-24 only 47 days away), only geo-political unrest poses any risk to a continuation of the prevailing bear trend.

Monthly Day-Ahead averages are on target this month (so far) to achieve 68p/therm (or circa. 2.3p/kwh).

ELECTRICITY & CARBON ALLOWANCES

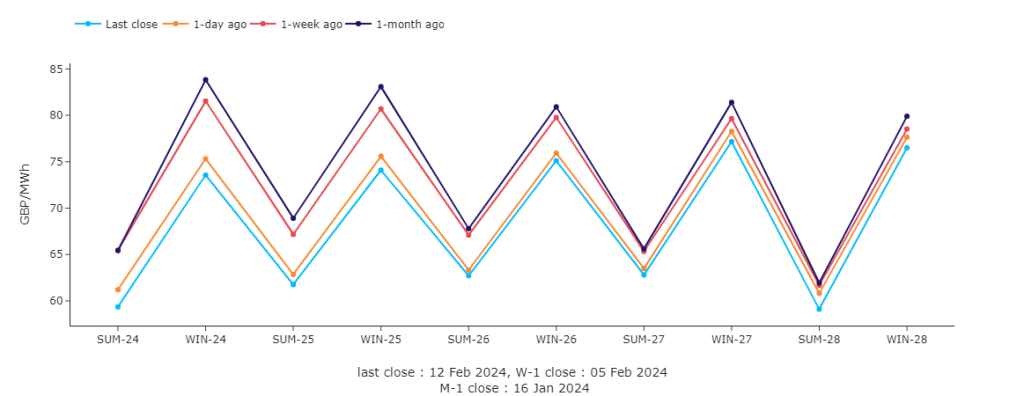

For the first time since 2018, Seasonal Forwards have assumed a contango state (future delivery prices more expensive than near-term delivery prices) – see chart.

Looking to the continent, near-term delivery prices dropped again yesterday driven down by weaker fuels and emissions prices along with expectations of slightly higher wind production and nuclear availability.

Expect prices to close lower again today in anticipation of tomorrow’s spike in temperatures across parts of NW Europe.

Declining gas and carbon prices also dragged long-term electricity prices lower yesterday following yet another milder revision of weather forecasts.

With European gas stocks at an all time high (67% versus the 5-year average of 54%), ongoing Industrial demand destruction and the “solar season” just around the corner with days getting longer, it’s difficult to see where any upward momentum might come from (save geo-political escalations).

Of course, a short-lived technical rebound is always a possibility when markets are so oversold – but any dead-cat bounce is likely to be modest.

European carbon prices remain under pressure and currently sit at a 23-month low.

The COT Commitment of Traders report) is due out today and may show another increase in speculators’ net short position (potentially prompting scalpers/short-term traders to trigger a short squeeze).

UKAs (UK carbon allowances) are circa. £37/tonne with a retest of 29th Jan lows of £36/tonne surely very likely if EUAs fall further.

Back in the UK, our generation mix is neutral with renewables contributing 30% and gas-for-power burn at 40%.

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £60/mwh (or 6p/kwh).