Contracts all the way down the curve are trading a little higher this morning off the back of reports that Russia has attacked an underground Ukrainian gas storage facility.

Ukraine ensured that supply has not been disrupted – however, further attacks on Ukrainian power facilities have resulted in the nation losing circa. 50% of its generating capacity, resulting in a cessation of electricity exports.

Fears of supply tightness has refocussed market participants’ attention on the ongoing disruption in the Red Sea.

In turn, concerns now abound that LNG supply to Europe/UK has dropped too far (with the UK set to receive just one cargo before month end).

Unfortunately, to further compound the Monday-worry, EDF has confirmed the extension of outages at two French reactors this morning.

Not surprisingly, with all this anxiety to feed on, market bulls have jumped all over price, and bears have been squeezed out of short positions.

Despite the bulls having taken hold for now, it’s worth pointing out that the UK system is comfortably long (supply outstripping demand), with demand wll below seasonal norms (given solid renewables outputs and mild temperatures).

Lest we forget, European storages remain at historical highs (59% fullness versus 38%) – with only 6 days of Winter-23 remaining before the onset of summer conditioning.

In short, fundamentals remain comfortable and any downside potential before the weekend’s geo-political flare-up was limited anyway (because of the LNG supply risk).

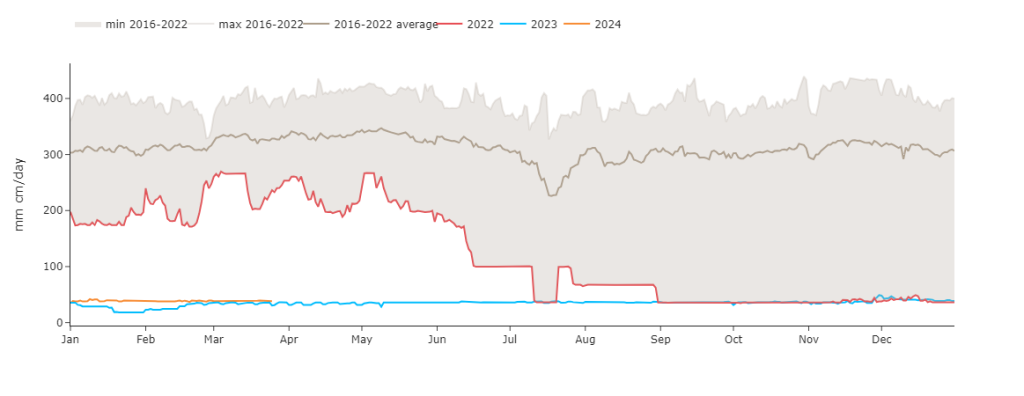

It’s a curious thing that Russia still exports gas through Ukraine (given of course that Nordstream remains unsanctioned/blown-up) – see chart for remaining flows.

Given the rise in attacks on energy facilities in Russia and in Ukraine in the past weeks and the rise in tensions since the attack which occurred in Moscow on Friday, risk of the loss of these remaining flows is now being built into price.

Notwithstanding the volatility we’ve seen this morning (increases down the curve of circa. 2p/therm), the upward move feels unsustainable (considering persistent weak demand and healthy gas stocks).

Monthly Day-Ahead averages are on target this month to achieve 68p/therm (or 2.3p/kwh).

ELECTRICITY & CARBON

Looking to the continent for more details, the energy complex is spiky today – with gas, power and carbon prices already opening circa. 3.5% higher than Friday’s settlements, likely buoyed once again by a downward revision of temperatures and wind forecasts for early-April, along with rising worries of gas supply reduction following the attack in Russia.

Beware of short covering fueling further the prices volatility in the carbon market as a significant amount of short positions are believed to have been taken above 65€/t, and a move above this level could squeeze investors and fuel a rally northwards.

Slightly colder than average temperatures will likely further support prices early this week, before weather turns progressively milder toward the weekend.

The strength of the gas market is attributed to the cold and calm weather expected in the first half of this week, boosting demand for thermal power plants/generation, although both factors seem a bit too speculative or weak to significantly tighten the markets’ balance and induce a sustained uptrend in forward prices.

With no particular news on the regulation side nor the industrial one, EUAs (and UKAs) are likely to continue following the gas market while market participants weigh-up if the recent progressive reduction of the investors’ net short position is a first sign that carbon has finally reached a floor, or simply a temporary profi-taking relief before prices resume their downward trajectory.

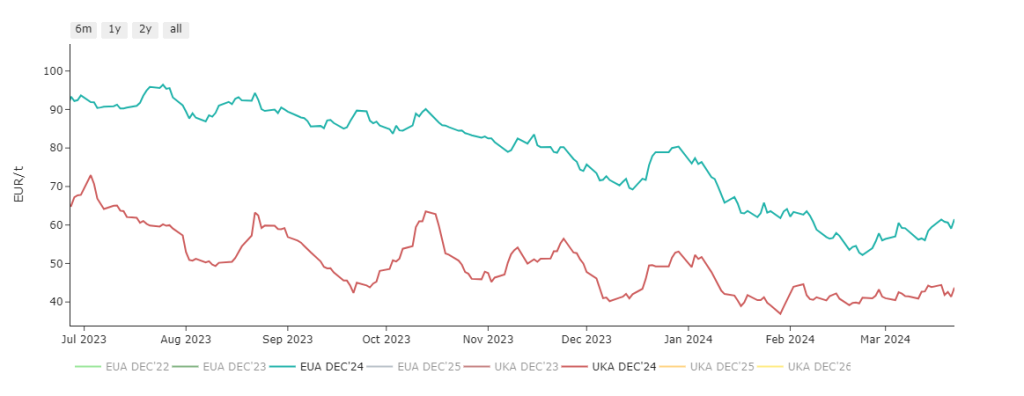

Back in the UK, UKAs are in and around £38/tn – the prevailing range at £45/tn to the topside (and £30/tn to the downside) – see chart of EUAs/UKAs comparison charted in EUROs.

Today, our electricity generation mix is neutral in nature with renewables contributing 35%, thermal at 29% (gas and coal) and low carbon at 25% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £62/mwh (or 6.2p/kwh).