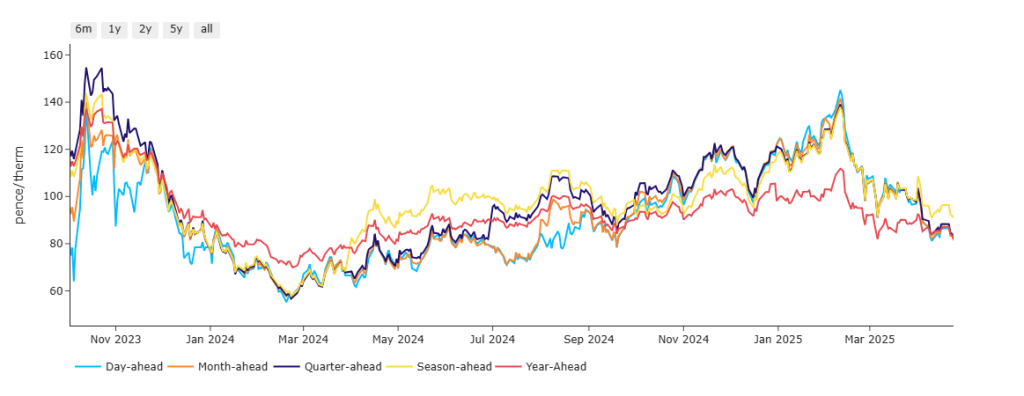

Whilst the lows last seen in Feb ’24 are still well-below current prices, it’s fair to say we’re headed in the right direction (please see chart below).

Prices have been falling steadily now (and in a confirmed downtrend) for just over two months, and bearish momentum has picked up again this week as we approach the conclusion of the first month of Summer-25.

In Europe and the UK, wider fundamentals are increasingly benign and ‘summery’ with heating demand close to historical lows.

As has been widely anticipated, the EP (European Parliament) has now voted to back plans to loosen the storage targets from 90% to 83%, and has removed the 1st Nov deadline to instead look to achieve the lowered storage figure between 1st Oct to 1st Dec (with a 4% downside allowance in the even market conditions are not favourable to injections) – this climb down will alleviate bullish pressure in the months leading up to the withdrawals season.

Notably, Germany’s Wilhemshaven on the North Sea will receive its second shipment of LNG this coming Monday – Wilhelmshaven LNG terminal is Germany’s first LNG shipping terminal.

Along with Brunsbüttel and Stade, these new terminals were a response to the lost pipeline flows from Russia (a fourth terminal is also planned for Lubmin).

At 38% versus the 5-year average of 50%, European storage fullness is building slowly but surely, and LNG arrivals are well above normal levels – owing, in part, to subdued Asian demand, in part to Trump’s tariff war with China, and in part due to the fact that degasifying at European destinations is more profitable than doing so across Asia.

With Asian gas at a discount to European gas, but with European gas still falling, there’s more room for further downside so long as we maintain a premium over Asian prices.

On the geopolitical front (and in moves to further liberate the world from the need to engage with Russia), President Ursula von der Leyen continues to reassert the EU’s intention to phase out all imports of Russian fossil fuels, and President Trump’s energy security council plans to host a summit in Alaska in early June, with a view to encouraging Japan and South Korea to firm-up commitments to the Alaska LNG project.

Buyers should be mindful that the bottom of this market may only come about if/when it becomes clear that we’ll successfully replenish gas stocks in time for Winter-25 (looking increasingly likely), and/or Putin and Trump engineer a means of getting more Russian gas flows into the European system (still on the cards).

Nonetheless, prices are looking increasingly favourable all the way down the curve – from front to back.

As such, taking a nibble out of current prices (or ‘scaling-in’ modest tranches of volume) is growing in popularity day-on-day.

This month’s UK gas Day-Ahead averages are drifting lower, now at 86p/therm (or approx. 2.9p/kwh excluding non-gas).

ELECTRICITY & CARBON

Not surprisingly, electricity markets entirely correlated to gas movements.

This correlation is even more pronounced given the weak renewables outputs of late (so increasing gas-for-power burn).

Notably, the UK’s commitment to renewable generation (under Labour’s GB Energy) is hotting up, with plans for £300-mn investment into more offshore wind farms.

Winter-25 is knocking on the door of £80/mwh (to the downside) – if this level breaks, all Seasons down the curve will be sub-£80/mwh.

On the Carbon markets, UKAs reacted bullishly to Trump’s climb-down on reciprocal tariffs (with investment speculators still net long and emissions increasingly developing a correlation with equities).

Right now, Dec-24 UKAs are back up at £47.67/tn having broken above the upper extremity of a long term bearish trend channel – with confirmed (and holding) resistance at £48.80/tn (please see chart below).

However, as has been the case since the current rangebound trading began (back in early Feb’25), momentum indicators are divergent and reflective of trends with little conviction either way.

Today’s UK electricity generation mix is bearish in nature, with renewables contributing 37%, thermal at 24% (gas and coal) and low carbon at 23% (nuclear and imports).

So far this month, electricity Day-Ahead averages are holding steady at £79/mwh (or approx. 7.9p/kwh excluding non-energy).