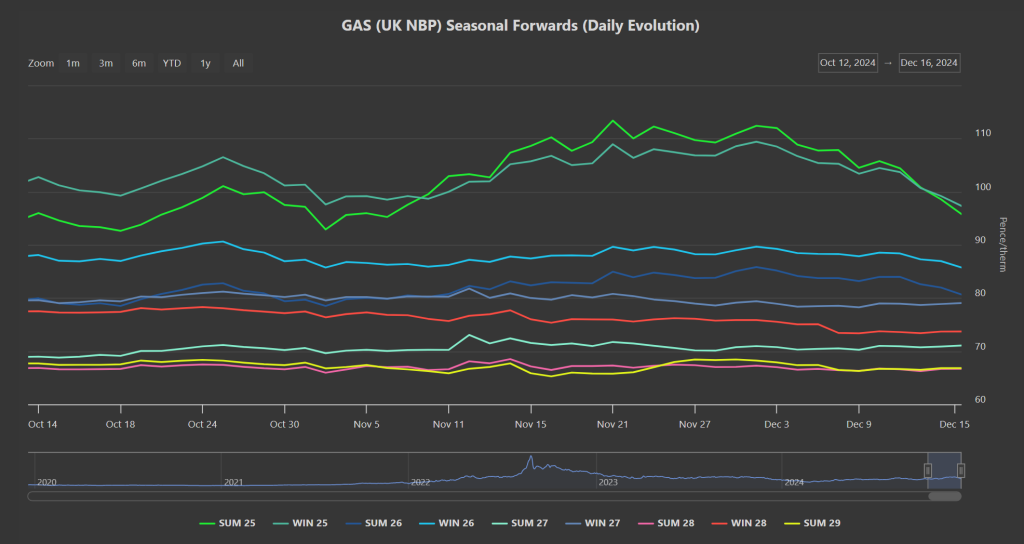

As we predicted back in early December (https://icdenergymanagers.com/tues-3rd-dec-24/), fears over replenishing Winter-25 storage were both premature and overcooked.

As of this week (off the back of warmer conditions, improved wind outputs), Summer-25 prices have fallen back below Winter-25 prices and relative order has been restored (see chart below).

That’s not to say that we should be complacent over Winter-25 storage, but to take the market higher this early was the work of bullish speculators, not genuine market dynamics.

Prices opened the week lower off the back of good sense prevailing, then trod water yesterday.

Today, it’s sideways price action again, with the front Seasons consolidating below the psychological level of 100p/therm.

Demand is back below seasonal norms, storage is at 78% versus the 5-year average of 77% (reflecting tempered withdrawals).

On the bullish side this morning, Norway’s three main gas processing facilities are suffering unscheduled disruptions.

On the bearish side, rumours abound that intense negotiations between Russia/Ukraine may in fact result in the retention of the transit deal into next year after all.

2025 is forecast to bring with it milder temperatures, limiting heating demand.

In short, prevailing conditions are now being reflected in more reasonable prices for both near- and far-term delivery.

Temperatures are up, wind is up, gas-for-power burn is down, European LNG arrivals are up, China’s LNG imports are down – so the bias is neutral to bearish.

The Russian central bank is expected to hike its key interest rate by another 200 basis points this week to 23% – evidently, Putin faces internal pressures heading into 2025 (which might be one of the reasons the Ukraine transit deal is back on the table – can the Kremlin afford to walk away from revenues?)

Monthly Day-Ahead averages are on the slide and on target to achieve 111.163p/therm (or approx. 3.793p/kwh excluding non-gas).

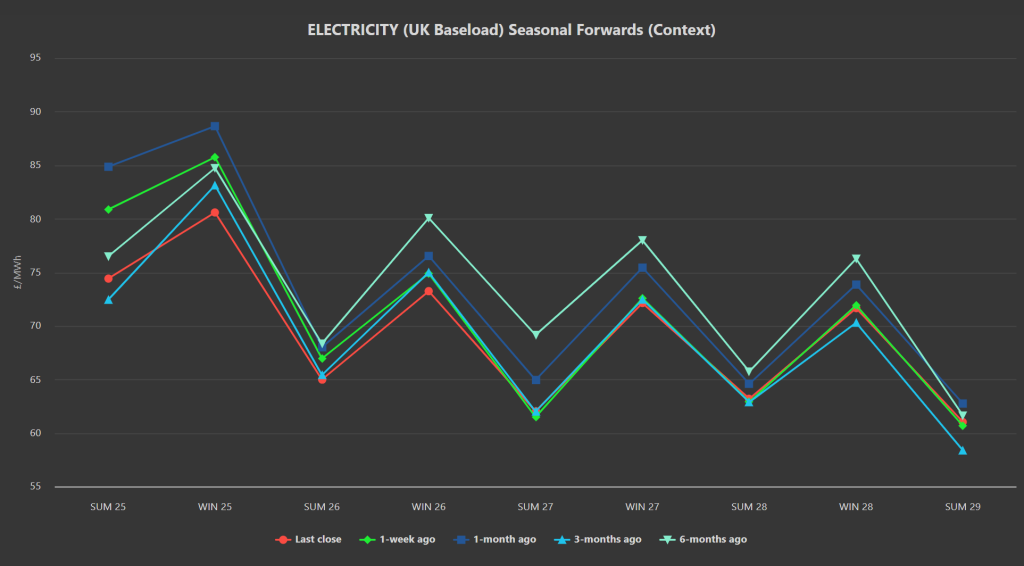

ELECTRICITY & CARBON

Seasonal electricity Forwards are down versus 1-week ago/1-month ago/6-months ago, and marginally up versus 3-months ago (see chart below).

So, to put it another way, the price buyers can access now for delivery in Summer-25/Winter-25/Summer-26/Winter-26 is lower than it was back in June (at the height of Summer-24) even though theoretically we’re approaching the height of Winter-24 – such have been the unpredictable impacts (that we’re still feeling) of the pandemic slow down in ’20/’21, closely followed by the loss of Russia’s gas flows into Europe (’21/’22).

Looking to the continent, windy conditions will persist this coming weekend, alongside predictably limited levels of solar generation.

On the Carbon markets, EUA (European Mandatory Allowances) Dec ’24 benchmark opened the week very low at €64.05/tn, with the most recent auction clearing at €63.6/tn off the back of a 1.47 cover ratio (a measure of the demand for EUAs relative to the number of allowances auctioned – a ratio below one indicates weak demand and a ratio above two indicates strong demand).

EUA Dec ’24 found a monthly low of €62.73/tn, before closing the day at €63.32/tn (-1.72%).

Back in the UK, our bearish predictions for UKAs have now come to pass with Dec ’24 delivery now at £33.38 on the mid (so late 33s on the buy price) – a retest of the all-time lows of £31.30/tn printed on 29th Jan-24 now looks in the offing.

The UK’s electricity generation mix is neutral in nature today with renewables contributing 34%, thermal at 35% (gas and coal) and low carbon at 19% (nuclear and imports).

Monthly Day-Ahead averages for the month so far are back on the slide after five consecutive relatively low days, and are on target to achieve £102.268/mwh (or 10.23p/kwh excluding non-energy).