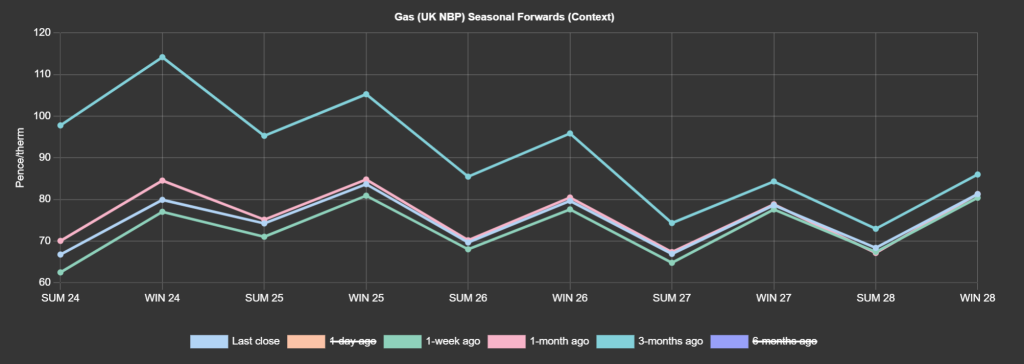

Markets have found support over the last week, but the bigger picture is one of front-end prices being 31% below those offered 3-months ago (see chart).

It’s been sideways price action this morning reflecting a balanced market enjoying some well-earned equilibrium with neither bulls nor bears managing to break out of rangebound trading conditions.

Looking down the Seasonal Forwards (Summer-24 to Winter-28, nine seasons), the most expensive contract is Winter-25 currently offered at 84.48 p/therm.

The least expensive contract is Summer-24 at 67.540 p/therm – a 29% variance between these two extremities.

Prices dropped off a little at yesterday’s close against a backdrop of lower demand due to improving temperatures and wind outputs (limiting gas-for-power generation).

It could be argued that lower LNG imports into the UK have been behind marginally higher prices this last week – but more likely, markets have fallen to a fair price and now they’re treading water/testing support and resistance levels.

Withdrawals throughout February were modest, and European inventories are on track to finish Winter-23 with more than 50% left in the tank – currently at 62% versus the 5-year average of 43%.

Geo-political risk persists with ongoing shipping attacks in the Red Sea area – though LNG is mostly headed around the Cape of Good Hope.

Russia’s flows are still missed, and their absence explains why markets haven’t fallen further (yet).

Notably (and a bullish driver), China imported more than 20 million tonnes of natural gas in the first month of ’24 – equating to y-o-y growth of more than 20%.

24 days of Winter-23 remain, and buyers are looking to summer conditioning to further soften Winter-24 offers.

Monthly Day-Ahead averages are on target this month to achieve 68p/therm (or 2.3p/kwh).

ELECTRICITY & CARBON

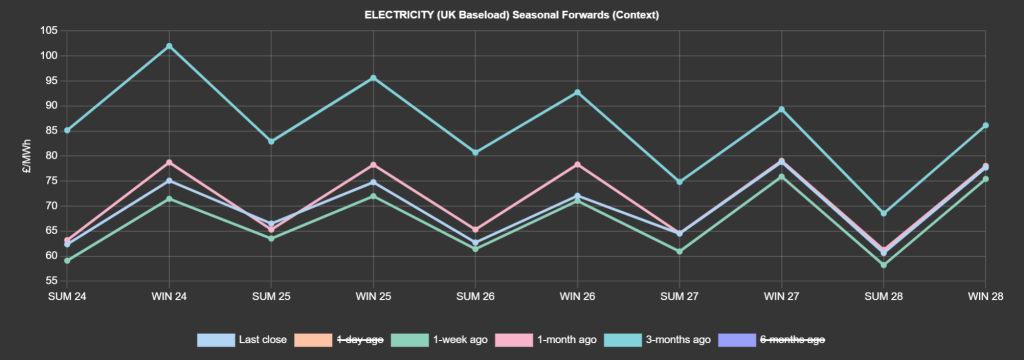

Looking down the Seasonal Forwards (Summer-24 to Winter-28, nine seasons), the most expensive contract is Winter-27 currently offered at £78.82/mwh.

The least expensive contract is Summer-28 at £60.63/mwh – a 22% variance between these two extremities.

Looking to the continent, European near-term delivery prices dropped a little yesterday pressured by improved renewables outputs, milder temperatures, softer fuels and emissions prices, and improved French nuclear availability.

Short-covering (buying to close out a sell-position) persisted on the carbon markets alongside the latest COT (Commitment of Traders report) showing only a slight reduction in speculators’ short position versus last week.

The upward move however lost its momentum by early-afternoon eventually closing below Tuesday’s settlement.

Prices opened lower again this morning off the back of a warmer revision of weather forecasts indicating the short-squeeze may have run out of steam.

Back in the UK, UKAs closed marginally down at £36/tn.

At the time of writing, our electricity generation mix is bearish in nature with renewables contributing 43% and gas-for-power burn at 22%.

Monthly Day-Ahead averages are on target this month to achieve £67/mwh (or 6.7p/kwh).