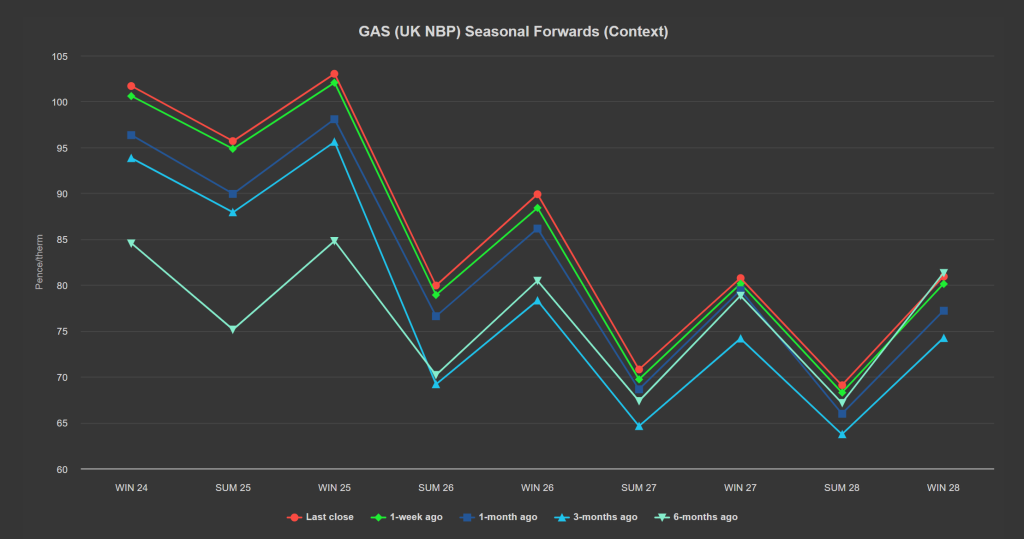

The see-sawing Summer-24 market is back at the top of its trading range – closing yesterday up versus 1-week ago/1-month ago/3-months ago/6-months ago(see chart below).

Whilst we witnessed a little bit of sell-off yesterday to mirror a global equity sell-off (in reaction to US jobless claims numbers indicating the world’s largest economy might be headed for a slow-down), markets have found their feet again today.

Both near- and far-term delivery prices were up at this morning’s open notwithstanding a long UK system (supply outstripping demand forecast).

Watchful eyes are trained on the Middle East as traders wait for a retaliatory strike by Iran on Israel.

Higher temperatures around the globe (notably Europe and Asia) have increased cooling demand propping up risk-premiums.

As a direct consequence of the European heatwave, the projected volume of LNG on European waters waiting for available terminals at which to degasify increased around 8% week-on-week.

Nonetheless, there are currently no LNG vessels set to land in the UK in the next couple of weeks.

Over the course of Summer-24 so far, demand has remained low against a backdrop of comfortable supply/storage – as such, replenishing gas stocks has not posed any problems.

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24).

European storage is at 86% fullness versus the 5-year average of 76%.

On the hedging side, we’re now on the other side of Summer-24 – with 128 days having elapsed, and 56 remaining.

Clients with open volumes for Winter-24 are now in the minority – with most having opted to close-out Positions given the ongoing geopolitical uncertainties and winter conditions now on the horizon.

Monthly Day-Ahead averages so far this month are on target to achieve 82p/therm (or circa. 2.8p/kwh excluding non-gas).

ELECTRICITY & CARBON

On the Carbon markets, EUA continue their bullish rally (correlating with recent gas price rises).

Back in the UK (and despite EUA’s bullish tone), UKAs (UK Carbon Allowances) have been slow to react – instead almost retesting £38/tn to the downside before being dragged back up by EUAs’ bullish fervour – now trading at circa. £39/tn.

At the time of writing, UKAs are trading within the confines of a confirmed strong bearish trend channel, and a confirmed weaker bullish trend channel – though £38/tn remains a viable target to the downside (see chart below).

Our electricity generation mix today is bearish in nature with renewables contributing 46%, thermal at 14% (gas and coal) and low carbon at 29% (nuclear and imports).

Electricity monthly Day-Ahead averages so far this month are on target to achieve £70/mwh (or approx. 7.0p/kwh excluding non-energy).