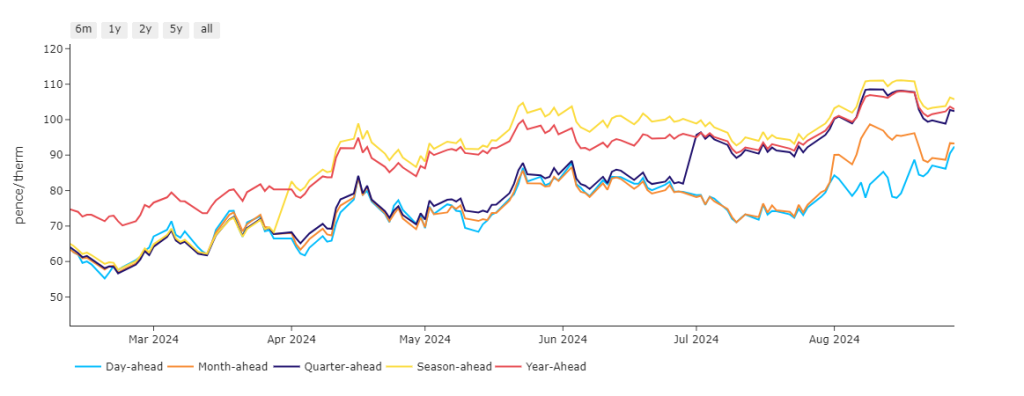

Day-Ahead has risen over the past few days, and is now at near-parity with Month-Ahead pricing – reflecting near-term delivery increases with the onset of Winter-24 now only 32-days away (see chart below).

As is often the case in the markets, drivers are priced-in before the fact – so markets are softening this morning despite the fact that significant Norwegian flows into the UK have gone offline today in preparation for the final round of scheduled summer maintenance outages (limiting supply).

Fortunately, wind outputs and are holding steady and temperatures remain above seasonal norms limiting gas-for-power demand.

Risk-premium continues to be attributed to the crucible that is the Middle East, and of course fears of the unknown that is the Ukraine/Russia conflict.

Notably, market speculation (as opposed to physical buyers) continues to skew the European gas markets – with investment funds very net long whilst physical buyers are net short!

Speculators are betting on higher prices off the back of a) the imminent contract expiry of the Ukrainian transit agreement (made more likely given that Ukraine have capured Sudzha!); b) delays of LNG projects across the globe: c) geopolitical tensions.

Physical buyers are betting on lower prices given a) very high European storage levels; b) weak demand.

The winter-shoulder month (September) is historically an edgy month due to the Atlantic hurricane season and the associated shipping lane disruption (impacting US LNG exports).

In other news, rumours abound that Ukraine intends to stockpile emergency reserves of gas from “European sources” as a contingency to counter the potential impact of recent Russian strikes.

Apparently, the volumes of contingency supply have been financed using leverage of €200 million from European lenders.

Three LNG arrivals from the US are expected to degasify at UK ports before 10th September – reflecting a drop in cooling demand throughout Asia (and a likelihood that pressure will ease on the JKM/NBP spread softening competition for cargos).

European storage fullness is at 92% versus the 5-year average of 87%.

Clients with significantly open volumes for Winter-24 are in the minority – with most having opted to heavily hedge Positions with winter conditions now on the horizon.

Monthly Day-Ahead averages so far this month are on target to achieve 83p/therm (or circa. 2.8p/kwh excluding non-gas).

ELECTRICITY & CARBON

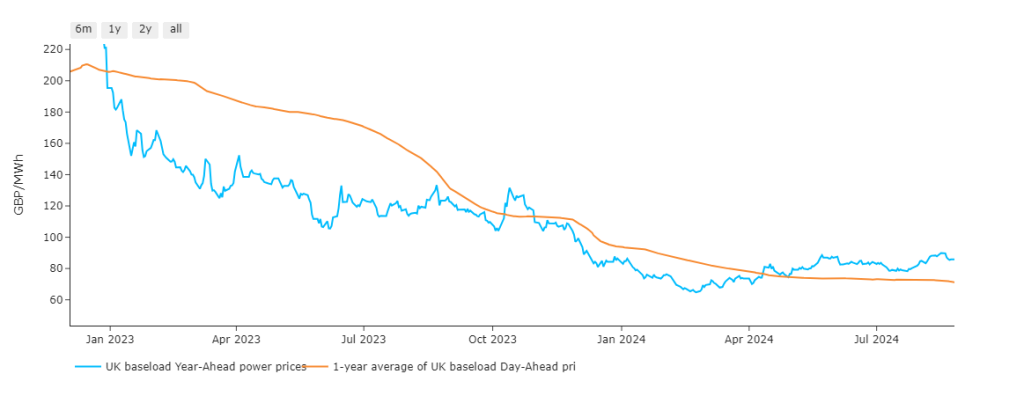

By way of an interesting metric, the UK yearly average of Day-Ahead prices remains below prevailing Year-Ahead prices – reflecting an increase in electricity premiums over Summer-24 (see chart).

Looking to Europe for indicators, near-term delivery prices closed yesterday at near yearly highs against a backdrop of high temperature anomalies (supporting demand for cooling), and below seasonal norm wind generation (failing to meet baseload requirements).

Conversely, Forward power prices lost a bit of ground yesterday, mirroring downward moves on the gas and carbon markets.

On the Carbon markets,EUA Dec ’24 benchamark prices continue to meander neutral to bearish.

As per the COT (Commitment of Traders Report) published last week, investment funds have reduced their net short position to the lowest level since July ’23 (in advance of winter conditioning and the associated supply/demand dynamics).

UKAs seem set to approach relative value parity with EUAs, having risen to £42/tn following the low achieved of £37 back on 9th August.

At the time of writing, our electricity generation mix is bearish in nature today with renewables contributing 45%, thermal at 16% (gas and coal) and low carbon at 26% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £58/mwh (or circa. 5.8p/kwh excluding non-energy).