Notwithstanding last week’s froth/noise, markets have resumed their downward trajectory this morning.

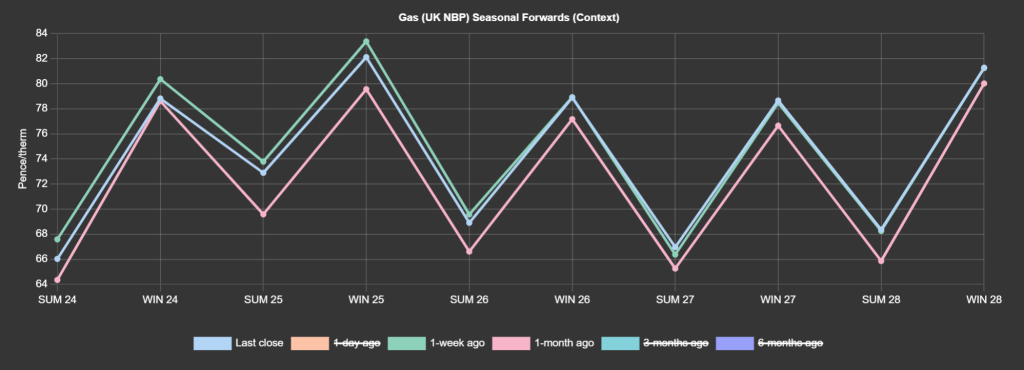

Key drivers remain overwhelmingly bearish and Seasonal Forwards are little changed versus 1-week/1-month ago (see chart).

On the supply side, European storage is at 61% versus the 5-year average of 41%.

Norwegian flows remain high and steady (despite unscheduled outages at the Nyhamna field).

The UK’s system opened short this morning – though demand remains below seasonal norms against a backdrop of temperatures remaining (in large part) above seasonal norms.

In no small part due to the resurgence of Freeport and the introduction of additional capacity at Calcasieu, America is likely to remain the world’s leading supplier of LNG in 2024 – with forecasts adding 4% to the country’s annual exports to just under 50 m/t (million tonnes).

Geo-political risk persists with ongoing shipping attacks in the Red Sea area – though LNG is mostly headed around the Cape of Good Hope.

Russia’s flows are still missed, and their absence explains why markets haven’t fallen further (yet).

Notably (and a bullish driver), China imported more than 20 million tonnes of natural gas in the first month of ’24 – equating to y-o-y growth of more than 20%.

20 days of Winter-23 remain, and buyers are looking to summer conditioning to further soften Winter-24 offers.

Monthly Day-Ahead averages are on target this month to achieve 68p/therm (or 2.3p/kwh).

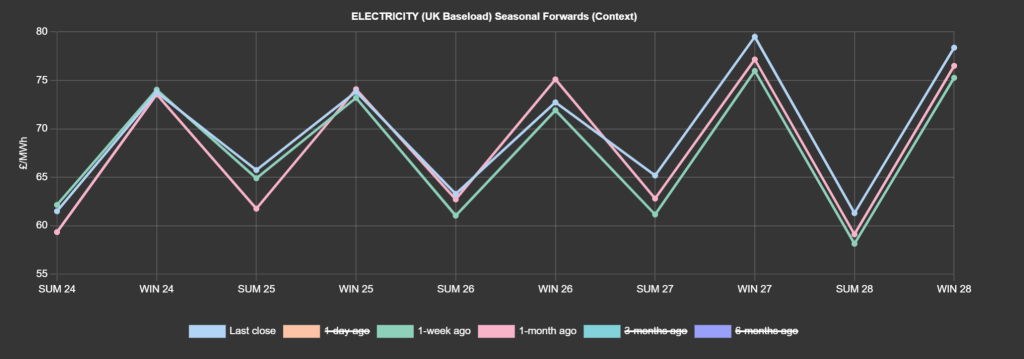

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices are marginally buoyed by decreasing renewables outputs alongside seaonal norm temperatures.

The strength of the market is likely to be short-lived with improving renewables outputs and higher temperatures forecast by the end of the week.

Down the curve, prices have resumed a bearish momentum following Friday’s short-covering rally – although with muted conviction (i.e., markets are stable and rangebound).

Markets are weighed further by a warmer and windier revision of weather forecasts for the second half of March.

In addition, bearish pressure is being exerted by the anticipation of the return of three French reactors by 23rd March, pushing the country’s nuclear availability back within historical range.

On the carbon markets, allowances continued to gently fade in the final session of the week – though aggressive bears are being matched by bottom-hunting Industrial bulls looking to capitalise on the value on offer.

UK Allowances closed last week around £35/tn – still testing support and resistance levels with a downside target of £30/tn, and an upside area of congestion circa £45/tn.

At the time of writing, our electricity generation mix is bullish in nature with renewables contributing 15.3%, thermal at 50.5% (gas and coal) and low carbon at 21.9% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £65/mwh (or 6.5p/kwh).