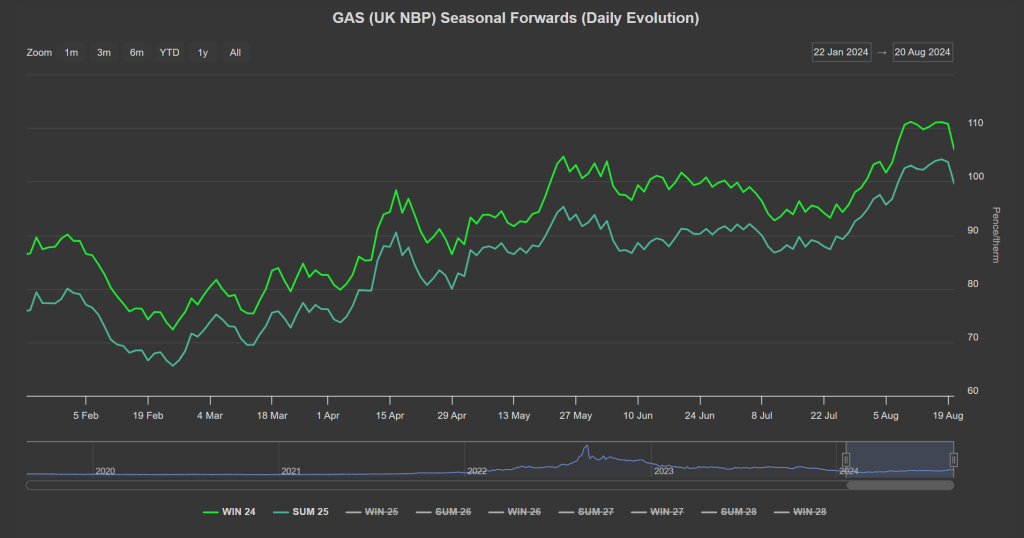

The Front Seasons (Winter-24/Summer-25) have rolled-over this week (see chart below) off the back of flows continuing uninterrupted via Sudzha – bringing a degree of calm to energy markets following the bullish impacts of Ukraine’s incursion into Russian territory.

The front of the curve has closed this afternoon approximately 10p/therm lower than the intraday highs we saw back on 12th Aug.

Storage levels at the upper extremity of the 5-year range continue to limit upside momentum with European MRS (mid-range storage) having already hit the 90% fullness objective a full 2-months before the November target.

Optimism abounds that a ceasefire of sorts between Israel/Hamas is now a very real prospect which is taking further heat out of the markets.

Norway’s period of heavy scheduled summer maintenance is nearly upon us, which is likely to limit any meaningful bearish momentum before the onset of Winter-24.

Lest we forget, notwithstanding recent anxiety over the Sudzha transit point, the transport deal between Russia and Ukraine is to expire at the end of 2024 anyway – will it be extended?

LNG flows to Northwest Europe are now approx 8% below the 30-day average – reflecting a decline in European demand.

We’re now also seeing cooling demand drop-off throughout Asia with inventories of LNG falling – if this trend persists, pressure will ease on the JKM/NBP spread, and competition for arrivals will soften.

European storage is at 90% versus the 5-year average of 79%.

On the hedging side, we’re now on the other side of Summer-24 – with 143 days having elapsed, and 41 remaining.

Clients with open volumes for Winter-24 are now very much in the minority – with most having opted to close-out Positions against the backdrop of ongoing geopolitical uncertainties (and with winter conditions now on the horizon).

Monthly Day-Ahead averages so far this month are on target to achieve 82p/therm (or circa. 2.8p/kwh excluding non-gas).

ELECTRICITY & CARBON

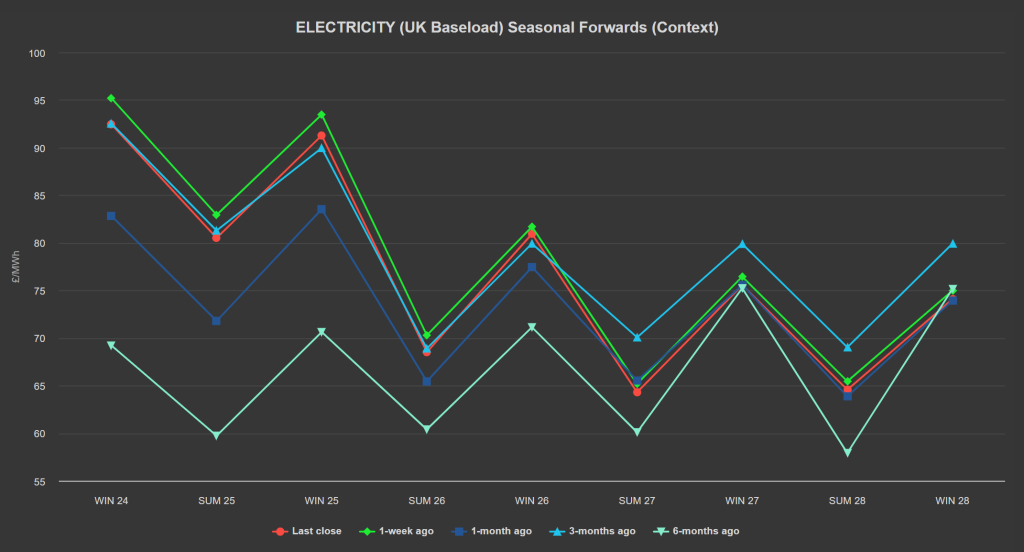

UK Seasonal Forwards are now commensurate with 1-month ago, and below 1-week ago (see chart below).

Looking to the continent, Europe’s near-term delivery prices averaged a 37% drop compared to Monday’s values.

Indeed, intraday negative prices are expected in all European countries during sun hours while the cooling demand remains limited – limiting the evening price spike.

Forward power prices have declined sharply off the back of easing fuel prices (gas/oil/coal).

On the Carbon markets, EUA prices remain at a premium to UKAs, with EUAs edging higher.

UKAs have rallied off last week’s lows (£37.87/tn on 9th august) – now trading back above £40/tn.

At the time of writing, our electricity generation mix is bearish in nature today with renewables contributing 55%, thermal at 15% (gas and coal) and low carbon at 22% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £60/mwh (or circa. 6.0p/kwh excluding non-energy).