Markets finished on a decidedly bullish tone on Friday, and have continued to post gains this morning.

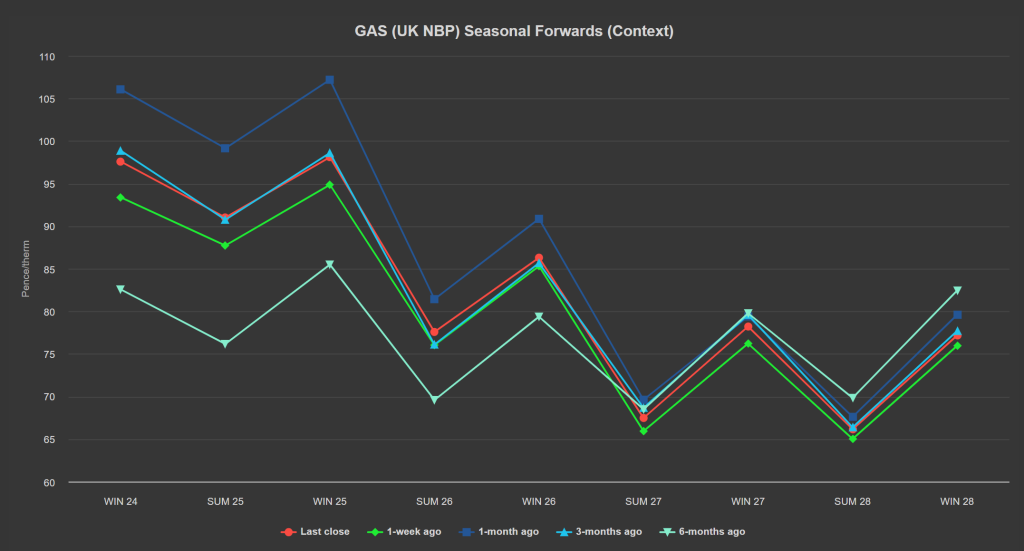

Seasonal Forwards are up on the week, down on the month (see chart below).

The UK system has opened short (demand forecast outstripping supply).

Ongoing scheduled maintenance and lower temperatures are supportive to the upside.

An unplanned outage at Asgard is restricting 7 million cubic metres of Norwegian flow.

LDZ demand is nominating at 103mcm, with temperatures marginally below seasonal norms today.

On the hedging side, all eyes are on Day-Ahead/Month-Ahead performance with Winter-24 beginning tomorrow.

Monthly Day-Ahead averages so far this month are on target to achieve 87.1p/therm (or approx. 3.173p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, near-term delivery prices are low reflecting very high wind outputs.

On the weather side, temperatures will be near normal on the short-term, cooling by the end of the week, then warming again next week.

Wind generation will be strong tonight, calming mid-week, with potential for increased activity next week.

Solar generation in Central Western Europe will be limited for the next few days, improving from Thursday, but may decrease next week due to low-pressure systems.

On the carbon markets, prices were slightly decorrelated from gas prices on Friday.

Gas climbed slightly while the EUA benchmark Dec ’24 contract lost 0.29% – closing the day, and the week, at €66.33/tonne, signing an overall gain of +4.64% week-on-week.

Conversely UKAs dropped below and out of the triangle, and broke below the mid-August lows on good bearish volume.

£33.50/tonne is now a far-off (but viable target) to the downside marking an area of confluence (historical low plus lower extremity of descending trend channel) – see technical chart below.

Fundamentally, the fall in UKAs is being attributed to market participants’ reaction to UK policy review (or the Free Allocation Review).

The outcome being that the expected scarcity of UKAs come 2026 has now been puished back to 2027 – no doubt resulting in speculators reducing long (buy) exposure.

As such, UKA values dropped 10% last week – more downside would seem likely over the coming weeks with an auction set for 2nd Oct.

Our electricity generation mix is bearish in nature today with renewables contributing 40%, thermal at 23% (gas and coal) and low carbon at 19% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £72.375/mwh (or approx. 7.2375p/kwh excluding non-energy).