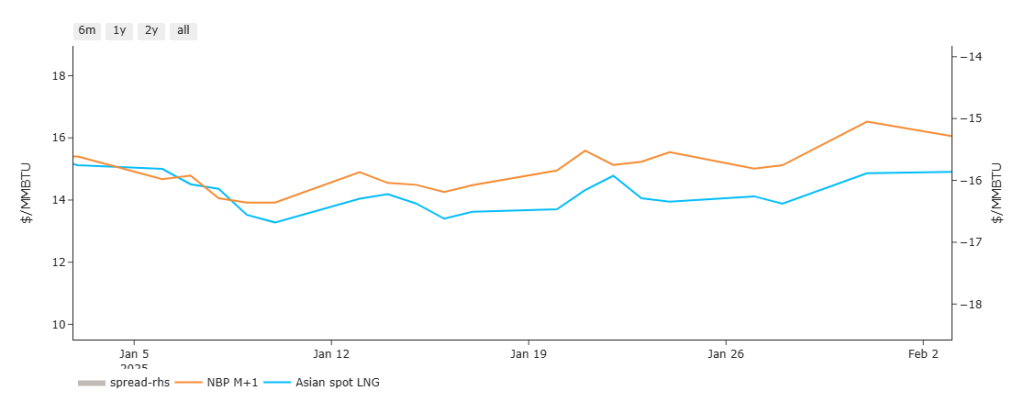

Whilst European/UK gas values remain above those of Asia/China, LNG continues to head in our direction (please see chart below detailing front-month UK gas versus Asia gas).

Markets are doing their best to absorb Trump’s tariff impacts, so remain a little bewildered by the avalanche of contradictory news.

Certainly, China has confirmed retaliatory tariff increases of 15% on US LNG (a bearish driver as more gas would then go to Europe).

However, Trump has paused some of the tariffs that were introduced over the weekend against Mexico and Canada – so will he do the same following discussions with Xi Jinping?

Given China’s rhetoric in the lead up, it would seem unlikely that they’ll be inclined to back down…

It’s worth noting that many Chinese gas buyers in the face of tariffs (that have ongoing contracts with US projects) would be forced to resell their supplies to importers elsewhere (most likely, Europe) – so if tariffs do go ahead, it could help Europe fill inventories over the coming summer.

Back in the UK, our system opened short this morning (demand forecast outstripping supply) – unscheduled Norwegian outages (Sleipner, Njord and Asgard) are reducing flows into the UK/Europe, subduing any bearish reaction to US tariffs against China and heating demand declines brought on by February’s La Niña temperatures (forecast to be above seasonal norms but coupled with low winds, unfortunately).

For now, the market remains supported on expectations that the upcoming cold spell (before things warm-up) will drive storage withdrawals, with the continued rate of decline fuelling worry over replenishing storage levels to the mandated 90% by 1st Nov ’25 (in time for the rigours of Winter-25 conditions).

However, today’s European fullness level is at 53% (exceeding the EU interim gas storage fullness target of 50%) versus the 5-year average of 54% – so are fears over storage being overcooked by the speculators (who benefit from talking up the market)?

Time will tell – suffice as to say, if US tariffs against China persist, and if US tariffs against Europe are imposed (forcing Europe to engage with Russia) – it’s entirely conceivable that the supply outlook could tilt in our favour as summer approaches.

At the time of writing, markets are trading sideways with the Mexican Peso and the Canadian Dollar having erased their losses now that Trump’s punitive tariffs have been put on hold.

The very heavily traded EUR/USD benchmark forex pairing rose back above key price levels yesterday, but remains poised for a big drop as tensions between the US and the EU look set to be the next stage in Trump’s trade war.

Even without tariffs, inflation continues to be a problem for many of the world’s leading economies – with the imposition of tariffs, might we see fiscal tightening coupled with industrial demand destruction (a bearish price driver)?

Monthly Day-Ahead averages for Jan-25 achieved 122.62p/therm (or approx. 4.184p/kwh excluding non-gas) – the average having remained at or above 120p/therm for the entire month.

It’s too early to say where Monthly Day-Ahead averages are heading this month – but right now they’re at 133.036p/therm (or approx. 4.539p/kwh excluding non-gas).

ELECTRICITY & CARBON

It’s taken a while for the heat to go out of last week’s UKA rally (fuelled by Starmer’s suggestion that EUAs and UKAs will be merged).

However, the momentum indicators are now posting bearish divergence versus price (which is now falling away from the upper extremity of the rising trend channel – please see chart below).

Indeed, EUA prices plummeted yesterday amid bearish macroeconomic sentiment caused by Trump’s new tariffs against Canada and Mexico (which were postponed later in the day).

But market participants are also pricing a fear of US tariffs against the EU, which would further dampen its economy (and result in demand destruction) – speculators are already holding very long (buy) positions, so any very bearish news will lead to a precipitous drop (given how many protective sell-orders exist below the bulls’ long positions).

Temperatures in the UK this week started below seasonal norms but have since risen and will peak marginally above seasonal norms come Wednesday.

The cold then returns as temperatures fall back below seasonal norms in time for the weekend!

The mild and windy spell we’re enjoying tight now has seen demand ease, with near-term delivery electricity prices softening as a result.

European electricity markets are also taking direction from the threat of US tariffs with US president Trump suggesting both the EU and UK could be hit with tariffs in the future.

Any tariffs will slow economic growth, resulting in demand destruction (a bearish price driver).

Today’s UK’s electricity generation mix is bearish with renewables contributing 51%, thermal at 22% (gas and coal) and low carbon at 14% (nuclear and imports).

Monthly Day-Ahead averages for Jan-25 achieved £118.060/mwh (or 11.81p/kwh excluding non-energy) – the average having stayed stubbornly above £100/mwh beginning week 2.

It’s too early to say where Monthly Day-Ahead averages are heading this month – but right now they’re at £114.978 (or approx. 11.5p/kwh excluding non-energy).