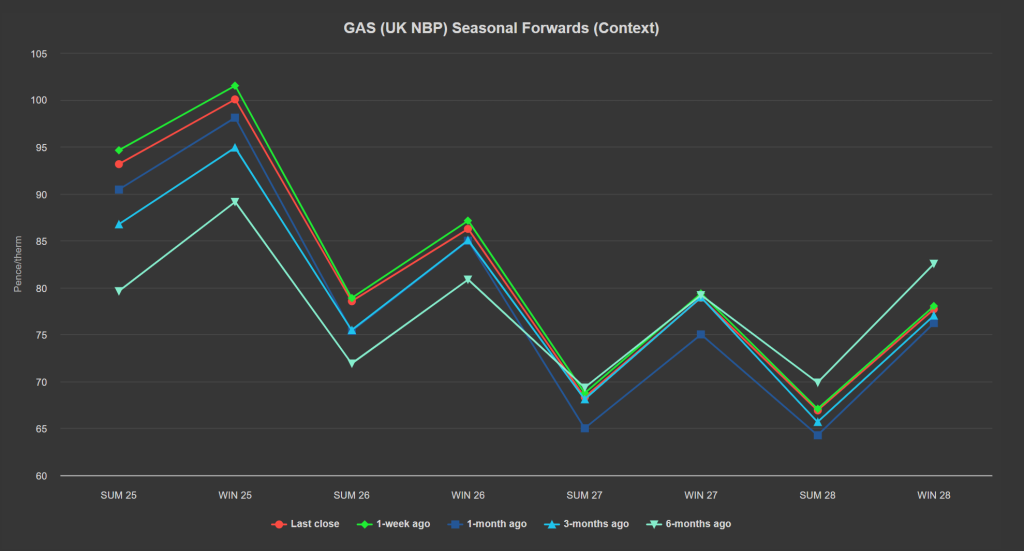

Seasonal Forwards are down on the week, but up on the month/3 months ago/6 months ago (see chart below).

Markets are flat today amid a long UK system (supply outstripping demand forecast).

Geopolitical risk premium persists with the ongoing threat of further escalation across the Middle East and the ever-present supply worries linked to Eastern Europe.

US and Israeli governments met yesterday to discuss next steps with regards Iran – the outcome remains unknown though Israel’s Defence Minister has suggested the retaliation will be “lethal and surprising”.

On the supply side, four more LNG arrivals are expected to degasify at UK ports by 15th November.

Unscheduled outages (blamed on compressor issues) persist at the Gullfaks and Asgard gas plants reducing Norwegian flows into Europe/UK.

However, the combination of healthy European storage levels (at 95% fullness verus the 5-year average of 91%) and temperatures forecast to rise back above seasonal norms by mid-month, continue to keep a lid on prices.

Globally, some nations are crying out for fresh gas supplies – with Germany not seeing sustained quarterly growth since 2022.

Whilst Europe’s last two winters have been exceptionally mild, the colder temperatures already being forecast this season will likely heighten competition with Asia for global LNG – ultimately resulting in shortages for countries unable to purchase them (scarcity of course means higher commodity prices).

Monthly Day-Ahead averages so far this month are on target to achieve 96.871p/therm (or approx. 3.305p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent for price signals, EUAs briefly dipped below €60/tn yesterday.

The benchmark Dec’24 contract closed the day at €62.01/tn, gaining overall 2.85% on the day.

Amid unsupportive fundamentals, we could see a short lived rebound to the daily MAs (with a cluster around €63.6/tn), before moving back lower towards €60/tn as the downtrend is expected to continue.

UKAs are on a bullish retracement having tested £35/tn on the mid-price – now at £38/tn – though next week’s auction settlement (if low) will bring about a continuation of the downtrend.

Wind generation aross Europe (especially Germany) will likely bring about some negative intraday pricing.

Clouds will limit solar output for the next week or so.

Rain is forecast to soak Southern and Central Europe before the weekend, boosting hydro production.

EDF has warned of the impact of two potential events:

1) Potential flooding in the Durance valley in the Alps from 8th Oct, significantly reducing hydro capacity.

2) A delay restarting three nuclear plants by a combined 14 days amid a depreciated price environment (so as not to flood the market with over-supply and further depress value).

Back in the UK, our electricity generation mix is bearish in nature today with renewables contributing 44%, thermal at 24% (gas and coal) and low carbon at 17% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £81.141/mwh (or approx. 8.1141p/kwh excluding non-energy).