Intraday, Summer-25 delivery has once more fallen below Winter-25 (to the tune of 2p/therm at the time of writing).

Prices have been threatening to drop off over the last few days, with markets feeling overbought/overcooked.

Whilst it felt this morning as though the fall was driven by profit-taking, it’s also the case that a number of bearish rumours have begun to circulate.

The European Commission’s announcement yesterday that is weighing new powers to cap gas prices will have encouraged speculators to close out long positions.

Warmer weather is also being forecast for the back-end of Feb (limiting demand and slowing the rate of storage withdrawals).

Trump has now lifted Biden’s pause on new Department of Energy permits for LNG export facilities– which clears the way for new shipment hubs to be developed.

China has of course imposed tariffs on US energy imports – meaning Europe is much more cargoes from the US.

Reports abound that Trump is determined to reach a peace agreement between Russia/Ukraine that would undoubtedly lead to a resumption of Russian pipeline flows via Ukraine into Europe.

All this, plus the long-touted glut of LNG supply expected in 2026 from projects already under way, mean that whilst the uptrend is still in place, it’s by no means a one-way bet with Summer-25 only 47 days away.

On the bullish side, Norweigian capacities are down due to unplanned outages at the Troll and Kristin gas fields (though Troll is still at 96% and the Kristin impact is negligible).

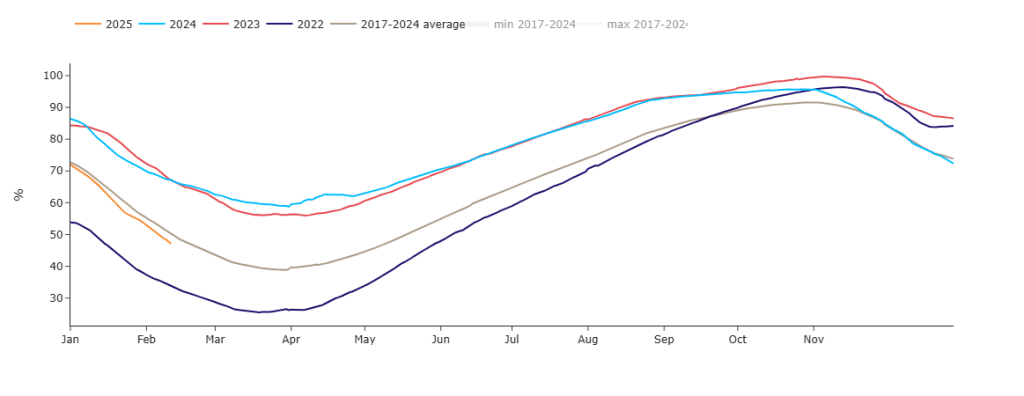

Today, European storage is at 47% hvering just below the 7-year average (please see chart below).

Monthly Day-Ahead averages will be softened by today’s price action, but are still high based on yesterday’s close – 136.071p/therm (or approx. 4.643p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, wind output forecasts have been revised downwards for the vcoming weekend (adding to the risk of increased gas-for-power burn and further storage withdrawals).

Carbon prices were down yesterday, mirroring gas and heading back towards a retest of the €80/tn support level.

The CoT (Commitment of Traders Report) confirmed speculators are net long again as of 7th Feb.

Emissions prices are of course supported by bullish weather fundamentals with cold snaps to come amid poor (wintry) renewables outputs.

Nonetheless, EUAs/UKAs remain correlated to gas which appears weakened on the news of US and Russia talks about a potential peace deal with Ukraine (and the possibility of a resumption of Russian gas flows).

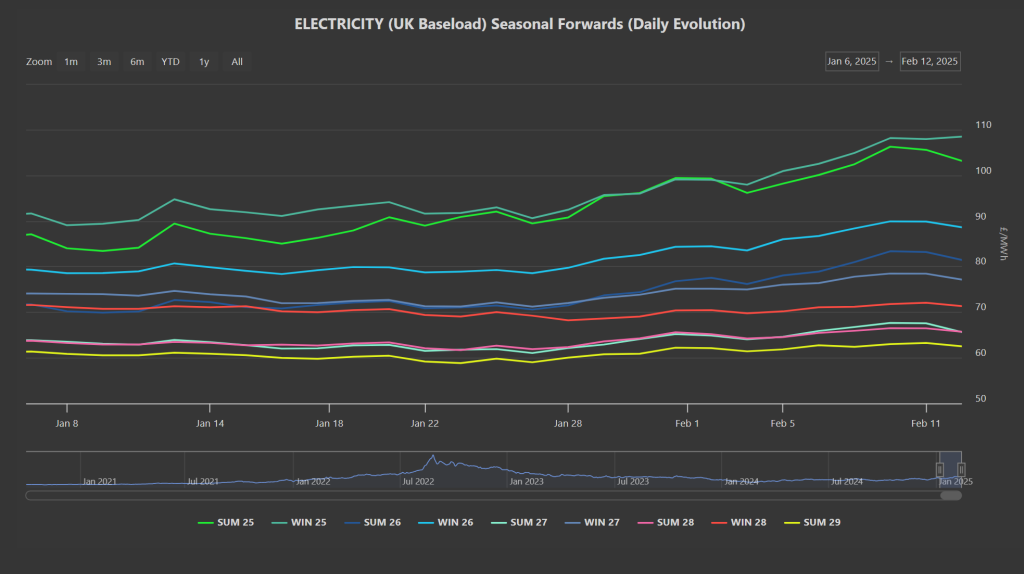

Summer-25 electricity is dropping off, whilst Winter-25 is pretty flat (please see chart below).

Today’s UK’s electricity generation mix has again been bullish with renewables contributing 17%, thermal at 53% (gas and coal) and low carbon at 21% (nuclear and imports).

Monthly Day-Ahead averages so far for this month are at at £119.224 (or approx. 11.92p/kwh excluding non-energy).