After several days of moderate bullish momentum, we saw some bearish price action at yesterday’s close.

Prices have fallen back a little further today – and it looks likely we’ll see another bearish close.

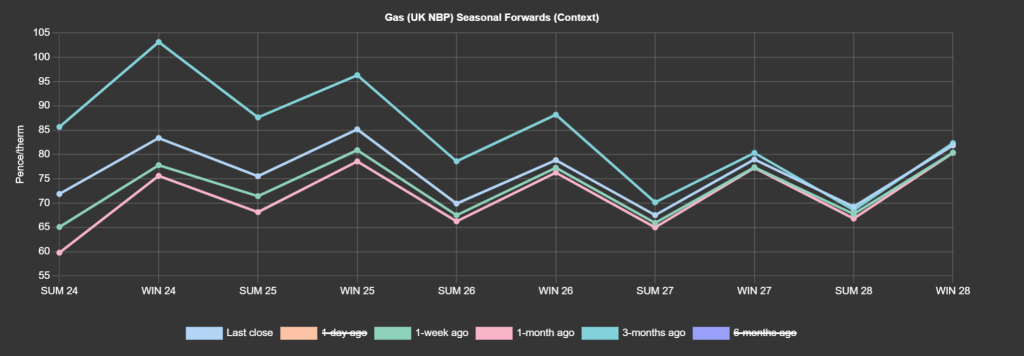

Seasonal Forwards are up on the week/month, but down versus 3-months ago (see chart).

Demand was marginally higher this morning (compared to yesterday) off the back of weak wind outputs (increasing the need for gas-for-power burn).

Temperature forecasts are ambiguous across the board, so it’s tricky to gauge what’s in store over the weekend.

With only 10 days of Winter-23 remaining, European storage looks set to close out the winter with circa 60% still left in the tank (versus the 5-year average of 41%).

Coupled with a resumption of Norwegian flows (with recent unscheduled outages having been resolved), downside pressure has picked up.

Notably, the drop in JKM prices (the Asian spot price index for LNG delivered to Japan and Korea) tends to confirm that Asian buyers will probably not buy LNG at any cost (because coal is a cheaper alternative).

Back in the UK, monthly Day-Ahead averages are on target this month to achieve 68p/therm (or 2.3p/kwh).

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices fell back yesterday, driven down by a retracement of fuels and emissions prices combined with forecasts of higher wind outputs.

Continuously driven by the gas market, prices down the curve traded sideways yesterday, opening with a rather steep correction attributed to anticipation of mild temperatures for late-March/early-April, before reversing mid-morning and slowly recovering throughout the remainder of the session.

Most contracts nonetheless closed lower on the day.

On the carbon markets, EUAs remained rangebound with a low volatility yesterday.

Observers have attributed this stability to the cautious sentiment prevailing in the market, with bears showing reluctance to take significant positions, whilst buyers appear to lack conviction.

The COT (Commitment of Traders report) showed a further weekly reduction of speculators’ net short position, potentially suggesting that their bearish view is weakening – or they’re happy to take profits and watch from the sidelines for now.

At the time of writing, Dec-24 contracts for UKAs are sitting at £38/tn.

Our electricity generation mix is bearish in nature today with renewables contributing 53%, thermal at 19% (gas and coal) and low carbon at 22% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £65/mwh (or 6.5p/kwh).