Markets have traded sideways this week – but importantly for buyers, last week’s price drops have held steady (hence the consolidation – as market participants carve out a new price range).

Whilst chatter has been quiet today given the bank holiday weekend, prices have inched up a little in reaction to impending Norwegian outages (both scheduled and unscheduled) – limiting flows, and slowing the rate of injections into storage.

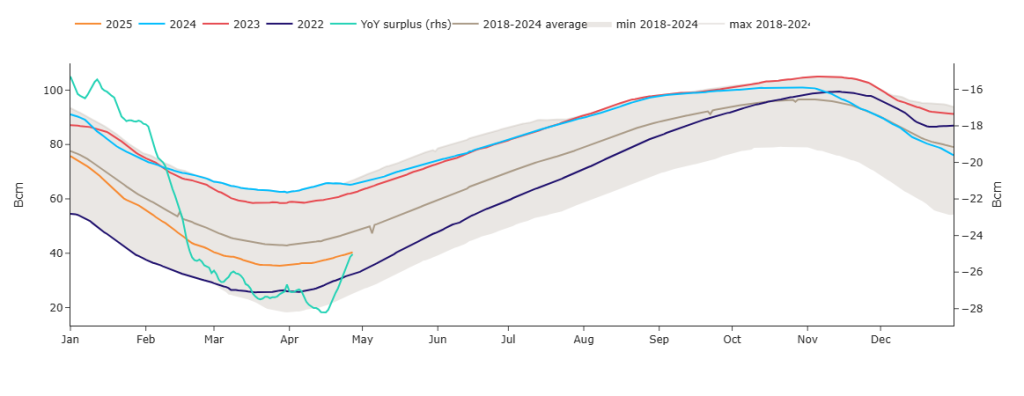

As per the chart below, storage is headed in the right direction – now at 40% versus the 5-year average of 51%.

Traders cite concerns that Russia will be feeling aggrieved now that the US and Ukraine have signed the minerals deal (making it more difficult surely for Russia to attack Ukraine once a US ‘presence’ on the ground is established…)

Bears cling onto hopes that the US can still engineer a return of Russian flows into the global system.

Europe has gone public on a £50bn trade deal with the US (including more US LNG imports) designed to placate Trump with a view to avoiding his impending reciprocal tariff attack.

On the trading side, clients running FLEX supply are encouraged to scale-in modest hedges over the coming days/weeks whilst the going’s good.

Whilst markets may still have further to fall, it’s worth remembering that current pices for Winter-25 (for example) are at a 66% discount versus the highs of Aug ’22 – so prevailing comparative value is undeniable!

This month’s UK gas Day-Ahead averages are drifting incrementally lower, now at 78p/therm (or approx. 2.6p/kwh excluding non-gas).

Electricity markets continue to move in tandem with gas.

Winter-25 managed to break below £80/mwh at yesterday’s close – but today’s uptick means £80/mwh is still holding as a key support level.

On the Carbon markets, prices have broken above horizontal resistance and look set to break above £50/tn for the first time in 2025 (please see chart below).

Emissions are increasingly developing a correlation with equities as opposed to fossil fuels – so this latest move is being driven by speculation, not fundamentals.

Right now, Dec-24 UKAs are back up at £49.77/tn with upper bullish trend channel resistance at £50.74/tn.

RSI momentum has also broken to the upside so unless gas sees some significant falls over the coming weeks, we’d wager UKAs have entered a new bullish pattern.

Today’s UK electricity generation mix is very bearish in nature, with renewables contributing 51%, thermal at 11% (gas and coal) and low carbon at 22% (nuclear and imports).

So far this month, electricity Day-Ahead averages are falling, now at £69/mwh (or approx. 6.9p/kwh excluding non-energy).