Given that Summer-25 delivery prices have been consistently at a very marginal premium to Winter-25 over the last month or so, it’s fair to say that the key driver contributing to comparatively high prices at the front of the curve remains whether Europe will be able to replenish storage in time for the onset of Winter-25 conditions.

And yet, looking at European storage (across ALL of Europe, Western and Eastern), inventories are just below parity with the 8-year average.

Flip-flopping mid to long-term weather forecasts aren’t helping, as any talk of an upcoming cold spell raises fears over increased withdrawals making the summer storage target appear as an even steeper hill to climb.

However, noise aside, UK temperatures are forecast to get back above seasonal norms by 24th Jan, no doubt limiting heating/gas-for-power demand.

Encouragingly, LNG arrivals to the UK/Europe remain at the upper extremity of the 10-year range, reflecting depressed demand across Asia where, in the main, temperatures remain unseasonably warm (coupled with China’s now all too evident economic slow down).

Cargoes are following the money and heading to our shores – lending credence to the argument that we can’t afford to let our prices fall too far (now that Russia’s gas is ebbing toward Asia at reduced prices).

Geopolitically, all eyes seem to be trained on a Gaza ceasefire (though Israel continues to carry out fatal attacks) – a ceasefire would alleviate bullish pressure on the wider energy complex.

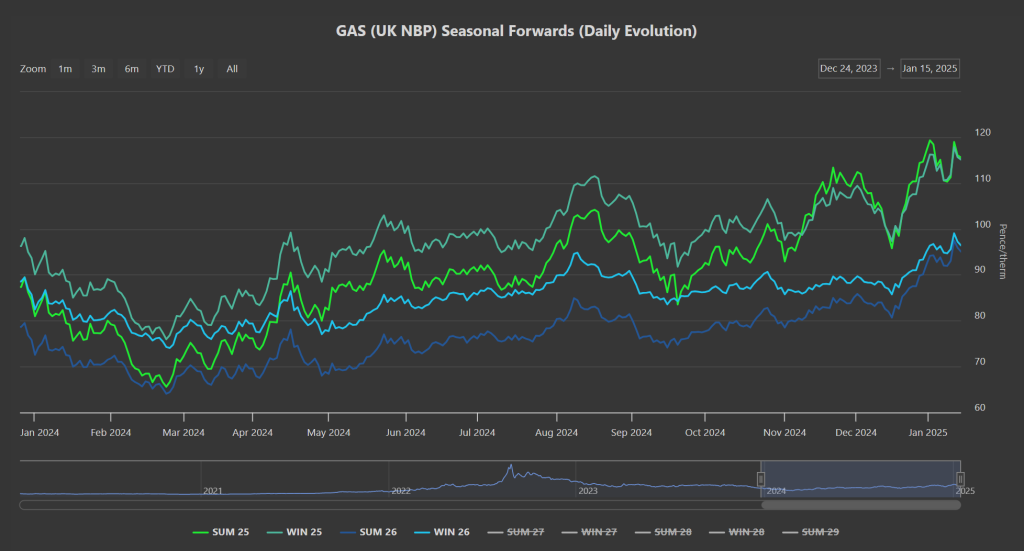

The front 6 Seasons are up versus /1-week/1-month/3-months/6-months ago – so it’s safe to say Forward prices are at the top of the market.

The front 4 Seasons are all up versus this time last year following a summer of geopolitical turmoil.

Day-Ahead prices remain more expensive than Month/Quarter-Ahead, reflecting a belief that prices are likely to fall as we approach the summer shoulder (Mar-25).

Monthly Day-Ahead averages for this month are very gradually decreasing as the month progresses – 119.226p/therm (or approx. 4.068p/kwh excluding non-gas).

ELECTRICITY & CARBON ALLOWANCES

On the Carbon markets, UKAs remain at a yawning discount versus EUAs – reflecting less scarcity of credits (with free allowances not scheduled to fall in the UK until 2027).

As we predicted, the illiquid bullish holiday period UKA rally lost steam as soon volume returned to the market.

Right now, prices are falling off a cliff, having broken below the 18th Dec lows and the lower extremity of a bearish trend channel which was confirmed at the turn of the year.

The mid-price is now at £32.06/tn (see chart below) – offering great comparative value for compliance buyers, but evidently there aren’t many of them out there (with heavy emitters having already acquired the required volumes to meet mandatory surrender).

Today’s UK’s electricity generation mix is bullish (and price supportive) in nature with renewables contributing 30%, thermal at 50% (gas and coal) and low carbon at 11% (nuclear and imports).

Monthly Day-Ahead averages for this month so far reflect poor renewables outputs – £112.986/mwh (or 11.3p/kwh excluding non-energy).