Skip to content

Energy Buyers Guide

Market Intelligence

ESOS Phase 3

SECR

Menu

Energy Buyers Guide

Market Intelligence

ESOS Phase 3

SECR

Tribar360 Login

0191 215 5456

enquiries@icdenergymanagers.com

Energy Buyers Guide

Market Intelligence

ESOS Phase 3

SECR

Energy Buyers Guide

ESOS Phase 3

Market Intelligence

SECR

Market Insight

Datasets reproduced in partnership with

Thurs, 22nd Feb ’24

GAS

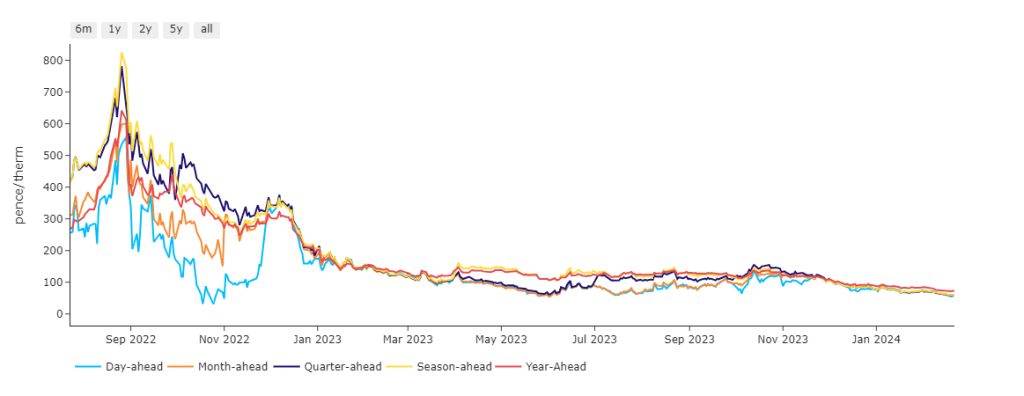

Bias remains neutral to bearish, with volatility almost flat compared to the chaos of 2022 (see chart).

Temperatures remain above seasonal norms amid decent wind outputs (limiting gas-for-power burn).

Down the curve, Forward contracts are meandering on decent volume but with little discernible direction!

European gas fullness is at 65% versus 5-year average of 45%.

On the supply side, Norwegian flows are at steady capacity despite extended unscheduled outages.

Ample supply and historically high storage makes any potential upside risk to near-term delivery prices limited.

In short, the bear-trend that began in Q422 is still in place.

With Summer-24 only 38 days away, only geo-political unrest poses any risk to a continuation of the prevailing bear trend.

Monthly Day-Ahead averages are on target this month (so far) to achieve 65p/therm (or circa. 2.2p/kwh).

ELECTRICITY & CARBON ALLOWANCES

Looking to the continent, the fundamental situation is bearish until the evening and likely marginally bullish thereafter.

Demand is dropping on the weekly cycle.

Wind supply is lifted and solar power generation is climbing (as the days get longer).

Moderate to high winds are expected to persist across Europe for the next 10-days or so.

On the carbon markets, the weekly COT( Commitments of Traders Report) published yesterday showed marginally lowered speculative interest.

Prices remain in a narrow trading range, mostly due to the lack of auctions yesterday and support from investment funds.

Energy fundamentals are relatively weak and unsupportive – as such, carbon may continue to take direction from gas.

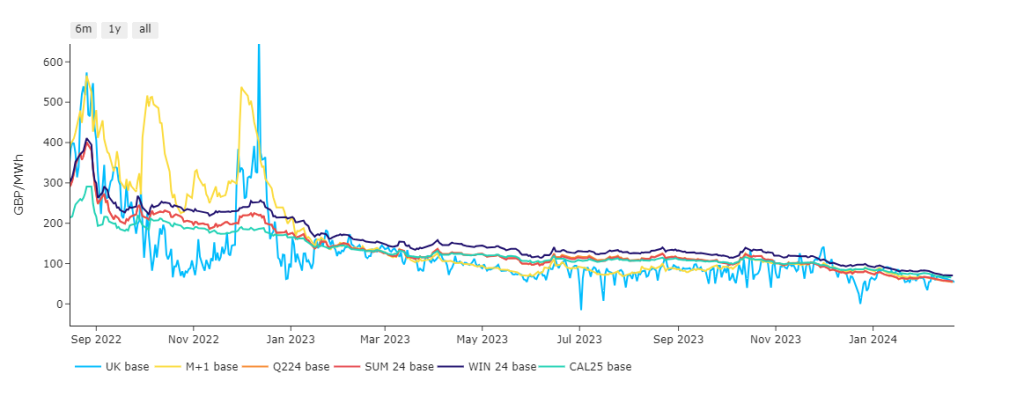

Back in the UK, our generation mix is bearish with renewables contributing 37% and gas-for-power burn at 23%.

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £60/mwh (or 6p/kwh).

Back to Market Insight

Share

Facebook

Twitter

LinkedIn

Search

Search

SERVICES

Tribar Client

Tendering & Procurement

Risk-Management

Market Intelligence

Compliance & Accreditation

UK-ETS Procurement & Advisory

Water Procurement & Advisory

Energy Audits

Net Zero Advisory

Monitoring & Targeting

Bureau & Client Services

Partner Agreements

Information

ESOS Phase 3

SECR

Market Intelligence

CONTACT

0191 215 5456

enquiries@icdenergymanagers.com

@icd-energy-managers

Get in Touch

INFORMATION

Case Studies

Weekly Market Intelligence

Energy reports

Endorsements

News

Case Studies

Testimonials

Values

About us

Our Method

Our Process

Our Team

Our Vision

Our Commitment

Compliance

Climate Change Agreements

ESOS Phase 3

SECR

How can we help?

Name

Phone

Email

Message

Send

How can we help?

Name

Phone

Email

Message

Send