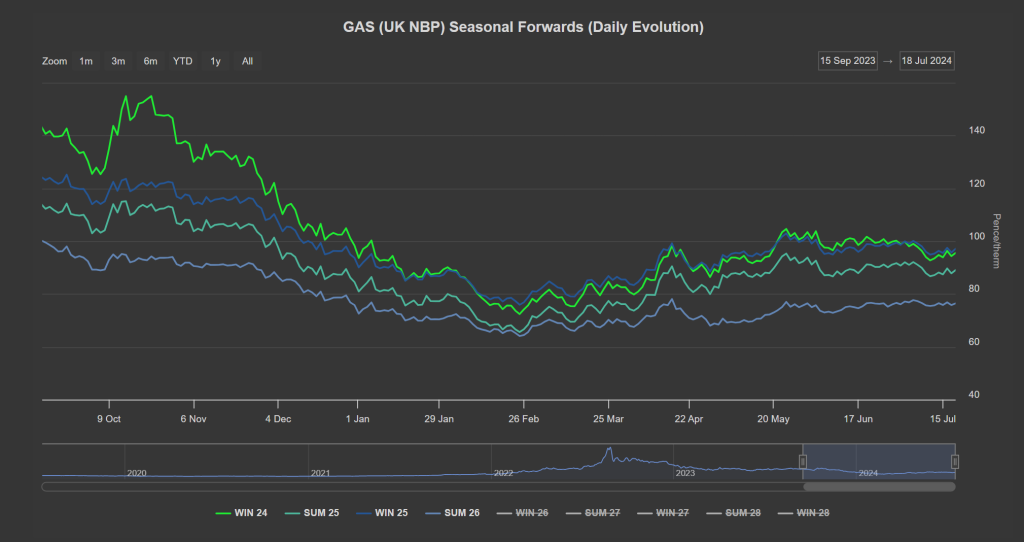

Winter-24 saw the biggest drop-off between Oct-23 to Feb-24, and has subsequently risen more steeply than Summer-25/Winter-25 over the course of the last few months – however, beginning last month, prices have been neutral to bearish (see chart).

Many financial market data feeds have been down today following the “Crowdstrike” system crash after a flawed software update prompted a global IT outage.

Nonetheless, at this morning’s open, prices moved lower off the back of a long system (supply outstripping demand forecast) and bearish fundamentals i.e., solid supply, weak demand amid a mini heat wave across parts of Europe.

Norwegian outages have lessened bringing stability to UK imports against a backdrop of steady injections into European storage.

Were it not for Freeport LNG still operating at reduced capacity, it’s likely we’d be seeing more downside price action – Freeport has been forced to cancel 10 scheduled shipments in the wake of damage caused by Hurricane Beryl.

Down the curve, longer term delivery contracts have been meandering sideways – with neither bulls nor bears having sufficient momentum to move the market.

All in all, solid injections and high European storage (82% versus the 5-year average of 69%) coupled with steady Norwegian flows continues to apply bearish pressure to a market exhibiting mild summery qualities.

With demand low, and supply comfortable, replenishing gas stocks is not posing any problems.

As such, Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24) – though LNG delivery remains tight against a backdrop of sustained high temperatures across Asia (and the associated cooling demand).

On the hedging side, we’re now on the other side of Summer-24 – with 110 days having elapsed, and 74 remaining.

Clients with open volumes for Winter-24 are increasingly scaling-in so as to avoid any loss of prevailing value.

Monthly Day-Ahead averages so far this month are on target to achieve 75p/therm (or circa. 2.55p/kwh excluding non-gas).

ELECTRICITY & CARBON

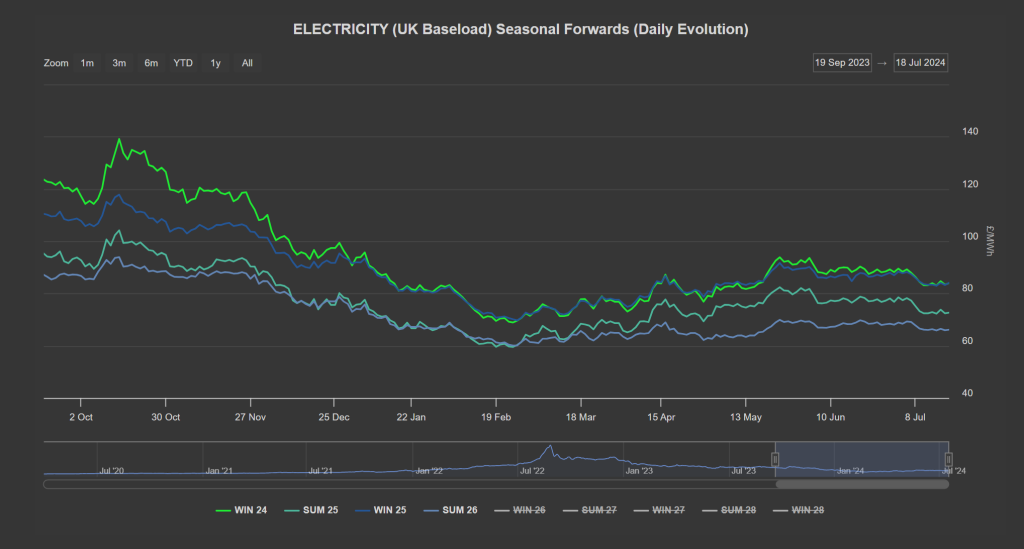

Looking to the continent, near-term delivery prices remain elevated amid a warm spell spreading over North-Western Europe (increasing cooling demand).

Even with prices dipping sharply in the afternoon (due to significant solar generation), prices have been spiking later in the evening.

Forward prices rebounded slightly yesterday, following the moderate uptick in gas prices.

On the Carbon markets, EUA prices continue to drift southwards with the benchmark Dec ’24 contract closing yesterday at €66.44/tn, now at €66.30/tn.

Bears are eyeing the €65/tn support, as breaching this level to the downside could open the door to a deeper retracement.

Back in the UK, UKAs (UK Carbon Allowances) followed our prediction that prices were due to fall (as indicated by RSI divergence) – now trading at circa. £40.72/tn.

If EUAs break with €65/tn, it looks likley UKAs will retest £40/tn with the next downside target at £39/tn.

Our electricity generation mix is bearish in nature today with renewables contributing 49%, thermal at 15% (gas and coal) and low carbon at 25% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £67/mwh (or circa. 6.7p/kwh excluding non-energy).