Markets have reacted bullishly to Russia firing an intercontinental ballistic missile (ICBM) at Ukraine – with tensions escalating after 33-months of relative stalemate.

ICBMs are, of course, strategic weapons designed to deliver nuclear warheads – so this retaliatory response to Ukraine having fired US-made weapons at Russia this week is no doubt the Kremlin’s way of reminding European countries of Russia’s nuclear capabilities.

Early reports suggest the missile was fired from the Russian region of Astrakhan, more than 700 km (435 miles) from Dnipro in Ukraine.

Both near- and far-term delivery is up – with Month-Ahead at 121.46p/therm at the time of writing.

All eyes are on the Sudzha transit point, and whether this latest incident will impact Russian flow currently transiting via Ukraine.

Prices are also being supported by outages at the Karsto gas plant in Norway amid the recent wintry increase in demand.

Subsequent to necessary withdrawals, European storage levels (now at 90%) are 1% lower than the 5-year average (91%).

However, recent LNG flows away from Asia and into Europe are tempering fears over supply shortages.

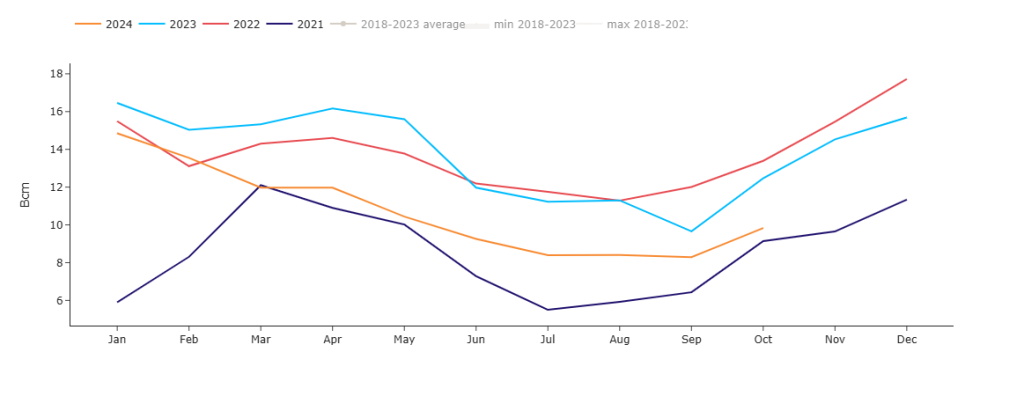

Thankfully, LNG arrivals to European shores are forecast at a 25% increase w-o-w, and are expected to be at levels not seen since Feb-24 by month-end (see chart below).

UK prices will likely remain at a premium versus Europe’s as the winter progresses – otherwise, we’ll be left high and dry where LNG arrivals are concerned.

This premium is always exacerbated by structural problems in the UK’s gas system resulting in high transmission costs and, of course, a lack of storage compared to Europe – meaning the UK needs to offer a much higher price to secure supply.

Monthly Day-Ahead averages so far this month are on target to achieve 108.633p/therm (or approx. 3.707p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, Carbon prices dropped off yesterday notwithstanding higher gas prices.

The COT (Commitment of Traders report) published yesterday showed that speculators have further increased their long (buy) positions.

Nonetheless, in the afternoon session, prices moved lower most likely off the back of profit taking pending the next bullish leg up.

UKAs have been enjoying further downside until this morning when, despite having broken below key trendlines, Russia’s ICBM attack instigated a significant bounce (see chart below).

The UK’s electricity generation mix is bullish in nature today with renewables contributing 31%, thermal at 46% (gas and coal) and low carbon at 16% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £101.643/mwh (or 10.16p/kwh excluding non-energy).