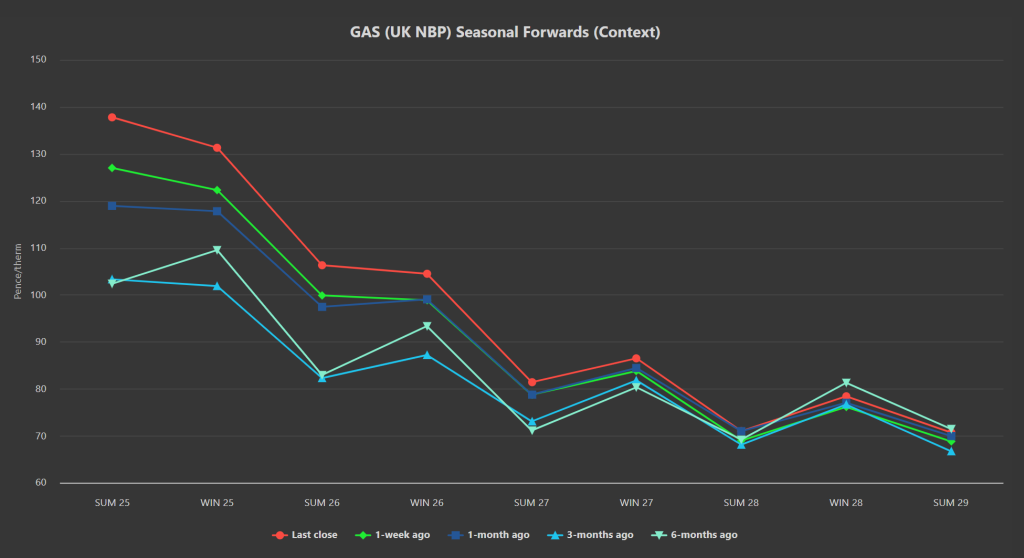

Seasonal Forward prices are up all the way out to Summer-28 (versus 1-week/1-month/3-months/6-months ago) – please see chart below.

Cold, still weather conditions are driving up demand (and putting pressure on storage withdrawals) – though notably, front-month delivery prices are flat on the day giving rise to hopes that forecasts of a warmer spell at the end of the month will reduce gas-for-power burn.

On the supply side, Norwegian flows are steady and LNG arrivals are still on the increase, matching 2023 highs.

This trend should continue over the coming weeks with plentiful cargoes arriving at Europe’s ports that would traditionally supply the Asian market (primarily Australia and Qatar).

Nonetheless (against a backdrop of wintry conditions), markets have yet to be convinced that very healthy LNG supply is enough to ensure viable supply dynamics.

For this to happen, LNG imports will likely need to rise further amid falling demand as summer approaches.

Otherwise, European inventories will remain below those we’ve enjoyed over the last couple of winters.

Were this to happen, prices would need to stay high over summer to ensure that stocks are replenished (and facilitate demand destruction).

On the geopolitical side, Trump’s comments are agitating the unsteady ceasefire between Israel and Hamas by initially suggesting America take over Gaza (and demolish/ rebuild into a resort), then threatening that should Hamas not release all Israeli prisoners by Saturday “all hell is going to break out”.

Should the ceasefire collapse, we’d no doubt return to problems in the Red Sea and LNG vessels would again be forced to avoid the Suez Canal (and head around the Cape of Good Hope adding two weeks to voyage durations).

Given the persistent anomaly of Summer-25 delivery prices remaining above those for Winter-25, Germany’s market manager has confirmed his intention to meet with traders to discuss strategy for enabling storage replenishing this summer (to achieve the mandated 90% fullness by 1st Nov ’25).

Today, European storage is at 48% versus the 5-year average of 50%, so not too far off course – though bullish market participants are already citing the impacts of scheduled Norwegian pipeline maintenance which doesn’t begin until late August!

Monthly Day-Ahead averages are on the rise as the month progresses, reflecting short-term storage withdrawals and wintry demand – 136.964p/therm (or approx. 4.673p/kwh excluding non-gas).

ELECTRICITY & CARBON

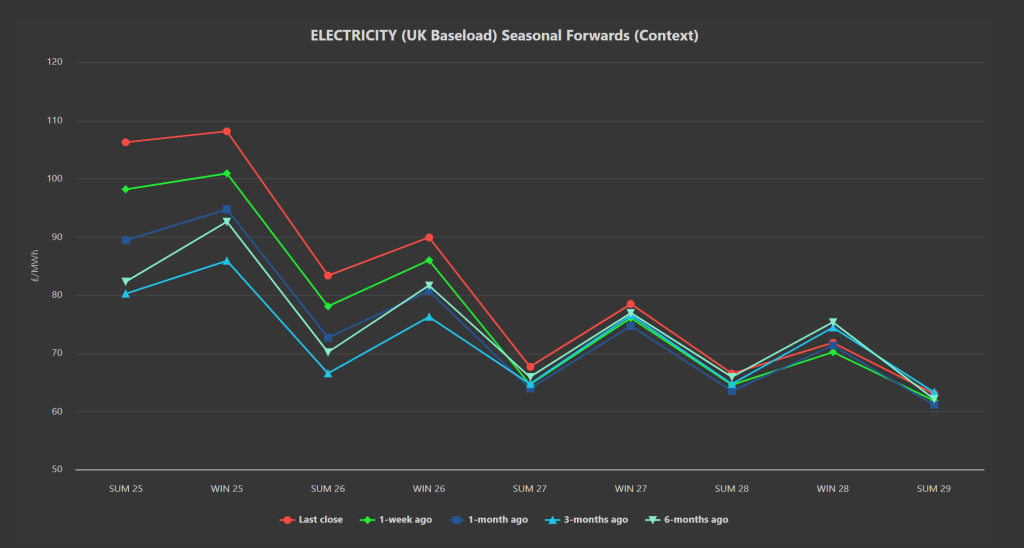

Seasonal Forward prices for UK baseload electricity are up all the way out to Summer-28 (versus 1-week/1-month/3-months/6-months ago) – please see chart below.

On the Carbon markets, whilst some of the heat has gone out of last week’s UKA rally (fuelled by Starmer’s suggestion that EUAs and UKAs will be merged), the uptrend is still technically in place.

Prices have dropped away from the upper extremity of the confirmed rising trend channel but the ascending triangle pattern (a bullish indicator) has broken to the upside and the mid-price is now at £47.93/tn.

Today’s UK’s electricity generation mix has again been bullish with renewables contributing 28%, thermal at 44% (gas and coal) and low carbon at 16% (nuclear and imports).

Monthly Day-Ahead averages so far for this month are rising, now at at £117.040 (or approx. 11.71p/kwh excluding non-energy).