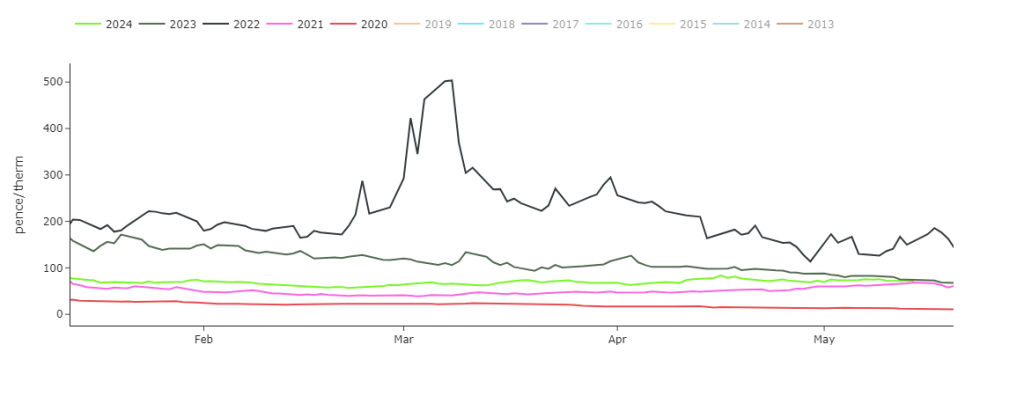

Month-Ahead prices have now reached parity with those offered in ’21/’23 – see chart.

Prices have dropped off a little versus this morning’s open – but it’s small potatoes, with prices still rangebound.

High pressure and warm/sunny/windless conditions are forecast for the remainder of May – reducing LDZ (local distribution heating demand) but also increased gas-for-power demand with wind outputs contributing less toward our generation mix.

The impacts of geopolitical outcomes continue to support the market (Middle East/Russia taking more territory from Ukraine/the US Presidential election being neck-and-neck).

Good news on the supply side – Freeport LNG terminal (Texas) is back up to capacity with all three trains back online.

On the continent, TTF (European gas market) Day-Ahead rates bounced yesterday despite the inherently sideways/balanced fundamental picture.

Reuters quoted several market participants attributing the marginally bullish session to mounting tensions on the Ukraine-Russia border in and around Kharkiv.

Ukraine have stated that Russia has positioned small assault units near Ukraine’s Sumy region, which is where the pipeline from Russia carrying gas across Ukraine into the EU enters Ukraine at Sudzha.

At the time of writing, Russia’s Sudzha flows are holding steady (very marginally up versus yesterday).

Undeniably robust supply dynamics are expected to keep a lid on any major upward moves – with European gas storage at 64% versus a 5-year average of 61%.

Back in the UK, Norwegian flows are in good shape – with no major unscheduled outages.

Storage injections are expected to outweigh withdrawals today with MRS (European mid-range storage) nominating at 4 million cubic metres/d of injections compared to 3mcm/d of withdrawals yesterday.

Rough (UK storage) has nominated at 6mcm/d of injections.

In short, markets remain at equilibrium with geopolitical support at odds with seasonal pressure (falling demand/solid supply/less reliance on withdrawals etc).

Temperatures above seasonal norms and historically high gas storage levels continue to reduce the UK’s LNG demand – with only 1 cargo degasifying in May so far (though 3 more are expected).

Market participants still have the jitters over news that the EU will be sanctioning Russian LNG (giving rise to worries over supply tightness).

Monthly Day-Ahead averages are on target this month to achieve 72p/therm (or circa. 2.45p/kwh).

ELECTRICITY & CARBON

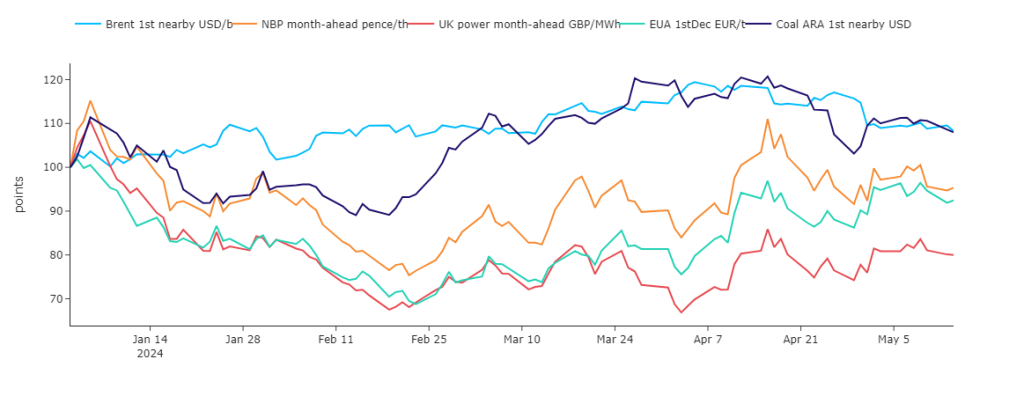

Looking at near-term delivery UK energy commodities, baseload electricity represents the best relative value – with premium having increased on gas at the onset of Summer-24 (see chart).

On the continent, European prompt (near-term delivery) prices moderately rebounded yesterday in response to a drop in solar output during the evening peak of demand.

On the Carbon markets, profit-taking could put further downward pressure on prices this week (participants selling into the market to close out buy positions).

The return to a normal auction schedule this week (and next) will improve supply and likely add some bearish momentum.

The regular release of COT (The Commitment of Traders report) will be closely watched too after funds further trimmed net shorts last week – suggesting the smart money is eyeing an imminent upside move.

UKAs (UK Allowances) are trading at £38/tn (Dec-24 benchmark).

Our electricity generation mix is neutral in nature today with renewables contributing 29%, thermal at 32% (gas and coal) and low carbon at 28% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £70/mwh (or 7p/kwh).