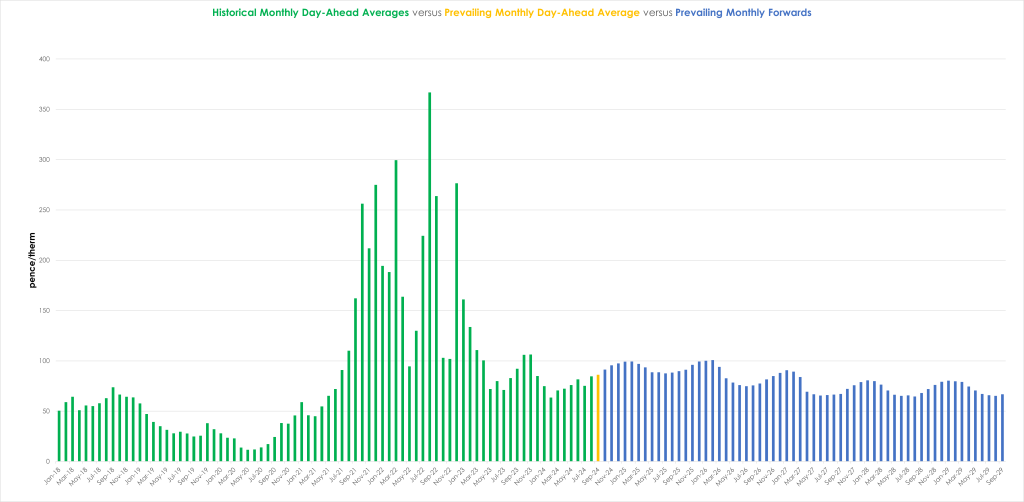

Looking at prevailing Monthly Forwards (blue bars) versus historical Monthly Day-Ahead averages (green bars), it’s worth noting how far the markets have fallen since the volatility began in Jul-21 (ending in May-23) – see chart below.

Near-term delivery has been a little more bullish today off the back of increased demand and extended Norwegian outages.

Flows through Langeled remain low and have dropped 3 million cubic metres day on day, contributing to fears over supply tightness.

The UK system opened short today (demand forecast outstripping supply), this despite reduced gas-for-power burn off the back of improved wind outputs.

Colder temperatures have ensured that LDZ demand (heating) is on the up with temperatures only expected to climb back above seasonal norms at the turn of the month.

On the supply side, mixed demand signals from Europe have resulted in an increase of LNG cargos idling at sea waiting for degasificiation.

Notably, Belgium is pushing for the EU to impose sanctions against Russian LNG (even though they have historically been one of Europe’s main importers of the gas).

Belgium’s Energy Minister has claimed that until the EU as a whole imposes sanctions, businesses are unable to terminate long-term agreements (commitments).

The regulations imposed by Brussels in December of last year have failed to stop Russian energy corporations from using EU infrastructure, nor have they provided adequate legal grounds for companies to reduce contracts.

On the hedging side, with only 4 days remaining of Summer-24, clients with partial open volumes for Winter-24 are eyeing Day/Month-Ahead performance with a view to hedging additional volumes as the winter season progresses.

Monthly Day-Ahead averages so far this month are on target to achieve 86.133p/therm (or approx. 2.939p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, the northerly flow will provide windy conditions in the coming days with high generation spikes expected.

Solar generation should increase in the coming days but will drop off next week.

Hydro-wise, very wet conditions are forecast in CWE this week, supporting increasing run-of-river production with another round of snowfalls over the northern Alps.

Temperatures are expected to drop this weekend but a rapid warming is expected after the weekend.

EDF has stopped its Cattenom-1 nuclear reactor to save fuel and extended maintenance at Paluel-4.

The two measures combined will reduce nuclear output by around 250 GWh this week and next, amid generally bearish supply-and-demand fundamentals.

On the carbon markets, EUA prices have mirrored gas increases.

As predicted last week, UKAs retested £39/tonnes (the lower extremity of a confirmed daily triangle formation) and have now broken below currently printing approx. £37/tn.

Fundamentally, the fall is being attributed to market participants’ reaction to UK policy review (or the Free Allocation Review).

The outcome being that the expected scarcity of UKAs come 2026 has now been puished back to 2027 – no doubt resulting in speculators reducing long (buy) exposure.

As such, UKA values dropped 8% today – we may see more downside over the coming weeks with an auction set for 2nd Oct.

£33.50/tn is a viable target to the downside.

Our electricity generation mix is bearish in nature today with renewables contributing 39%, thermal at 22% (gas and coal) and low carbon at 20% (nuclear and imports).

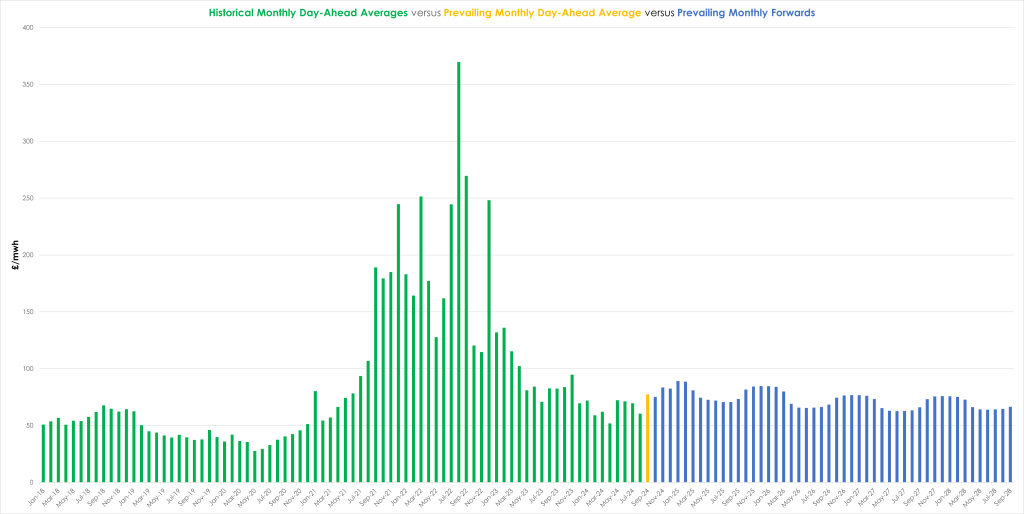

Monthly Day-Ahead averages so far this month are on target to achieve £77.302/mwh (or approx. 7.7302p/kwh excluding non-energy).