The increasingly unpredictable (and contrarian) movements of the European/UK gas markets persist – arguably reflecting a more speculative market condition where the participants (increasingly investment funds or “non-physical buyers”) are buying on the rumour, then selling on the news…

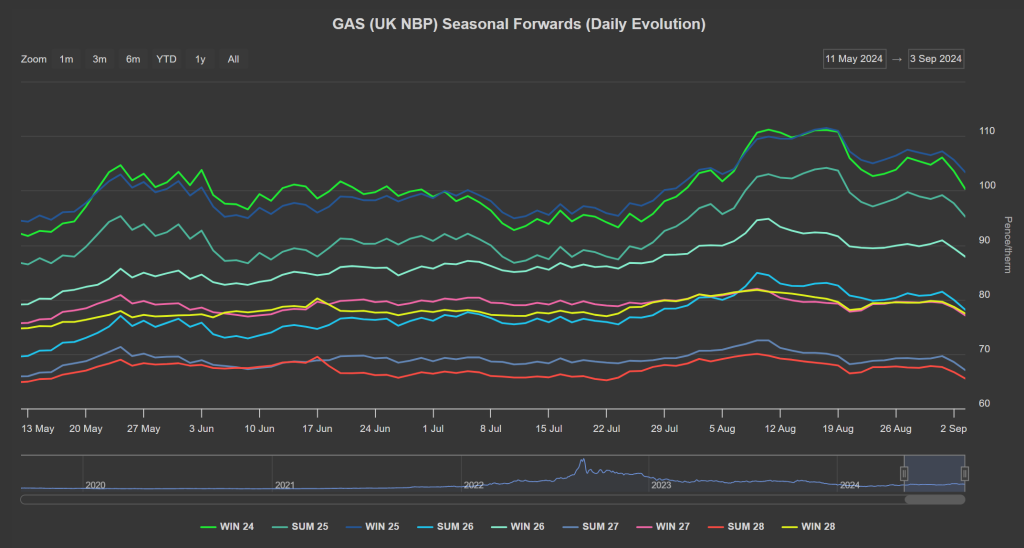

It’s been a bearish session today with Winter-24 prices breaking below 100p/therm for the first time in over a month despite massively reduced Norwegian flows due to ongoing scheduled maintenance – with the Easington terminal offline until 16th September (meaning zero flows into the UK from Norway’s Langeled).

Analysts are citing bearish drivers as being confidence in historically high European storage levels coupled with very low industrial and domestic demand.

European storage is 93% versus the 5-year average of 82%.

Industrial and domestic demand across Europe is around 20% below average levels for the 2017 to 2021 period.

We’re expecting two more LNG arrivals to degasify at British terminals before 11th September which should provide a boost to supply (amid current supply constraints caused by Norway’s flows being offline).

European LNG send-outs are forecast to be more than 20% higher in September compared to August – further evidence of a drop in cooling demand throughout Asia.

Elsewhere it appears geopolitical risk premiums are easing with tensions in the Middle East and on the Ukraine-Russia border stabilising (for now).

Clients with significantly open volumes for Winter-24 are in the minority – with most having opted to heavily hedge Positions with winter conditions now on the horizon.

Monthly Day-Ahead averages so far this month are on target to achieve 93p/therm (or approx. 3.1p/kwh excluding non-gas).

ELECTRICITY & CARBON

On the carbon markets, the benchmark EUA Dec ’24 contract sold off yesterday, finally breaking below the psychological €70/tonne support level – closing at €68.16/t after losing -3.22%.

Carbon’s bearish momentum has been atttributed to the decline of gas prices, thought the increased nuclear generation target from EDF certainly played a role, as it is the confirmation that thermal assets are losing further ground to low carbon energy sources for the upcoming months.

High temperatures across Europe are still expected to persist until this weekend, especially in Germany.

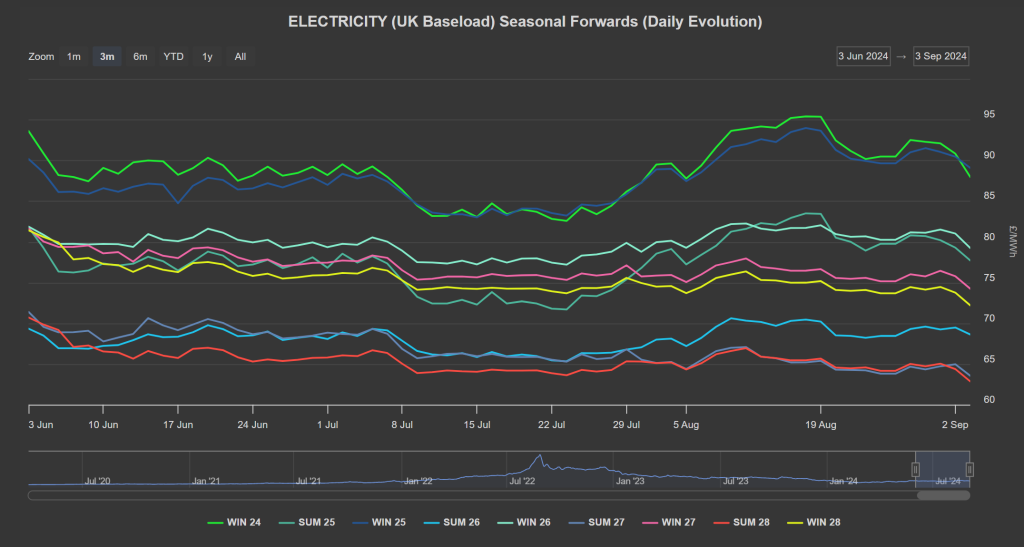

Down the curve, Forward prices also sold off yesterday as well – mirroring losses on both carbon and gas.

UKAs have finally recognised (and emulated) the falling value of their more heavily traded European counterpart, having dropped to £41/tn today from £43/tn yesterday.

Our electricity generation mix is bullish in nature today with renewables contributing 15%, thermal at 47% (gas and coal) and low carbon at 25% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £83/mwh (or approx. 8.3p/kwh excluding non-energy).