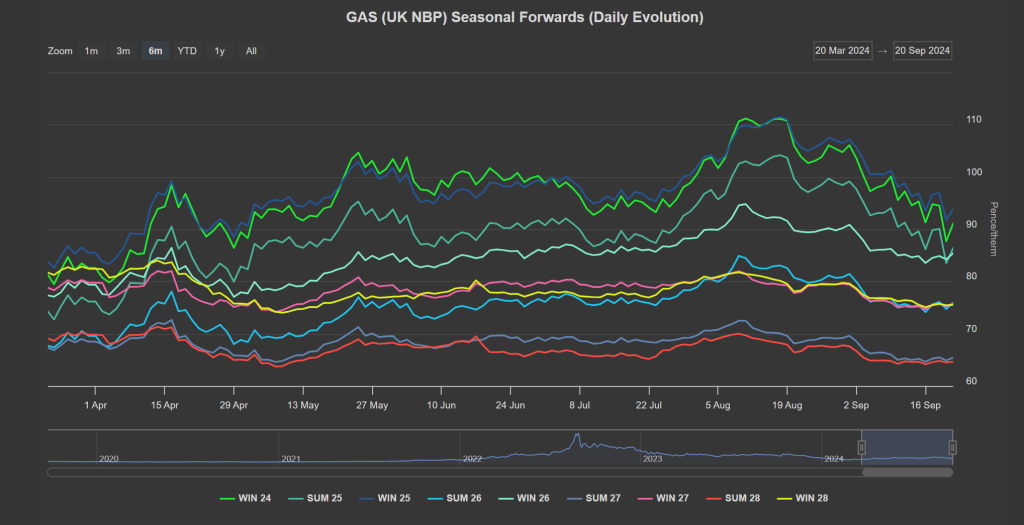

With only 7 days of Summer-24 remaining, price-action continues to buck traditional norms with front-end Seasonal Forwards having fallen approx. 50% over the latter stages of Winter-23 (Dec ’23 to Feb ’24), only then to rise gradually thereafter until mid-Aug ’24 before falling back 25% off the back of late summer profit taking/repositioning (see Seasonal Forwards “Daily Evolution” at foot of GAS report below).

To put it another way, we’ve had falling prices in winter, followed by rising prices across the summer – only then to fall with winter conditions on the horizon!

The UK system was short at this morning’s open (demand forecast outstripping supply) – as such, prices started higher and have subsequently fallen back again.

With winter now nearly upon us, market participants will surely begin to eye the potential supply impacts of geopolitical tensions across the Middle East and Eastern Europe.

Consensus points toward Moscow preparing to attack Ukraine’s nuclear infrastructure with a view to Ukraine being forced to abandon its sustained counter-invasion of the Kursk region (the location, of course, of the transit point for the Sudzha pipeline).

Israel has followed-up last week’s “device” attacks with an escalation of airstrikes on Hezbollah’s positions across Lebanon.

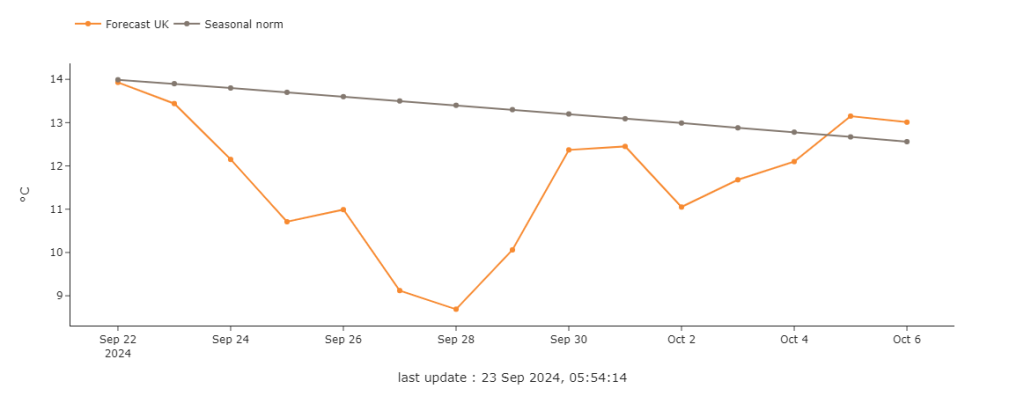

Looking to more local drivers, lower temperature forecasts look set to increase heating demand:

UK Temperature Forecast

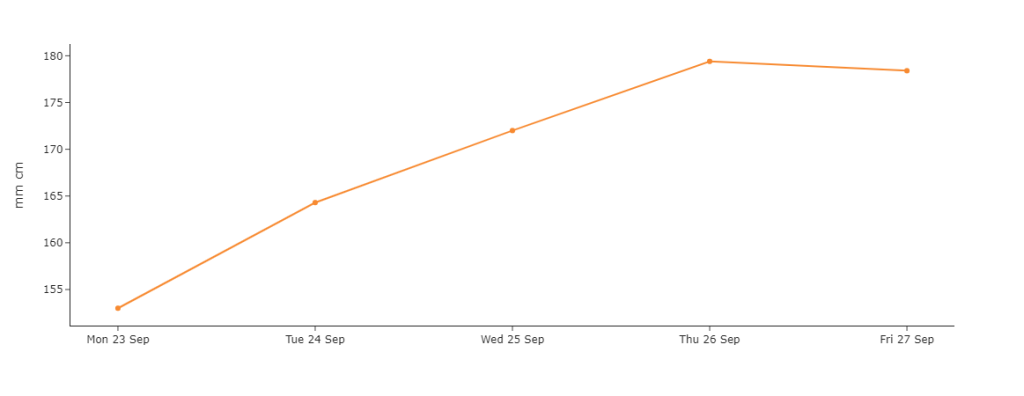

UK 5-day gas demand forecast

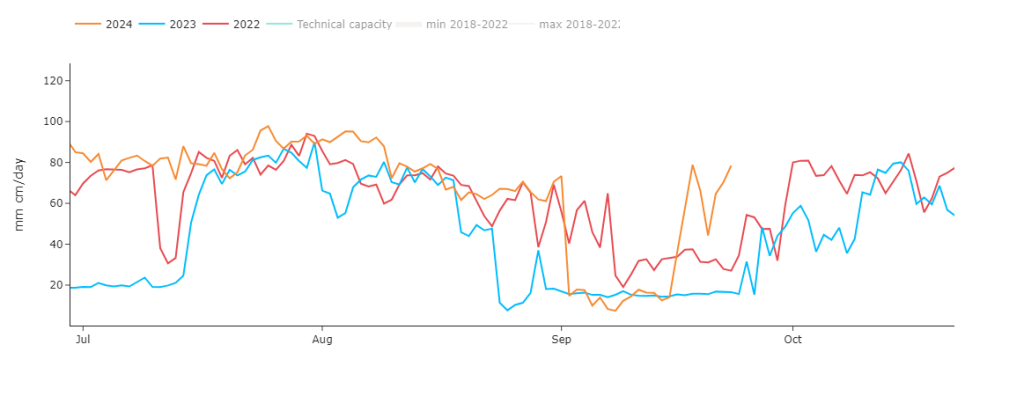

Norwegian maintenance has all but ended with flows through Langeled to the UK now back online in earnest (with scheduled maintenance having ended earlier than ’23 & ’24):

Norwegian gas exports to the UK

The lion’s share of remaining European offline capacity is expected to resume next week barring any last-minute extensions to maintenance.

Clients with significantly open volumes for Winter-24 are now very much in the minority – with most having opted to heavily hedge Positions with winter conditions now only a week away.

Monthly Day-Ahead averages so far this month are on target to achieve 85.8p/therm (or approx. 2.928p/kwh excluding non-gas).

ELECTRICITY & CARBON

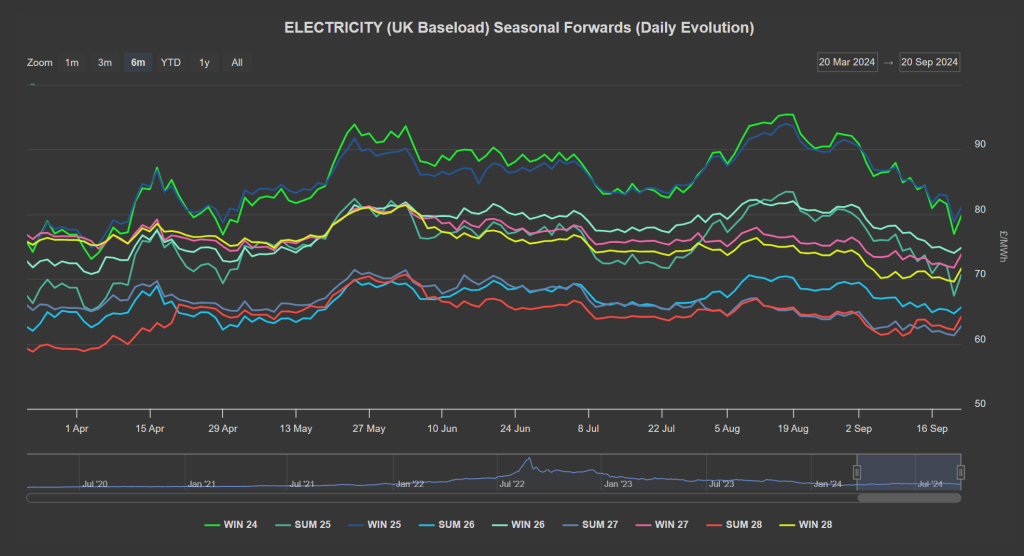

With only 7 days of Summer-24 remaining, price-action continues to buck traditional norms with front-end Seasonal Forwards having fallen approx. 50% over the latter stages of Winter-23 (Dec ’23 to Feb ’24), only then to rise gradually thereafter until mid-Aug ’24 before falling back 30% off the back of late summer profit taking/repositioning (see Seasonal Forwards “Daily Evolution” at foot of ELECTRICITY report below).

Looking to the continent for market drivers, temperatures will fluctuate around seasonal averages over the coming week, with a cold spell expected on Friday and over the weekend in Central-Western Europe.

Wind generation outlook has been revised to calmer conditions, but periods of high output are still expected, particularly in Germany, starting tomorrow’s night until Saturday.

Solar generation is forecast to be unstable this week due to low-pressure systems, with low production likely on some days.

Wet conditions in Central-Western Europe will support increased run-of-river production and snowfall in the northern Alps, with a high chance of seasonal to above-normal precipitation continuing next week.

On the Carbon markets, EUAs rebounded on Friday, off the back of a rebound in gas prices, following a volatile session on Thursday due to an as-yet-unconfirmed Ukraine-Azerbaijan deal transit extension.

EUAs were still down 2% on the week nonetheless with the Dec ’24 benchmark contract closing at €63.39/tonne.

Down the European electricity curve, prices rebounded to finish the week following the uptick in gas and carbon prices.

As predicted last week, UKAs are retesting £39/tonne which marks the bottom of a confirmed daily descending trend channel – both EUAs and UKAs are now in a bearish trend.

Our electricity generation mix is bullish in nature today with renewables contributing 19%, thermal at 43% (gas and coal) and low carbon at 22% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £77.994/mwh (or approx. 7.8p/kwh excluding non-energy).

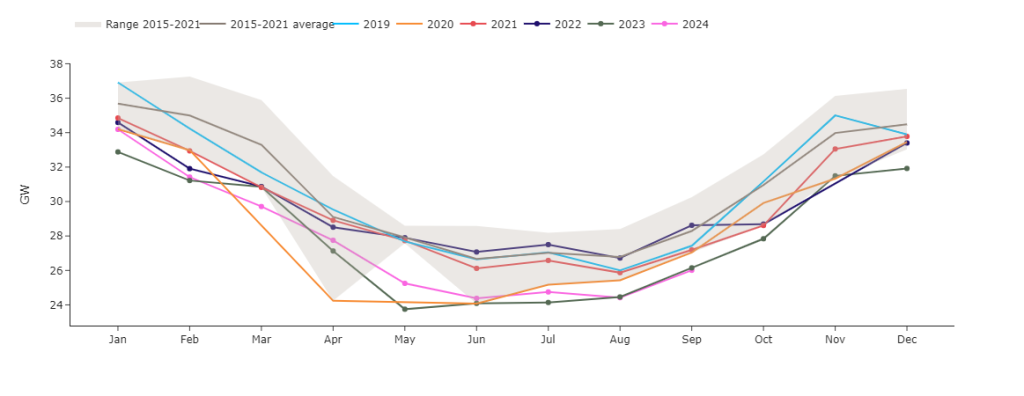

Power load demand has begun its upward trajectory heading into Winter-24: