Whilst the overall trend in UK gas markets remains bearish, the drivers behind the fall need to be watched closely over the coming days/weeks.

Trump’s determination to re-order trade balances by imposing reciprocal tariffs drove markets steeply lower off the back of fears of global economic slowdown – with equities selling-off and money jumping into safe-havens (primarily gold and bonds).

Then rumours circulated that China was strategically dumping their inventory of US bonds, thus driving the prices lower and forcing the yields back up (making it more expensive for the US to borrow money).

By way of response to China’s perceived intransigence, Trump has offered a stay of execution to those countries that have approached the US over the last few days to reach a deal, rolling back their reciprocal tariffs to 10% for 90-days – except China, for whom Trump has raised the tariff to 125%!

So, for the time being at least, trade between the world’s two largest economies has ground to a halt – as such, US LNG that has historically found its way to China (when the JKM spread has meant cargoes to Asia will make more money), will now need to go elsewhere.

Of course, Europe (and the UK) will be the most obvious beneficiaries – so energy markets remain soft at the prospect of more gas being made available over the coming summer months (so as to allow a less panicky replenishment of European storage in time for the mandated 90% by 1st Nov).

It’s already been confirmed, in fact, that China’s hitherto importers of US LNG haven’t wasted any time in transferring the lion’s share of their contracted volumes to Europe to secure better returns against a backdrop of weak demand, shaky economic indicators and retaliatory tariffs on US imports of 84%.

So as not to miss this golden opportunity to ensure a sustained fall in gas prices (when most needed), European countries are edging ever closer to a revision of the mandated storage requirement by 1st Nov – with a 10% reduction looking most likely and a softening of the 1st Nov deadline (perhaps a wider time window).

Such measures will mitigate fear and avarice amongst market participants amid more plentiful supply and subdued Asian competition (hopefully).

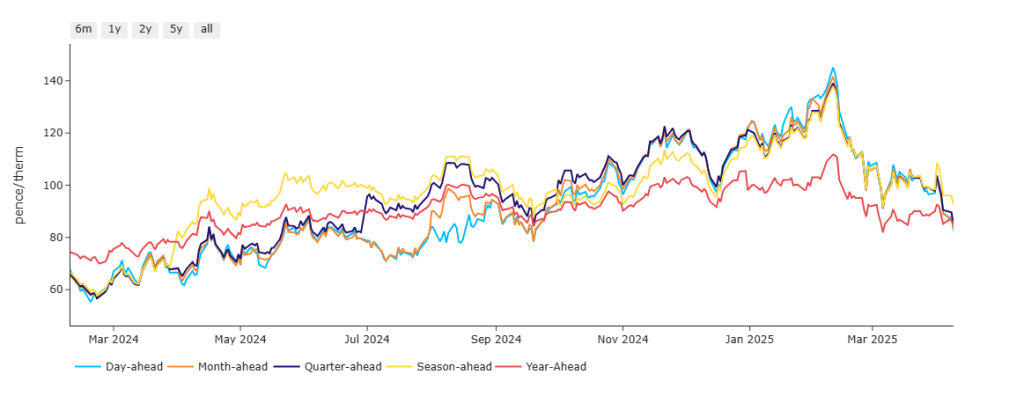

It’s worth noting that this time last year Year-Ahead prices were higher than Day/Month/Quarter-Ahead – this year (beginning Oct’24) the opposite is true.

So, mid-term risk has been lower than near-term risk since the onset of Winter-24, reflecting surely an underlying belief amongst market participants that all the pain has been at the front-end.

Now, Day/Month/Quarter/Season-Ahead are very close to parity with prices falling, reflecting surely an underlying belief amongst market participants that the commodity is losing value for both near- and mid-term delivery (please see chart below).

So, are we seeing the beginning of the impacts of a new world order?

Depending on what you believe, Trump’s tariffs are aimed at encouraging global businesses to relocate their manufacturing base to the US to avoid paying the import taxes (which are inevitably passed along to consumers).

But how long will this take? And will the global economy be able to withstand the rigours of the transition? Surely economic contraction will inevitably lead to global recessions and Trump will be forced to change tack? Or will China come to the table and start negotiating?

For now, these unanswerable questions will likely keep a firm lid on global equities and continue to wreak havoc across macroeconomic indicators.

As of this morning, UK gas prices are holding steady at sub-100p/therm all the way from the front to the back – so, with Summer-25 now begun in earnest, conditions point to good potential for further downside in price if we can start seeing some meaningful injections into storage over the coming weeks (and if we can have a lighter maintenance season across Norway this summer than has been the case over the last few years).

Right now, European storage is at 35% versus the 5-year average of 49% (but levels are slowly rising – so injections are very marginally higher then withdrawals as you’d expect for this time of year).

The spread between Summer-25/Winter-25 prices is slowly widening, making it more viable for traders across EU nations to stockpile in advance of Winter-25.

FLEX clients with open volumes down the curve are encouraged to assess the solid comparative values currently available down the curve, and to start drawing lines in the sand for respective periods of delivery (i.e., how do prevailing Forward prices compare to current hedged prices, and what are your price targets for near/mid/far-term?)

This month’s gas Day-Ahead averages are at 91p/therm (or approx. 3.1p/kwh excluding non-gas).

ELECTRICITY & CARBON

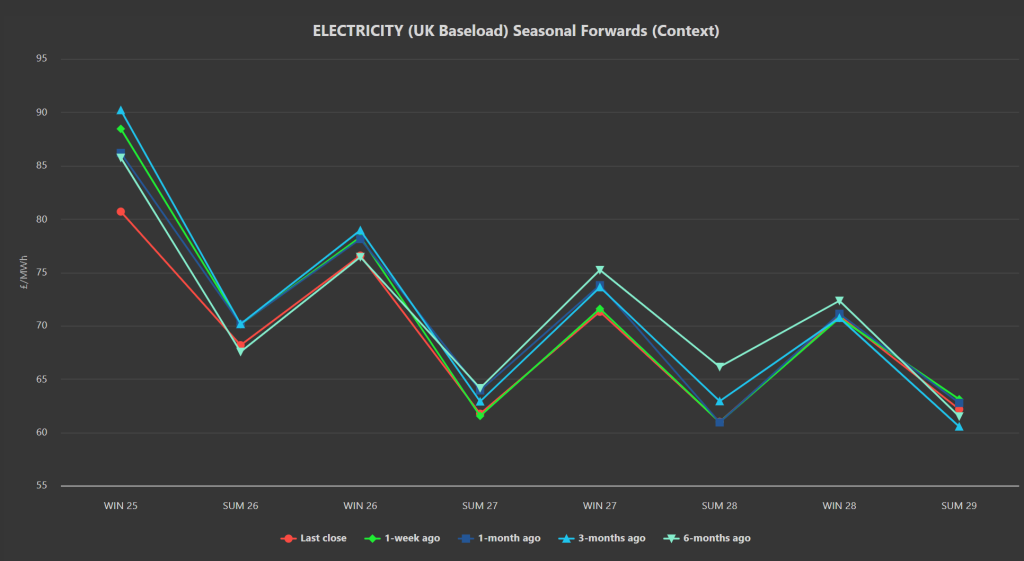

Electricity values look increasingly solid, with ALL Seasonal Forwards below £85/mwh (or 8.5p/kwh) at the time of writing.

On the Carbon markets, UKAs have reacted bullishly to Trump’s climb-down on reciprocal tariffs (with investment speculators still net long and emissions increasingly developing a correlation with equities).

However, if gas prices see a sustained bear run over the coming months, how long can Carbon resist a fall?

Today’s UK electricity generation mix is price supportive, with renewables contributing 19%, thermal at 39% (gas and coal) and low carbon at 24% (nuclear and imports).

So far this month, electricity Day-Ahead averages are on target to achieve £77/mwh (or approx. 7.7p/kwh excluding non-energy).