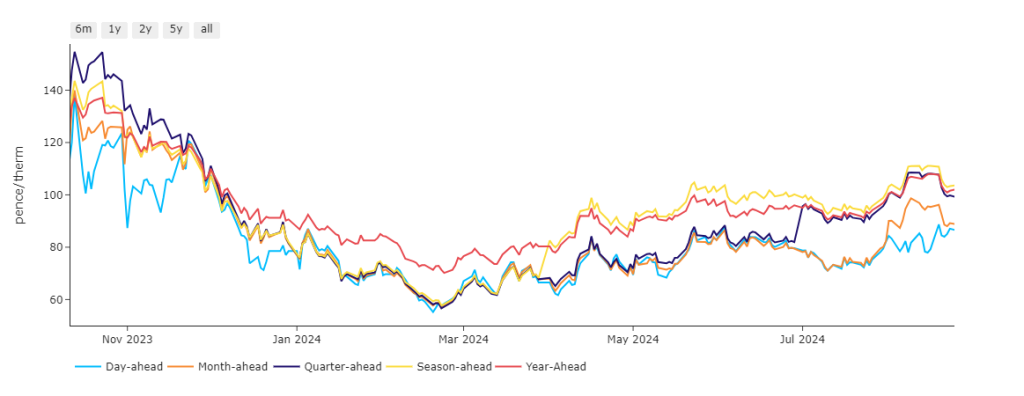

Having been at parity since the turn of the year, Day-Ahead is now significantly discounted versus Month-Ahead, reflecting increasing mid-term risk-premiums with only 34 days of Summer-24 remaining (see chart below).

The end of last week’s session saw some promising falls in Seasonal contracts with Winter-24 looking likely to have another crack at breaking below 100p/therm before the onset of the winter-shoulder month (September).

However, geopolitical developments over the weekend have put paid to any further downside, with this morning’s prices rallying off the back of Russian attacks on critical Ukrainian infrastructure raising worries over supply tightness.

Whilst the Sudzha transit point remains (for now) unaffected by recent skirmishes, concerns over significant disruption of gas flows continues to impact on sentiment with summer-conditioning increasingly in the rearview mirror.

Looking to the Middle East, ongoing talks in Egypt over the weekend failed (again) to secure an IDF/Hamas ceasefire.

Ominously, further strikes in the region followed the announcement of no agreement, likely signalling a potential backwards step, and heightening fears that global supply disruption will result should the conflict widen to include Iran etc.

On the supply side, Norwegian flow nominations, and LNG sendout, remain consistent versus the end of last week.

However, the bulk of summer’s final Norwegian maintenance outages has arrived – kicked off by Åsgard at the end of last week and followed by a full shutdown of Kårstø before this weekend.

In positive news, three LNG arrivals from the US are expected to degasify at UK ports before 10th September – reflecting a drop in cooling demand throughout Asia (and a likelihood that pressure will ease on the JKM/NBP spread softening competition for cargos).

The UK system opened long again this morning (supply outstripping demand forecast).

Overall, bullish drivers continue to be tempered by European storage fullness at 92% versus the 5-year average of 82%.

On the hedging side, we’re approaching the onset of Winter-24, with 150 days of Summer-24 now behind us.

Clients with open volumes for Winter-24 are very much in the minority – with most having opted to close-out Positions against the backdrop of ongoing geopolitical uncertainties (and with winter conditions now on the horizon).

Monthly Day-Ahead averages so far this month are on target to achieve 83p/therm (or circa. 2.8p/kwh excluding non-gas).

ELECTRICITY & CARBON

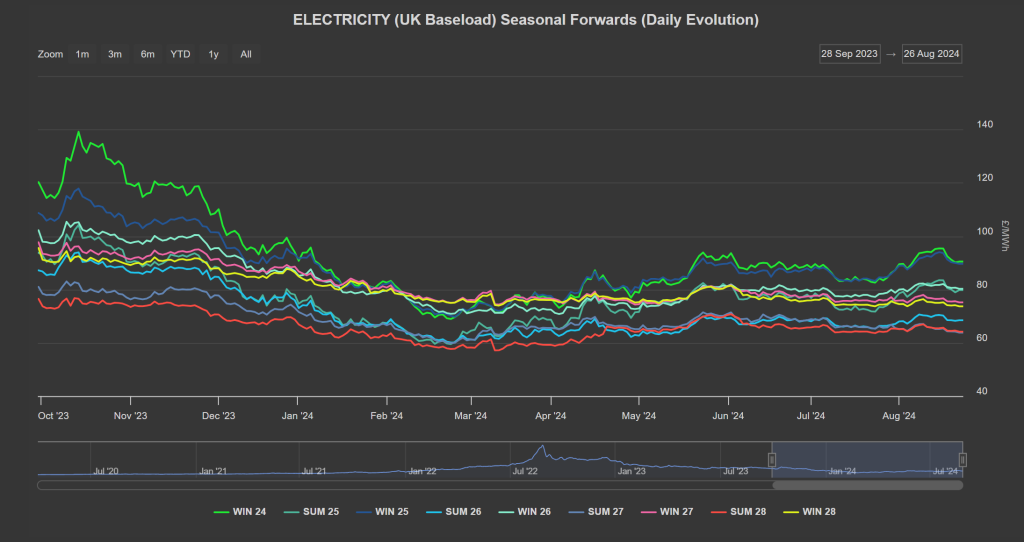

Seasonal Forwards are stacked in a perfectly backwardated state, but for Winter-25 carrying a marginally inflated premium versus Winter-24 (see chart below).

Looking to the continent for direction, it’s sideways price action – near-term delivery prices inched higher yesterday.

Seasonal forward contracts were torn between a climbing gas price and declining carbon price – consequently, trading in a tight range.

On the Carbon markets, EUA prices remain at a premium to UKAs – though both have dropped off to start the week.

UKAs rallied off 9th August lows of £37.87/tn and are now trading water back above £40/tn.

At the time of writing, our electricity generation mix is bearish in nature today with renewables contributing 59%, thermal at 9% (gas and coal) and low carbon at 21% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £58/mwh (or circa. 5.8p/kwh excluding non-energy).