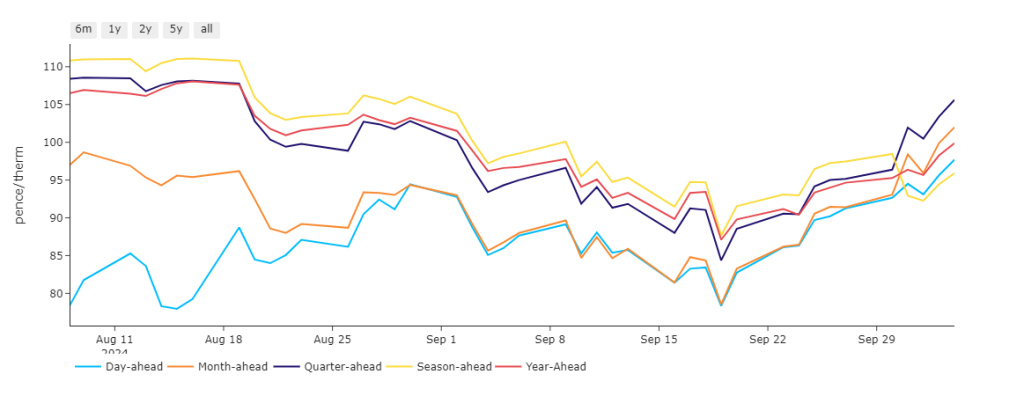

Whilst Day-Ahead remains the least expensive way to buy gas, it’s worth noting that near-term delivery has begun the Winter-24 season on a bullish note (see chart below).

With the onset of Winter-24, geopolitical events seem to be the focus of bullish fervour – with concerns persisting over disruptions to exports and key transit routes across the Middle East (and Eastern Europe).

Market participants are watching closely to see how Israel might respond to Iran’s recent ballistic missile attack.

On the supply side, the ongoing outage at Troll (taking 13 million cubic metres of Norwegian flow offline) is also a major supportive driver this morning.

Our system opened short this morning (demand forecast outstripping supply) – though total demand is on par with seasonal norms.

Temperature forecasts are showing a dip below seasonal norms this weekend, but should be back up above seasonal norms come mid-month.

Monthly Day-Ahead averages so far this month are on target to achieve 96.903p/therm (or approx. 3.306p/kwh excluding non-gas).

ELECTRICITY & CARBON

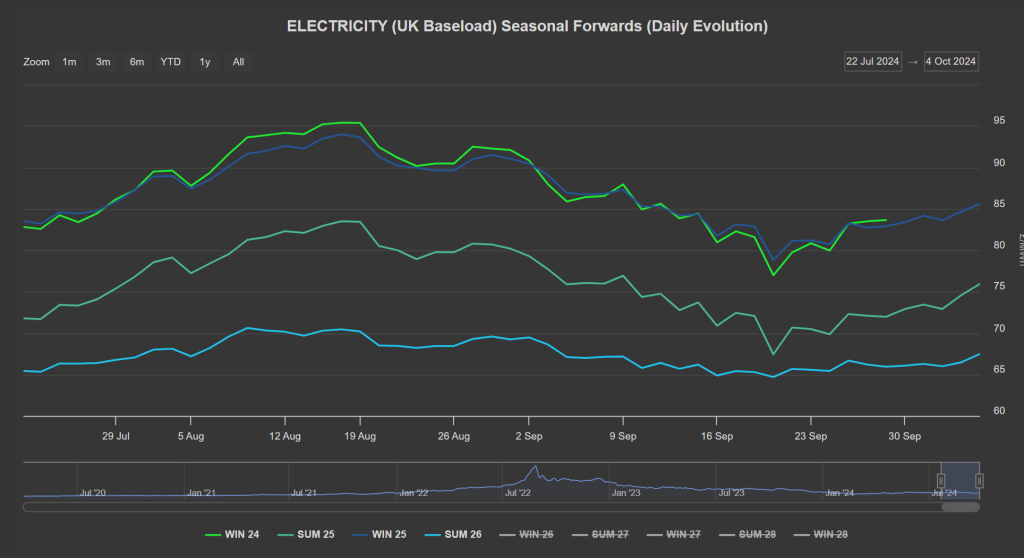

With Winter-24 having now begun, the Front Seasons (Summer-25/Winter-25/Summer-26) are turning ominously Northwards (see chart below).

In typical winter-fashion, prices down the curve are starting to stretch, with Summer-26 posting a 21% discount versus Winter-25.

Looking to the continent for price direction, cyclone Kirk is providing warmer conditions this week across Central Western Europe, where 3°C above normal is forecast for tomorrow in Germany.

EUAs closed in a downtrend last week – low demand for credits resulting in a decoupling from surging gas prices.

The bearish trend continues at the time of writing, the Dec’24 benchmark contract already having lost an additional -2.26%.

Back in the UK, UKAs are also very much in a downtrend having dropped below and out of the confirmed daily triangle pattern, then breaking below the mid-August lows on good bearish volume.

£33.50/tn is now a viable target to the downside marking an area of confluence (historical low plus lower extremity of descending trend channel) – see 30th Sep’s technical chart here.

Fundamentally, the fall in UKAs is being attributed to market participants’ reaction to UK policy review (or the Free Allocation Review).

The outcome being that the expected scarcity of UKAs come 2026 has now been puished back to 2027 – no doubt resulting in speculators reducing long (buy) exposure.

Last week’s auction cleared at £34.91/tn.

Our electricity generation mix is bearish in nature today with renewables contributing 40%, thermal at 22% (gas and coal) and low carbon at 20% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £81.976/mwh (or approx. 8.1976p/kwh excluding non-energy).