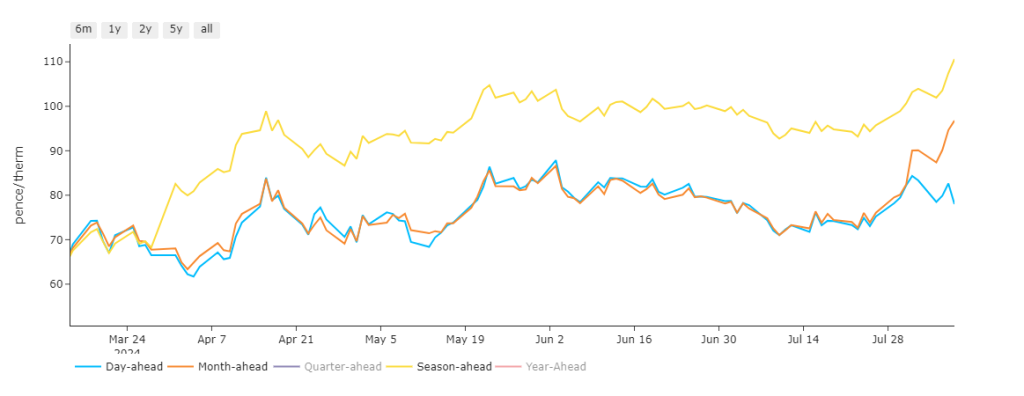

Whilst Day-Ahead prices have remained constant in response to Ukraine’s incursion into Russia, Month-Ahead and Season-Ahead are bullish reflecting higher mid-term risk (see chart below).

Russian forces have seemingly been caught off guard by Ukraine’s cross-border raid into Russian territory (Kursk) – having now captured the Sudzha border point (a transit juncture of the remaining Russian gas flowing into Europe via Ukraine).

At the time of writing, Russian gas flows via Sudzha remain uninterrupted but nominations are at lower levels day-on-day – understandably, market participants have the jitters and risk-premium at the front of the curve has been the outcome.

Whilst a gas transit agreement to move Russian gas via Ukraine expires at then end of the year, an earlier than expected halt to flows would come as a shock and is increasingly being priced-in.

It’s important to note that some central European nations still depend on this last vestige of Russian pipeline supply (Austria, Slovakia, Italy, Hungary, Croatia, Slovenia, and Moldova).

In addition, fears of escalation across the Middle East continue to limit the chance of any meaningful summer downside with Iran expected to respond militarily (following the assassination of the leader of Hamas).

Looking at the big picture, were it not for ongoing geopolitical uncertainties, summer conditioning would likely be softening both near- and far-term prices.

Weak demand and solid renewables outputs persist against a backdrop of historically high European storage.

The UK system again opened long this morning (supply outstripping demand forecast).

Nonetheless, European/UK LNG arrivals are on the floor – with Asian cooling demand (and associated higher prices) attracting the lion’s share of cargos.

Outage-wise, the short-term calendar is pretty sparse, with a couple forecast for UKCS (continental shelf).

Whilst Norwegian pipeline flows remain at the upper extremity of a 10-year range, the Kollsnes plant is undergoing unscheduled maintenance (which is temporarily reducing delivery to the UK/NW Europe).

Over the course of Summer-24 so far, demand has remained low against a backdrop of comfortable supply/storage – as such, replenishing gas stocks has not posed any problems.

Europe remains on track to achieve 100% storage fullness levels by Winter-24 (early Oct ’24) with inventories currently at 87% versus the 5-year average of 75%.

On the hedging side, we’re now on the other side of Summer-24 – with 131 days having elapsed, and 53 remaining.

Clients with open volumes for Winter-24 are now in the minority – with most having opted to close-out Positions given the ongoing geopolitical uncertainties and with winter conditions now on the horizon.

Monthly Day-Ahead averages so far this month are on target to achieve 81p/therm (or circa. 2.75p/kwh excluding non-gas).

ELECTRICITY & CARBON

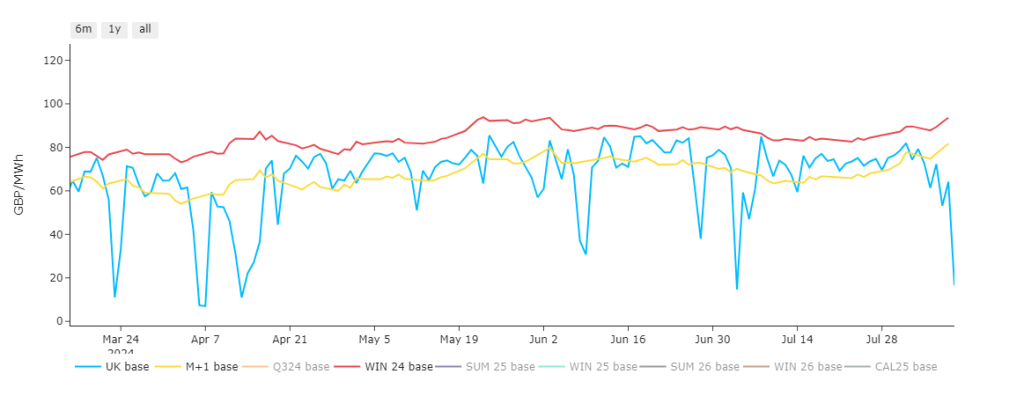

Whilst Day-Ahead dropped off significantly yesterday (reflecting benign near-term conditions, notwithstanding Ukraine’s incursion into Russia), Month-Ahead and Season-Ahead are mirroring the bullish gas rally (see chart below).

On the Carbon markets, EUA prices remain at a premium to UKAs, with EUAs now consolidating in a tight range at the top of last week’s bullish rally.

UKAs continue to fall (as indicated by the daily timeframe RSI divergence and confirmed descending trend channels) – now trading at circa. £38/tn.

At the time of writing, our electricity generation mix is very bearish (and “summery”) in nature today with renewables contributing 71%, thermal at 8% (gas and coal) and low carbon at 14% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £61/mwh (or circa. 6.1p/kwh excluding non-energy).