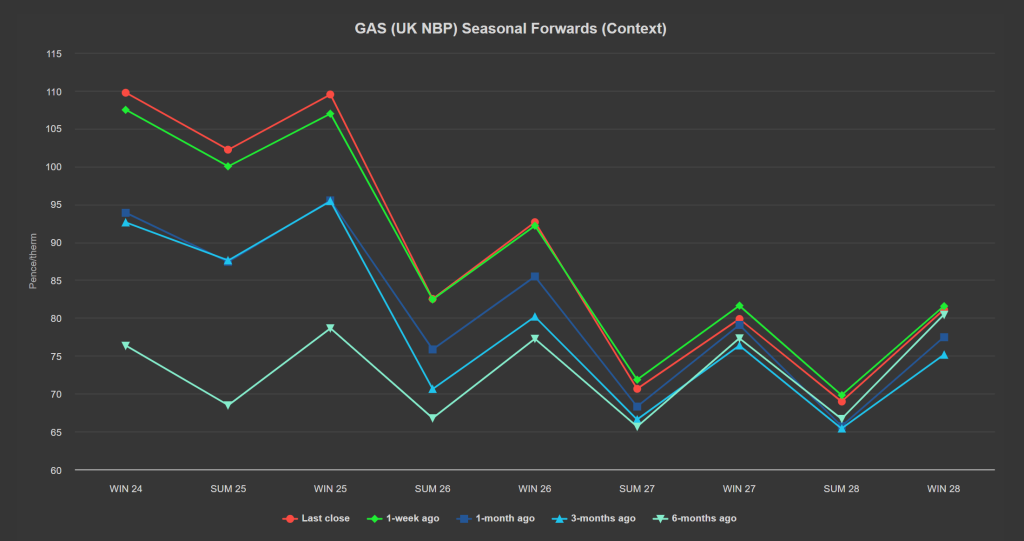

Seasonal Forwards remain up versus 1-week/1-month/3-months/6-months ago – see chart below.

Despite having dropped off during yesterday’s afternoon session, prices are marginally up again this morning off the back of the ongoing Ukrainian incursion into Russia (and the capturing of the Sudzha gas transit point, endangering Russia’s remaining flows into Western Europe).

2 LNG arrivals are now expected to degasify at UK terminals by September.

The impact of reduced LNG arrivals to Europe/UK has been less injection into storage.

Nonetheless, Europe remains on track to achieve 100% storage fullness levels by Winter-24 (early Oct ’24) with inventories currently at 88%.

The UK system was long at open (supply outstripping demand forecast).

Norwegian flows remain solid at the upper extremity of a 10-year range and above the 5-day moving average – to some extent, limiting upside/bullish momentum.

On the hedging side, we’re now on the other side of Summer-24 – with 135 days having elapsed, and 49 remaining.

Clients with open volumes for Winter-24 are now in the minority – with most having opted to close-out Positions given the ongoing geopolitical uncertainties and with winter conditions now on the horizon.

Monthly Day-Ahead averages so far this month are on target to achieve 82p/therm (or circa. 2.8p/kwh excluding non-gas).

ELECTRICITY & CARBON

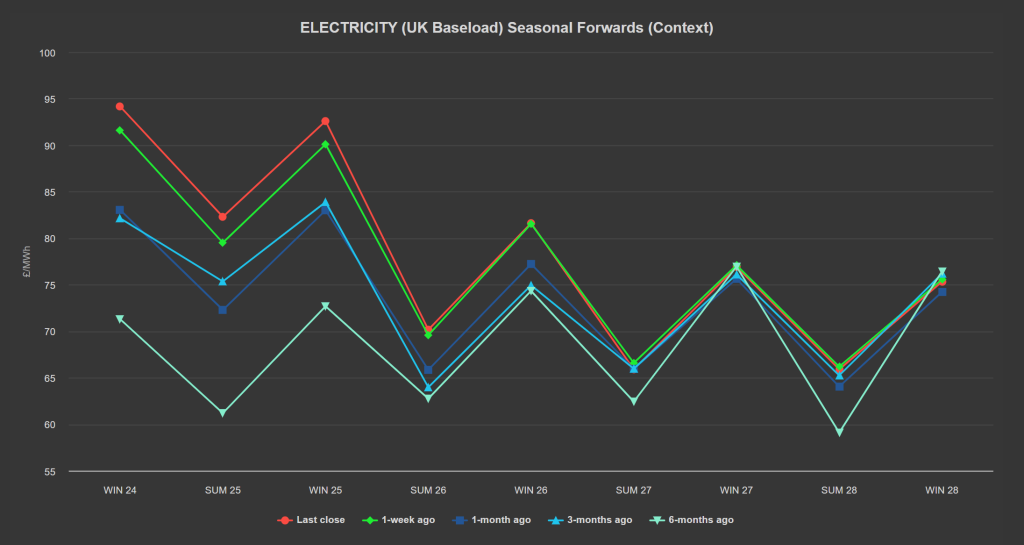

Whilst Day-Ahead printed a low number yesterday (£55/mwh), all other Forward periods of delivery are mirroring the bullish gas rally.

On the Carbon markets, EUA prices remain at a premium to UKAs, with EUAs now consolidating in a tight range at the top of last week’s bullish rally.

UKAs are moving off last week’s lows and trading at circa. £39/tn.

At the time of writing, our electricity generation mix is neutral in nature today with renewables contributing 22%, thermal at 31% (gas and coal) and low carbon at 31% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £63/mwh (or circa. 6.3p/kwh excluding non-energy).