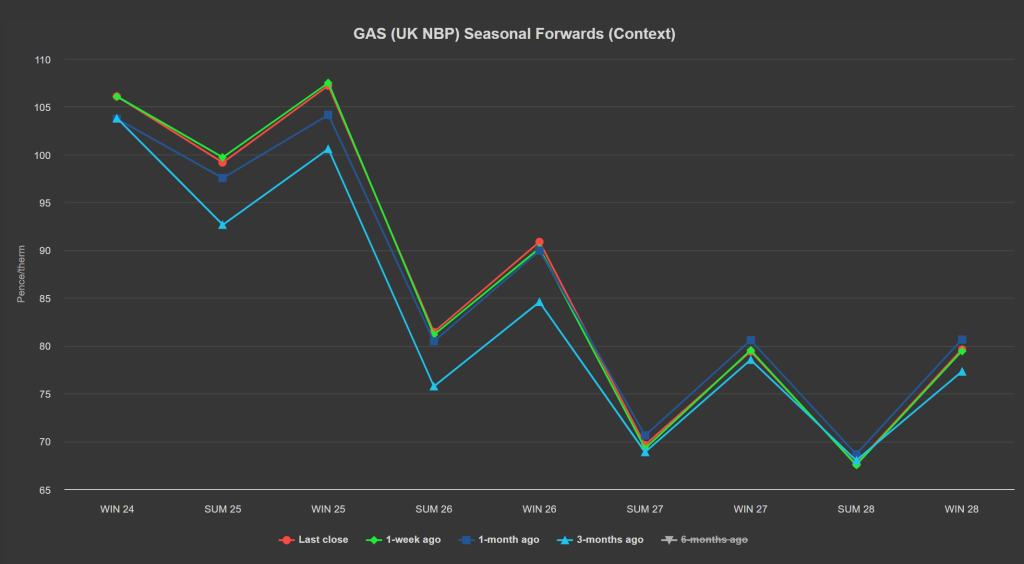

Seasonal Forwards are down on the week, but up on the month/3-months ago (see chart below).

Prices opened up this morning off the back of ongoing Norwegian maintenance (though the maintenance of the Kollsnes and Nyhamna gas-processing plants has been delayed).

Most notably, the Easington terminal is offline for maintenance from today until 16th September, meaning zero flows into the UK from Norway’s Langeled.

Not surprisingly then, the UK system opened short today despite demand being significantly below seasonal norms.

Given reduced Norwegian flows, the UK is now withdrawing 24mcm from storage to help balance the grid.

Accordingly, UK exports have reduced to retain volumes – this is set to continue, as the Interconnector will go offline for maintenance tomorrow (ending 18th September).

Temperatures are set to turn gradually cooler as the week progresses, before warming at the weekend.

Europe’s storage levels (92% full versus the 5-year average of 82%) continue to offset Europe’s demand for gas as the amount of LNG idling at sea for more than 30 days waiting to degasify is increasing – reaching 1.7 million tons last week (reflecting a glut).

Three LNG arrivals from the US are expected to degasify at UK ports before 10th September – reflecting a drop in cooling demand throughout Asia.

Clients with significantly open volumes for Winter-24 are in the minority – with most having opted to heavily hedge Positions with winter conditions now on the horizon.

Monthly Day-Ahead averages for August achieved 85p/therm (or approx. 2.9p/kwh excluding non-gas).

Monthly Day-Ahead averages so far this month are on target to achieve 94p/therm (or approx. 3.2p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent for direction, European near-term delivery prices averaged €111.11/mwh for delivery today.

Such high figures are among the highest power prices of the year.

Elevated temperatures, low wind speeds and declining hydro generation are the supportive drivers.

An increase in wind generation at the end of the week should help prices to trade lower.

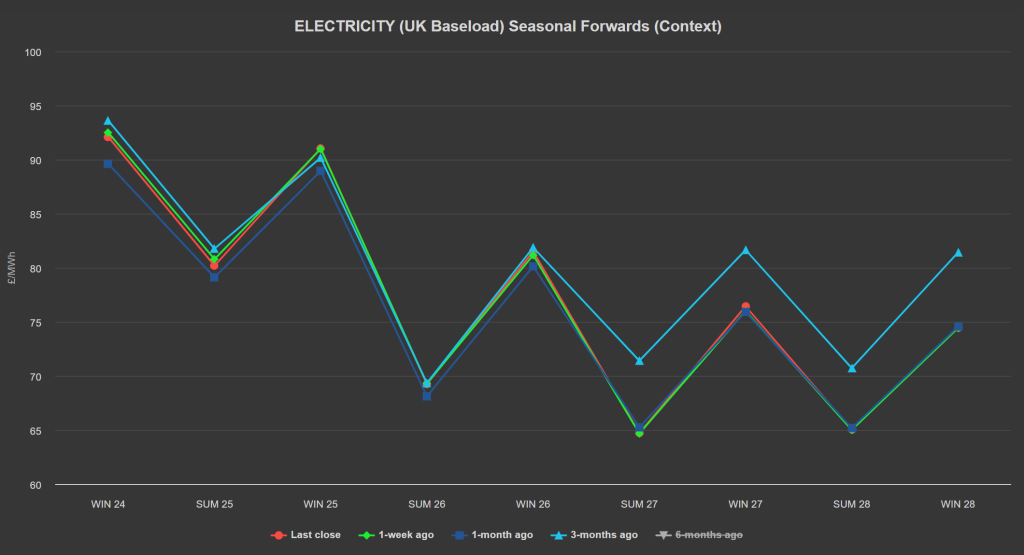

Seasonal Forward prices were down last week following developments on the carbon side, and despite higher gas prices.

On the Carbon markets, EUA’s are idling sideways, whilst UKAs are drifting higher.

From a technical perspective, the €70/tonne support level for EUA Dec ’24 is still holding but has been retested countless times over the past week, increasing the likelihood of it being breached.

And with a challenged correlation with gas, moves on EUAs seem even harder to anticipate.

Conversely, UKAs seem set to approach relative value parity with EUAs, having risen to £43/tonne following the low achieved of £37 back on 9th August.

Our electricity generation mix is bullish in nature today with renewables contributing 29%, thermal at 36% (gas and coal) and low carbon at 23% (nuclear and imports).

Monthly Day-Ahead averages for August achieved £60/mwh (or approx. 6p/kwh excluding non-energy).

Monthly Day-Ahead averages so far this month are on target to achieve £80/mwh (or approx. 8p/kwh excluding non-energy).