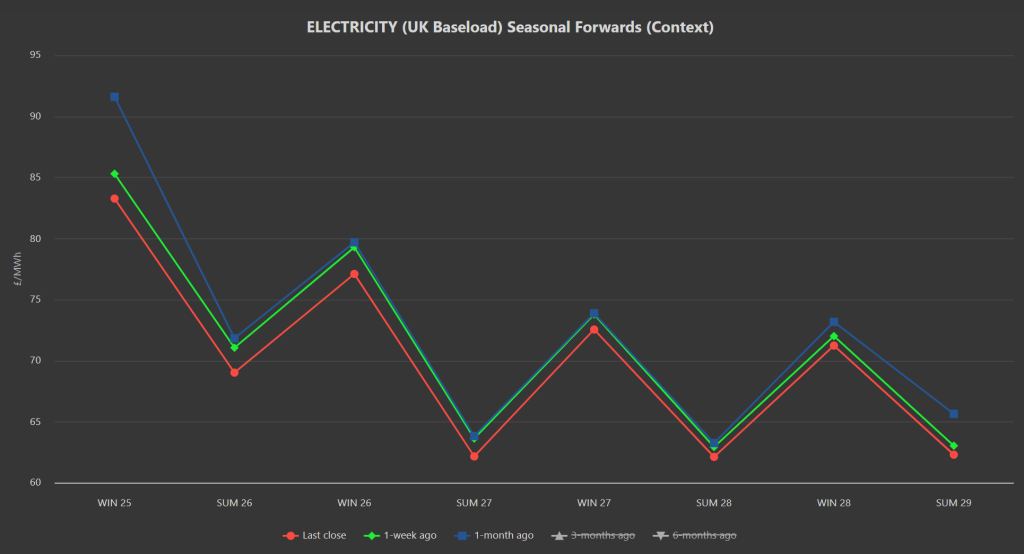

Delivery prices for the front 3-Seasons (Winter-25; Summer-26; Winter-26) are down versus 1-week/1-month/3-months/6-months ago.

In addition, Day/Month/Quarter/Year-Ahead are at a significant discount to Season-Ahead – so no matter how you look at it, noise aside, comfortable fundamentals abound, and comparative summer value is increasingly on offer.

Prices dropped off yesterday again against a backdrop of improving weather forecasts and falling demand.

Some Norwegian pipeline flows have been redirected from Europe to the UK – nonetheless, our system opened short this morning (demand forecast outstripping supply) – so Day-Ahead might see a little upward pressure today but not enough to have any meaningful impact on prices further down the curve.

European gas prices remain at a premium to the UK’s, reflecting marginally less risk in our supply/demand dynamics.

Storage levels across Europe are at 37% versus the 5-year average of 50%, so whilst the trajectory of stock replenishment is shallow, at least it’s climbing (and injections are steady).

Market participants remain pretty much entirely focussed on whether Europe will be able to adequately re-fill storage inventories in time for the withdrawals season (Winter-25).

Europe is seemingly preparing to shoot itself in the foot, with a sanction on spot purchases of Russian LNG still looking likely – limiting much needed supply over the coming months.

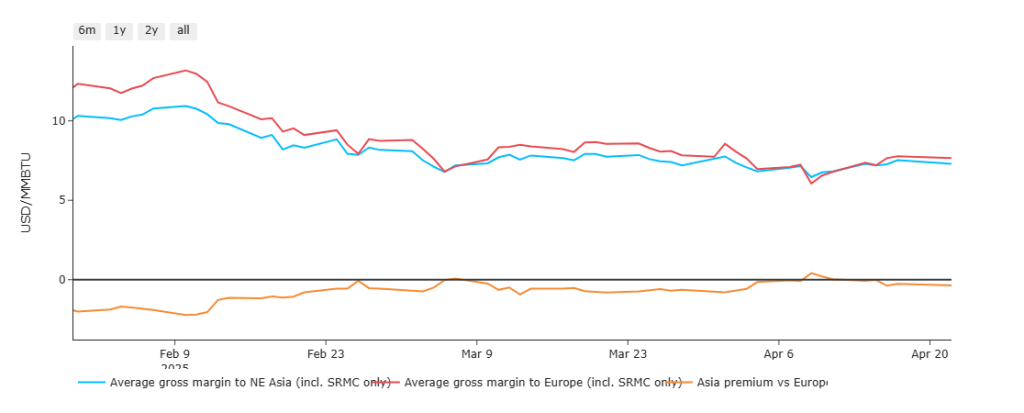

Asia JKM prices are down again, and LNG netbacks remain in Europe’s favour (i.e., LNG cargoes are making more profits heading to Europe than Asia) – please see chart below.

Buyers should be mindful that the bottom of this market may only come about if/when it becomes clear that we’ll successfully replenish gas stocks in time for Winter-25, and/or Putin and Trump engineer a means of getting more Russian gas flows into the European system – neither of which may happen any time soon.

As such, taking a nibble out of current prices (or ‘scaling-in’) would seem increasingly prudent – hedging increments of Forward volumes regularly (and gradually) as summer progresses.

This month’s UK gas Day-Ahead averages are holding very steady at 87p/therm (or approx. 2.9p/kwh excluding non-gas).

ELECTRICITY & CARBON

Seasonal Forwards all the way down the curve are down versus 1-week/1-month/3-months ago (please see chart below).

On the Carbon markets, UKAs reacted bullishly to Trump’s climb-down on reciprocal tariffs (with investment speculators still net long and emissions increasingly developing a correlation with equities).

Right now, Dec-24 UKAs are back up at £47.90/tn having broken above the upper extremity of a long term bearish trend channel – though confirmed resistance can still be found around £48.80/tn.

Today’s UK electricity generation mix is a little bullish in nature, with renewables contributing 24%, thermal at 41% (gas and coal) and low carbon at 22% (nuclear and imports).

So far this month, electricity Day-Ahead averages are on target to achieve £79/mwh (or approx. 7.9p/kwh excluding non-energy).