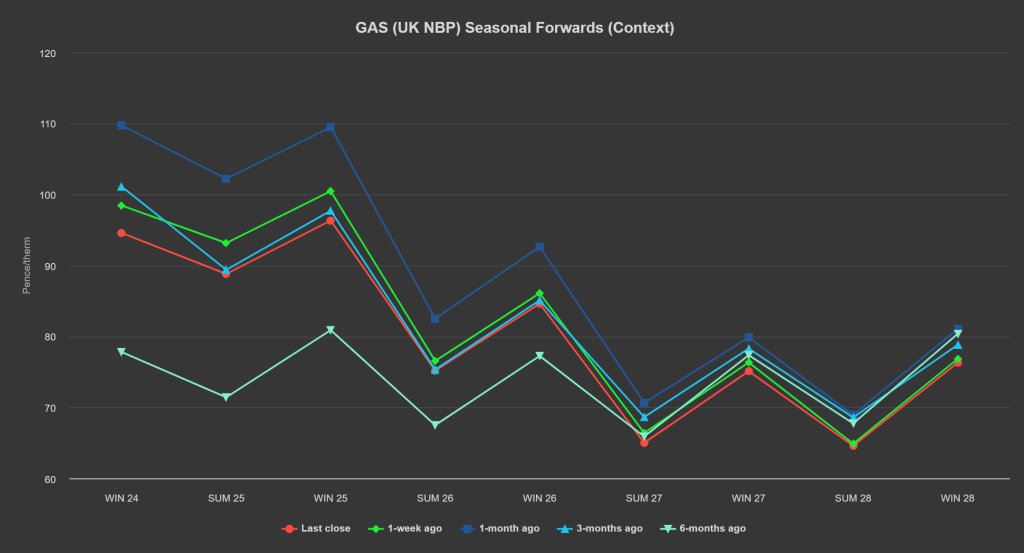

Notably, the front three seasons (Winter-24/Summer-25/Winter-25) closed yesterday down on the week/the month/3-months ago (see chart below).

Winter-24 is at a marginal discount to Winter-25, reflecting risk-premium well into next year (given it looks unlikely that Russia will renew its contract to supply gas into Western Europe via Ukraine – tightening supply).

This week has seen steadily improving values – primarily at the front of the curve.

High storage, benign weather conditions, improved LNG arrivals, “calmer” geopolitical disquiet could all be drivers attributing to this late Summer-24 bearish rally.

In truth, it’s more likely that bullish factors have been “baked-in” over the last few months, and now traders are selling off prior to the onset of Winter-24.

Clients with remaining open volumes for Winter-24 are encouraged to assess the value on offer versus the highs we saw back in mid-August.

Thankfully, after making landfall in Louisiana overnight, Hurricane Francine has now been downgraded to a tropical storm limiting fears of disruption to US LNG export plants.

Ongoing Norwegian maintenance persists, and weather related demand increases, are further contributing to supply tightness.

Storage withdrawals have ramped up significantly in order to meet demand (meaning European storage is now down to 93% versus the 5-year average of 85%).

Bears will be pleased to hear that temperatures are expected to lift back up above seasonal norms next week.

Capacity currently offline due to scheduled Norwegian maintenance events is expected to be re-introduced into the system from next Friday (easing supply tightness/limiting storage withdrawals).

Egypt continues to eat up LNG arrivals increasing global competition for cargos in advance of winter conditions.

Hitherto, Egypt was largely energy independent – however, as its own natural gas production falls and power demand climbs, the country’s position as a natural gas exporter over recent years (as part of a plan to become a reliable supplier to Europe) looks destined to end.

In other news, Australia (one of the largest exporters of natural gas worldwide), plans to begin shipping green hydrogen overseas by 2023 in an effort to accelerate the slow-moving global market for the low-emission fuel.

Monthly Day-Ahead averages so far this month are on target to achieve 88p/therm (or approx. 3p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, European short-term delivery prices are geographically disparate with Germany’s price approx. €40/mwh more expensive than their French counterpart today.

Despite lower tempertures and shorter days, solar generation remains significant and is allowing intraday prices to dip.

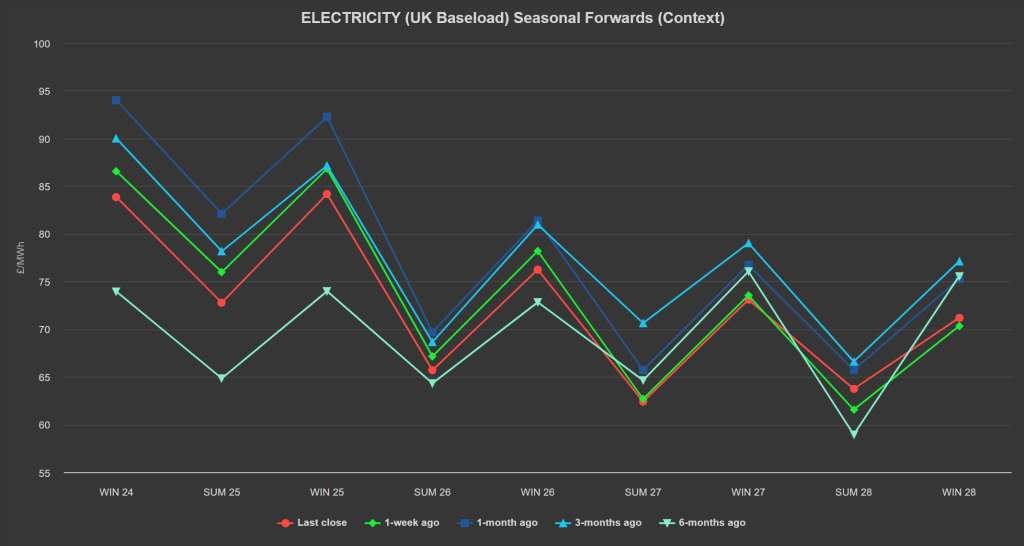

Down the curve, Forward prices have continued to trade lower, mirroring the bearish momentum of EUAs and gas.

On the carbon markets, the EUA Dec ’24 benchmark lost over 1.43%, closing at €65.45/tonne.

September is Europe’s compliance month, and so market participants had expected stronger buying boosted by late mandatory credit buyers – it has yet to materialise!

Back in the UK, UKAs are holding steady around £42/tonne.

Our electricity generation mix has been bearish in nature today with renewables contributing 35%, thermal at 20% (gas and coal) and low carbon at 25% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £76/mwh (or approx. 7.6p/kwh excluding non-energy).