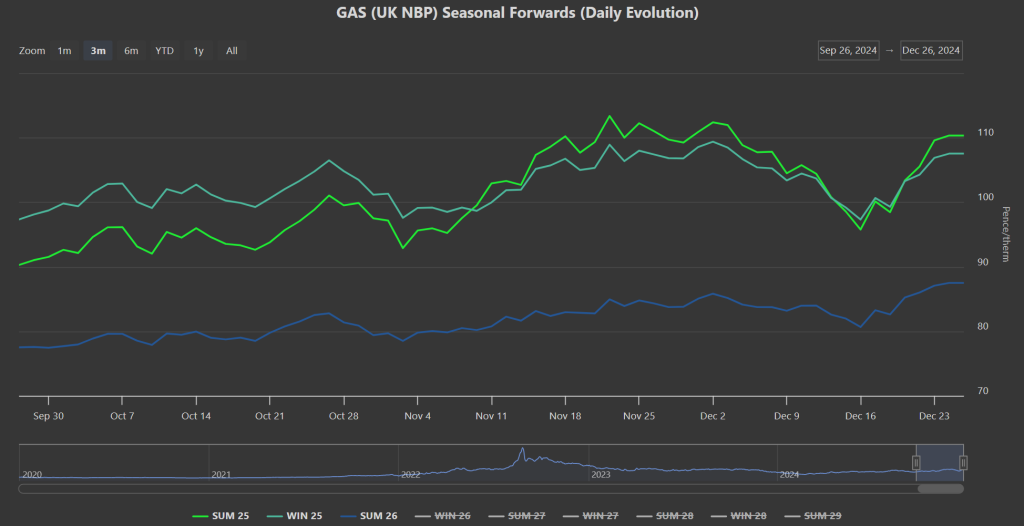

As you’d expect, volatility is high given low holiday liquidity – as such, Summer-25 delivery prices are (anomalously) back above Winter-25 delivery – see chart below.

In fact, prices are up across the board driven by ongoing worries that the Ukraine/Russia transit deal (that still supplies several European countries) is coming to an end on 31st Dec.

Vladimir Putin said on Thursday that time had run out this year to sign a new deal – nonetheless, Gazprom (Russian state gas supplier) said it would pipe marginally more gas to Europe via Ukraine today versus yesterday.

Understandably, the likes of Slovakia/Austria/Czech Republic will be none too pleased with Ukraine if they continue to obstruct a transit deal with Russia – if negotiations between Russia/Ukraine end without a deal being struck, expect “reciprocal measures” being handed out to Ukraine by its adversely impacted neighbours…

It’s inevitable that the loss of piped Russian gas will see Europe import more LNG – accordingly, Venture Global (a US LNG company) confirmed yesterday that the first cargo (from its newly commissioned Plaquemines export plant in Louisiana) had left the facility bound for Germany.

At the time of writing, European gas inventories are circa 75%% full – so slap-bang in the middle of the 8-year range.

Monthly Day-Ahead averages are almost unchanged versus 1-week ago, and are on target to achieve 110.195p/therm (or approx. 3.760p/kwh excluding non-gas).

ELECTRICITY & CARBON

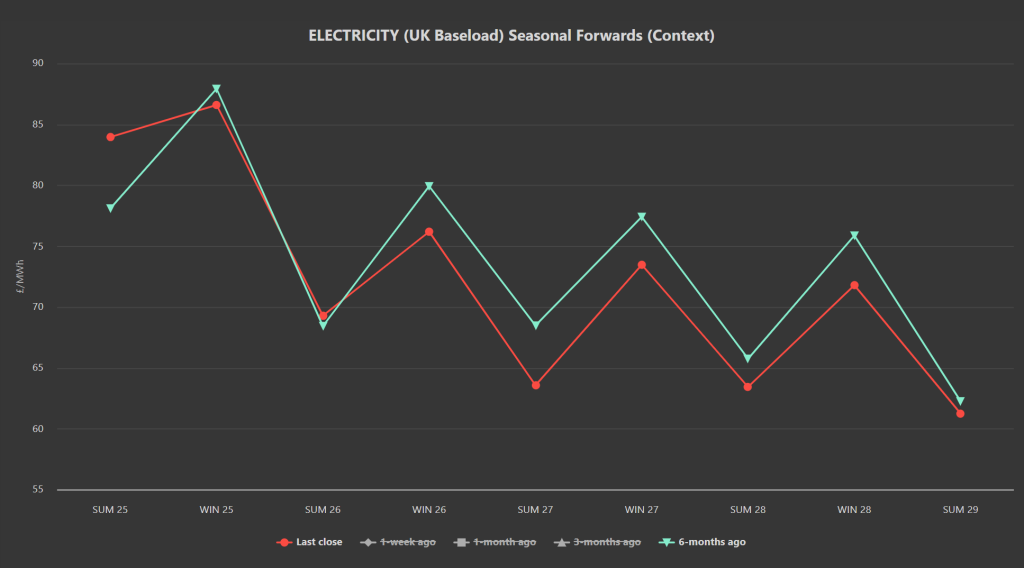

Whilst the front Season is currently higher in price than was the case 6-months ago (at the height of Summer-24), all other Seasonal Forwards down the curve are currently being offered at prices below 6-months ago (see chart below) – even though we’re in the height of Winter-24 – reflecting surely a better-than-expected winter condition.

Renewables across Europe are pretty weak in the run up to the New Year, so thermal generation demand is up (supporting gas prices).

On the Carbon markets, UKAs have found support off the back of low volume/high volatility – now at £34.92/tn on the mid-price.

Today’s UK’s electricity generation mix is bullish (and price supportive) in nature today with renewables contributing 11%, thermal at 53% (gas and coal) and low carbon at 22% (nuclear and imports).

Monthly Day-Ahead averages for the month continue to fall, holding steady below £100/mwh at £92.267/mwh (or 9.23p/kwh excluding non-energy).