Prices have softened this morning following yesterday’s surge in near-term delivery prices.

Bullish, wintry fervour can be attributed to lower temperature forecasts (increasing heating demand); poor wind output expectations for the remainder of the month (increasing reliance on gas-for-power burn); and renewed risk of disruption to the the last vestige of Russian pipeline gas supplies transitting via Ukraine into Europe (see chart below for Russian gas flows at the Sudzha entry point in Ukraine).

Ukrainian President Zelensky has confirmed a build up of circa. 50,000 Russian troops in and around the Kursk region suggesting an imminent counter-offensive is in the offing.

Of course, any escalation in this region poses a risk to the pipeline infrastructure at the entry point in Sudzha.

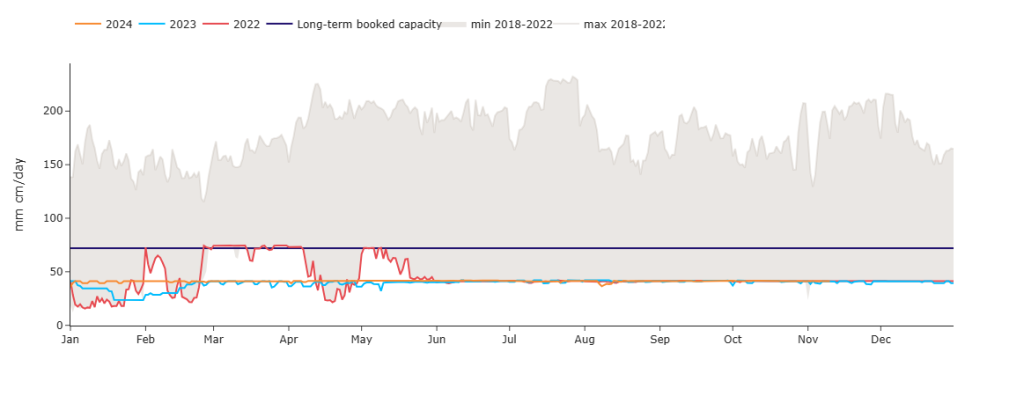

European storage fullness has dropped from 94% last week to 93% (versus the 5-year average of 89%).

Some of the market’s bullish momentum is being offset by steady Norwegian gas flows to the UK/Europe, which remains above the 5-day moving average.

In other news on the supply side, with Western sanctions starting to bite, Russia’s Artic LNG 2 facility has reduced its gas supply to almost zero this month.

The LNG facility’s gas fields have seen a 90% decrease from the facility’s average output last month – meaning a significant drop of gas in the European system.

Our gas in the UK will likely remain at a premium versus Europe’s as the winter progresses – otherwise, we’ll not continue to attract the cargos.

This premium is always exacerbated by structural problems in the UK’s gas system resulting in high transmission costs and, of course, a lack of storage compared to Europe – meaning the UK needs to offer a much higher price to secure supply.

Monthly Day-Ahead averages so far this month are on target to achieve 103.1p/therm (or approx. 3.518p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent in more detail, EUA prices were down yesterday, they lost -0.66% and closed at €67.57/tn.

UKAs have mirrored EUAs’ drop, though have still yet to retest the lows of 8th Oct – currently sitting at £38.27/tn on the mid-price.

European gas has moved higher however, so it appears yesterday’s downward electricity move was due primarily to weather forecast revisions.

Indeed, both warmer and windier conditions across Europe should limit short-term emissions from power generation (hence EUAs’ bearish bias this week).

In contrast to the UK, strong winds across Europe will continue next week – especially in Germany.

Solar output will be limited by morning fog in the coming days, dropping to lower levels next week.

Meanwhile, hydro conditions are turning wetter next week across France, Spain, and Italy, which should lead to increased run-of-river production.

The strong wind generation outlook should provide downward pressure on prices, partially offset by below-normal temperatures in the UK.

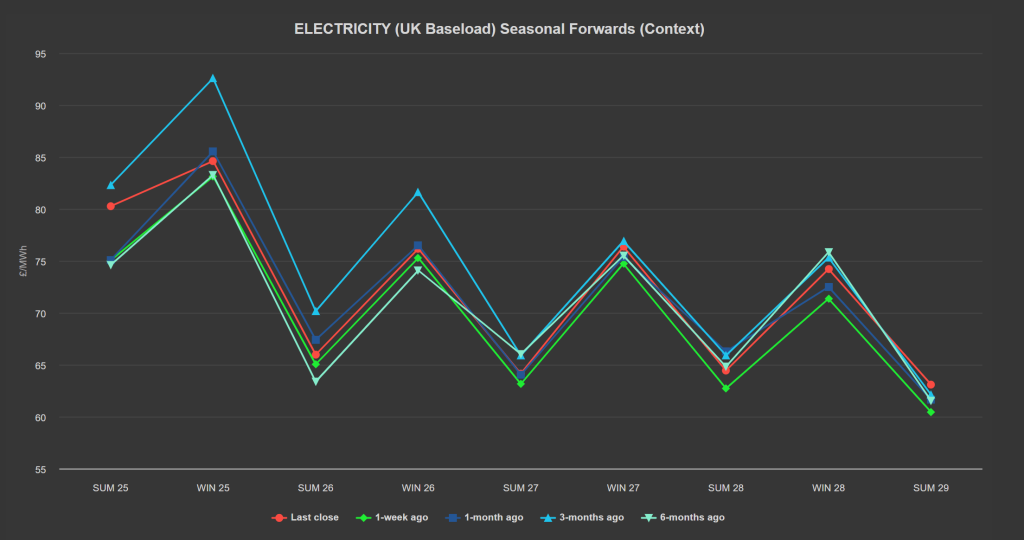

Down the European curve, Forwards are up, following the strong rise in gas prices.

Back in the UK, Summer-25 prices jumped significantly yersterday reflecting wintry sentiment (not a good time to be hedging Seasonal Forwards).

Our electricity generation mix is bullish in nature today with renewables contributing 28%, thermal at 44% (gas and coal) and low carbon at 20% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £102.818/mwh (or 10.28p/kwh excluding non-energy)