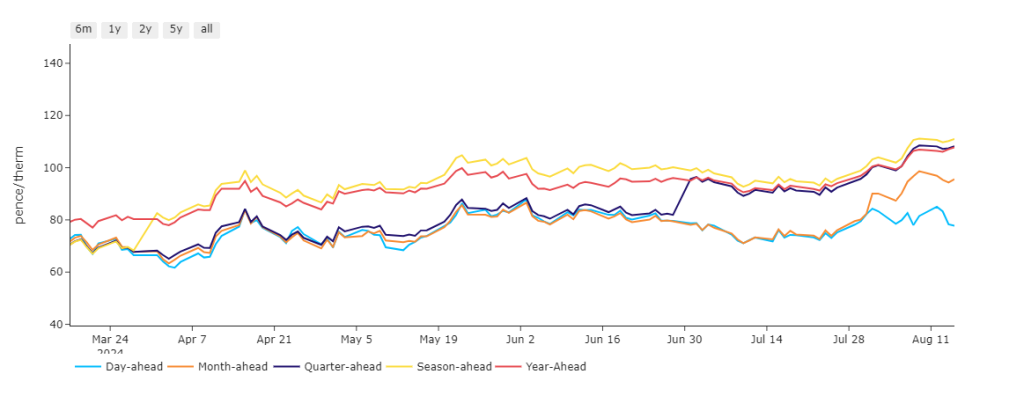

Day-Ahead holds steady at approx. 80p/therm whilst Month-Ahead has diverged and rallied to hold approx. 95p/therm with Qrtr/Season/Year-Ahead at parity around 110p/therm – see chart below.

Premium in current markets is primarily derived from risks to supply security – primarily geopolitical uncertainty in Ukraine/Russia (threatening Sudzha transit) and Israel/Iran (threatening Suez Canal LNG transit).

UK gas prices opened marginally higher in early trading but have dropped off over the course of the morning – it’s sideways price action, but 110p/therm for Winter-24 delivery will need strong bearish momentum to break to the downside.

The UK continues to export to the continent – a reflection the UK is generating more than demand requires.

Forecasts of stronger wind generation for the middle of next week will help to reduce gas-for-power demand.

So, we may see retests of 110p/therm for Winter-24 next week subject to geopolitical developments.

More Norwegian maintenance is scheduled for the end of August.

However, at the time of writing, Norwegian flows remain solid at the upper extremity of a 10-year range and above the 5-day moving average – thankfully, limiting upside/bullish momentum.

European storage is at 88% versus the 5-year average of 78%.

On the hedging side, we’re now on the other side of Summer-24 – with 138 days having elapsed, and 46 remaining.

Clients with open volumes for Winter-24 are now in the minority – with most having opted to close-out Positions given the ongoing geopolitical uncertainties and with winter conditions now on the horizon.

Monthly Day-Ahead averages so far this month are on target to achieve 82p/therm (or circa. 2.8p/kwh excluding non-gas).

ELECTRICITY & CARBON

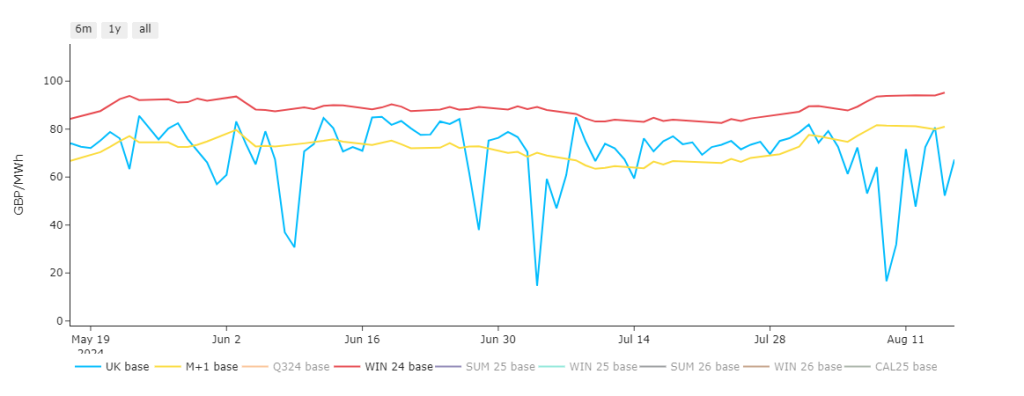

Day-Ahead prices remain comfortably below Winter-24 delivery, and averaging well-below Month-Ahead – see chart below.

On the Carbon markets, EUA prices remain at a premium to UKAs, with EUAs edging higher.

UKAs have rallied off last week’s lows (£37.87/tn on 9th august) – now trading back above £40/tn.

At the time of writing, our electricity generation mix is neutral in nature today with renewables contributing 46%, thermal at 11% (gas and coal) and low carbon at 31% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £63/mwh (or circa. 6.3p/kwh excluding non-energy).