Nearly a month into Winter-24 and it’s been a bullish week amid a dearth of LNG arrivals, persistent unscheduled Norwegian outages, and flip-flopping weather forecasts.

At the time of writing, the front month (Nov-24) contract is pricing at 108.50p/th, another rise of 2p/therm versus yesterday’s close.

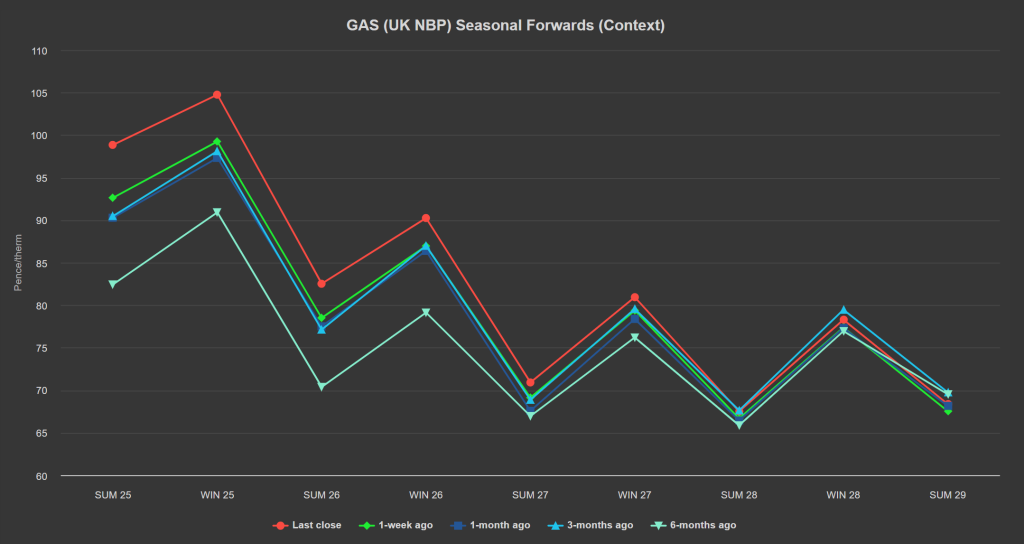

Seasonal Forwards are up on the week/month/3-month/6-month (see chart below).

This week has seen weaker “feedgas” flows at major US facilities (feedgas being the natural gas that is delivered to a liquefaction facility via pipeline to be converted into LNG).

This will undoubtedly mean less LNG coming to Europe/UK in the coming days/weeks.

Outages at Sleipner and Oseberg are taking a combined 16milion cubic metres of Norwegian flow offline – but flows look set to ramp up to maximum capacity over the coming days.

Warm conditions have meant low heating demand this last few weeks.

However, contrary to previous consensus (and depending on which weather forecast you place the most stock in), lower temperatures (and higher heating demand) now look on the cards for early next month.

This coupled with wind outputs below seasonal norms for the next couple of weeks will increase gas for power demand.

The premium on UK gas (NBP) prices over and above the European benchmark (TTF), is supporting strong imports into the UK from the continent.

It’s fair to argue that European prices need to rise to attract more LNG cargos to our waters (and away from Asia).

Solid European storage at 95% (versus the 5-year average of 92%) is helping to diminish bullish momentum.

Notably, Russia’s pipeline exports to China are up 40% y-o-y – meaning Russia is now exporting more gas to Asia than it does Europe.

It’s likely these exports will increase still further with the completion of the Far Eastern pipeline in 2027.

However, Chinese demand remains in question, with recent economic indicators reinforcing fears of deflation and the need for meaningful stimulus measures – though the Communist Party remain reluctant to devalue the yuan and trigger capital flight (which seems inevitable).

Monthly Day-Ahead averages so far this month are on target to achieve 97.645p/therm (or approx. 3.332p/kwh excluding non-gas).

ELECTRICITY & CARBON

Notably, last week highlighted the strain on power supply when National Grid triggered a market notice (with overall capacity falling short of demand).

At the time, nuclear generation was very low due to unplanned outages and delays in restarting units – though capacity is expected to recover by month-end.

This supply tightness has been coupled with IUK (the interconnector with France) being at only 25% capacity – it broke down back on 10th Oct and is not due to be restarted until 17 November.

On the carbon markets, EUAs continued their uptrend yesterday as they gained another 2.68% off the back of a short-squeeze (the unwinding of sell positions by rising price hitting sellers’ protective stop losses).

Conversely, UKAs are down 1.75% versus yesterdays close at £39.30/tn – poised to break below an intraday rising trend channel on the hourly charts (see chart below).

Average True Range (reflecting trend strength) is rising to suggest the downtrend has legs.

MACD is is negative and falling (further confirming downtrend on lower timeframes).

Fundamentally, the fall in UKAs over the summer was attributed to market participants’ reaction to UK policy review (or the Free Allocation Review).

The outcome being that the expected scarcity of UKAs come 2026 has now been pushed back to 2027 – resulting in speculators reducing long (buy) exposure.

However, the recent bull run was evidence of investors scaling back-in at lower levels given the great value on offer compared to the Sep-24 highs.

Our electricity generation mix is bullish in nature today with renewables contributing 15%, thermal at 49% (gas and coal) and low carbon at 21% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £81.653/mwh (or approx. 8.1653p/kwh excluding non-energy).