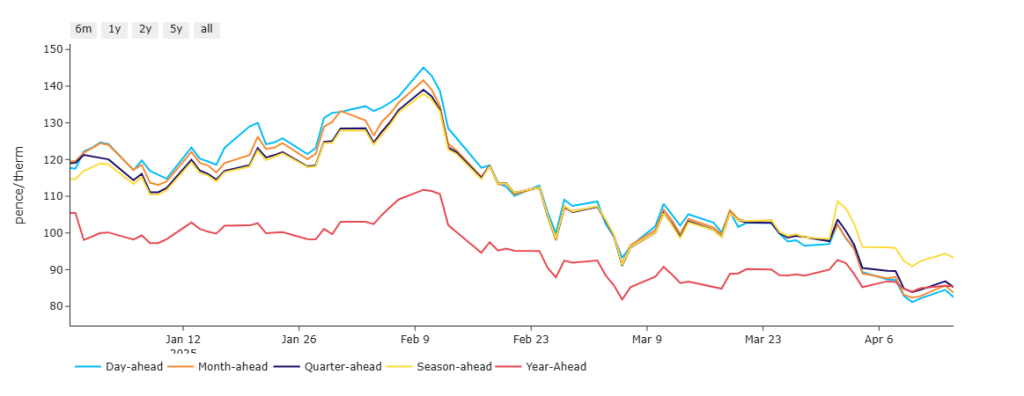

Back on 10th Feb (at the height of Winter-24 delivery), Day/Month/Quarter/Season-Ahead were at a 23% premium to Year-Ahead – reflecting front-loaded risk (please see chart below).

Fast forward to today, and Day/Month/Quarter/Year-Ahead are at an 11% discount to Season-Ahead – reflecting near/mid/far term prices having converged at near parity (so volatility has undeniably settled down).

The Easter weekend is nearly upon us, and so liquidity is already dropping off in preparation for trading desks being closed Friday to Monday inc.

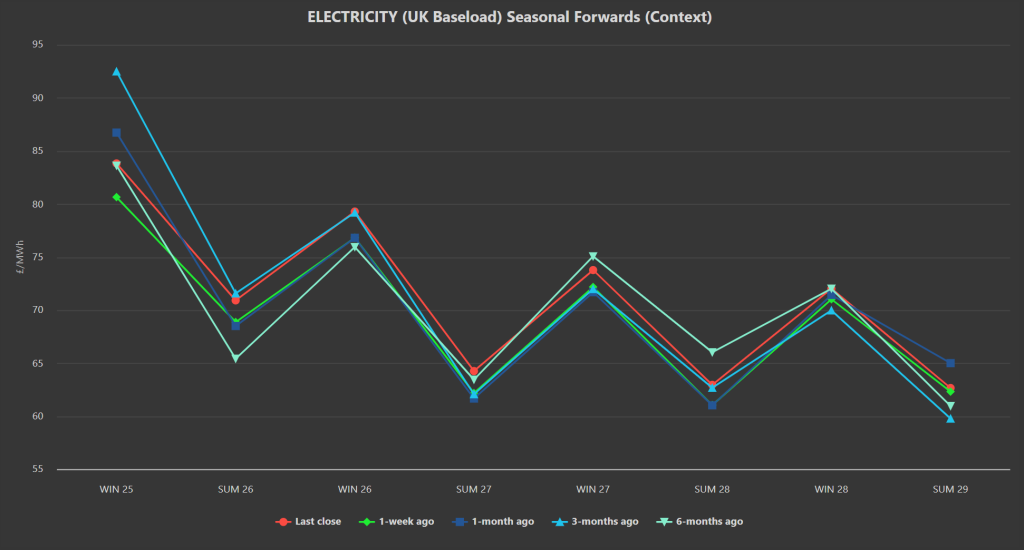

Seasonal Forwards are down versus 1-month/3-months/6-months ago, but on a par with one week ago – so it’s fair to say that prices are well balanced/at equilibrium.

The UK system opened short this morning (demand forecast outstripping supply) with some minor outages bringing modest pipeline capacities offline – but nothing serious.

European storages are enjoying some ‘summery’ injections, with fullness now at 44% versus the 5-year average at 49% – accordingly, Winter-24’s alarmists (opportunistic sales people/bullish traders) have stopped making quite so much noise about Europe’s inability to replenish storage in time for Winter-25…

The US and Russia continue to enjoy bilateral discussions, with Witkoff (US Special Envoy to the Middle East) now headed for France following ‘compelling’ meeting with Putin over ‘five territories’ in Ukraine.

It would seem obvious that deals are being struck – market participants are all ears should a ‘peace deal’ be imminent (amid rumours that the US wants to take control of the Sudzha pipeline as part of the long touted minerals deal between the US and Ukraine).

On the weather side of things, long-range forecasts are starting to edge towards a hot summer – so market bulls are keen to suggest that Asia will be forced to compete with Europe for LNG cargoes (so as to acquire gas imports to power air-con units etc).

Though if the US and Asia remain entrenched in tariff wars for the foreseeable future, it seems a bit far-fetched to suggest Asia will want to buy LNG at any price – China, for one, will likely revert to coal instead.

Buyers should be mindful that the bottom of this market may only come about if/when it becomes clear that we’ll successfully replenish gas stocks in time for Winter-25, and/or Putin and Trump engineer a means of getting more Russian gas flows into the European system – neither of which may happen any time soon.

As such, taking a nibble out of current prices (or ‘scaling-in’) would seem increasingly prudent – hedging increments of Forward volumes regularly (and gradually) as summer progresses.

This month’s UK gas Day-Ahead averages so far continue to fall – now at 87p/therm (or approx. 2.9p/kwh excluding non-gas).

ELECTRICITY & CARBON

Seasonal Forwards all the way down the curve continue to be offered at sub-£85/mwh (please see chart below – the red line being yesterday’s closing prices).

On the Carbon markets, UKAs reacted bullishly to Trump’s climb-down on reciprocal tariffs (with investment speculators still net long and emissions increasingly developing a correlation with equities).

However, if gas prices see a sustained bear run over the coming months, how long will it be before Carbon follows suit?

Right now, Dec-24 UKAs are back up at £47.39/tn having broken above the upper extremity of a long term bearish trend channel – though confirmed resistance can still be found around £48.80/tn.

Today’s UK electricity generation mix is very bearish in nature, with renewables contributing 66%, thermal at 8% (gas and coal) and low carbon at 21% (nuclear and imports).

So far this month, electricity Day-Ahead averages are on target to achieve £78/mwh (or approx. 7.8p/kwh excluding non-energy).