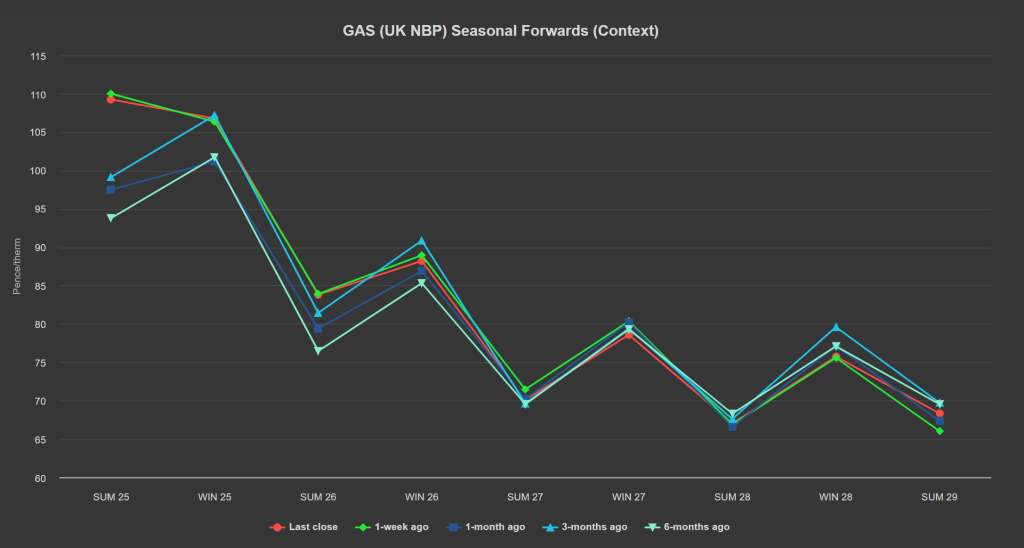

Notwithstanding supportive drivers (Ukraine/Russia transit deal due to end; lower temperatures meaning significant storage withdrawals; ongoing geopolitical uncertainty), front Seasons are marginally down on the week (see chart below).

Prices are drifting sideways again today amid the impacts of the Israel/Hizbollah ceasefire which is just about holding; warmer temperature forecasts and improved wind outputs limiting gas-for-power burn; gas withdrawals slowing.

In short, markets have found equilibrium for the time being – neither bears nor bulls have the upper hand.

Nonetheless, UK prices will likely remain at a premium versus Europe’s as the winter progresses – otherwise, we’ll be left high and dry where LNG arrivals are concerned.

This premium is always exacerbated by structural problems in the UK’s gas system resulting in high transmission costs and, of course, a lack of storage compared to Europe – meaning the UK needs to offer a much higher price to secure supply.

On the Carbon markets, EUAs edged lower yesterday with the Dec ’24 benchmark closing at €67.63/tn after losing 1.23% on the day.

It is being dragged down by slightly lower gas prices but fundamentally, we have seen lower emissions over the past days in the power sector thanks to above average wind levels.

This is set to continue next week, reducing demand in the short-term.

As we’d been predicting, UKAs saw another rally southwards beginning 21st Nov dropping as low as £35.56/tn yesterday on the mid-price.

Prices have since risen to £36.65/tn off the back of Compliance buyers bargain hunting at these low levels.

The UK’s electricity generation mix is bearish in nature today with renewables contributing 50%, thermal at 29% (gas and coal) and low carbon at 14% (nuclear and imports).