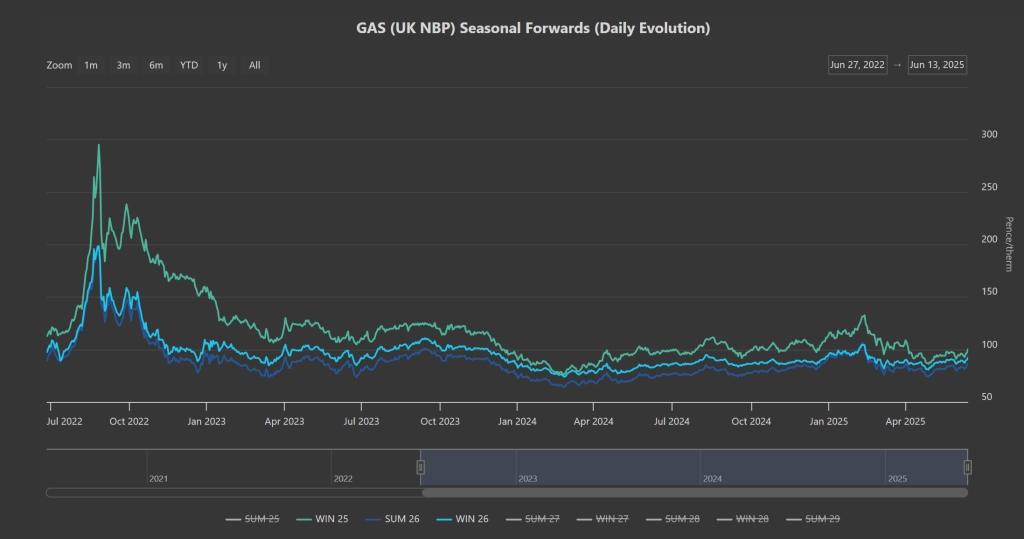

Escalating conflict between Israel and Iran is supporting prices from front to back, all the way down the curve – most notably, Winter-25 is back above the psychological resistance level of 100p/therm.

To put the recent moves into perspective amid the noise, please see chart below detailing the evolution of prices for the front-seasons (Winter-25/Summer-26/Winter-26) dating back to the energy crisis of Aug ’22.

As you can see, whilst prices have certainly reacted with increased risk-premium the last few days, it’s too early for panic stations.

The tensions between Israel-Iran have now entered their 4th day – market participants are pricing-in the risk of supply disruption via the Straits of Hormuz, as well as counting the cost of a fire at the South Pars facility after Israeli strikes hit the area taking 12 mcm/d gas production offline (the South Pars/North Dome field is a gas field in the Persian Gulf).

Whilst the UK system opened long this morning (supply outstripping demand forecast), ongoing Norwegian summer maintenance and temperatures significantly above seasonal norms across Europe are both supportive drivers (limiting pipeline flows and increasing cooling demand).

European storage is at 53% versus the 5-year average of 61% – so, for now at least, warm and windy conditions are helping with injections.

On the trading side, clients running flexible capability are watching from the sidelines as the Israel-Iran flare-up unfolds – in the near term, talk of Iran regime change is pervading the airwaves (so expect more volatility in the coming days).

This month’s UK gas Day-Ahead averages are at 86p/therm (or approx. 2.9p/kwh excluding non-gas).

ELECTRICITY & CARBON

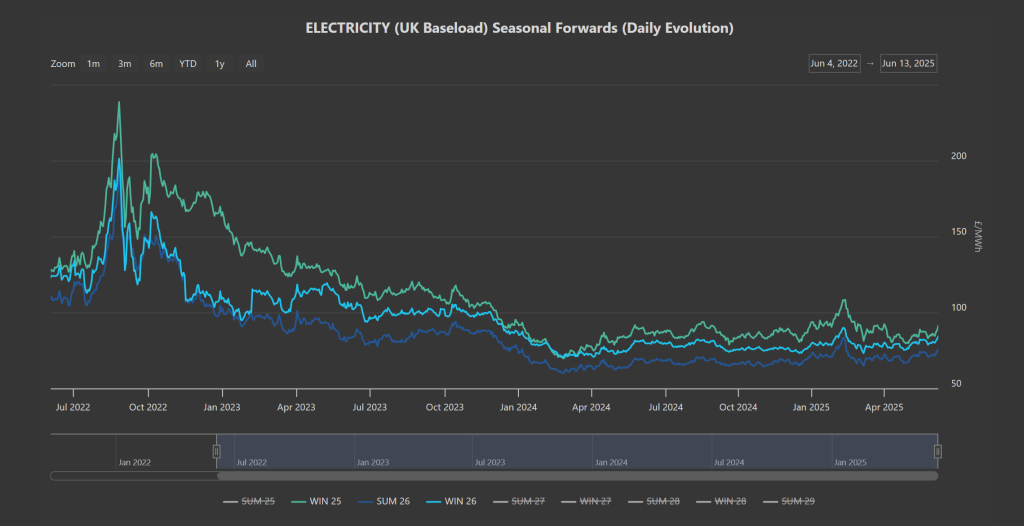

Not surprisingly, near-term electricity prices (especially at the front-end) are well-supported to start the week.

Notably, Winter-25 is adding to last week’s gains – now at £94/mwh (so an increase of 18% versus the lows we saw back on 1st May).

Again, to put the recent moves into perspective amid the noise, please see chart below detailing the evolution of prices for the front-seasons (Winter-25/Summer-26/Winter-26) dating back to the energy crisis of Aug ’22.

On the Carbon side of things, UKAs continue to drift toward parity with EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May – UKAs remain well-bid sitting at £54.24 on the mid-price this morning.

Today’s UK electricity generation mix is bearish in nature reflecting benign weather conditions – specifically, renewables are contributing 38%, thermal at 16% (gas and coal) and low carbon at 24% (nuclear and imports).

Electricity Day-Ahead averages for the month are creeping up in response to geopolitical risk – currently at £66/mwh (or approx. 6.6p/kwh excluding non-energy).

On the trading side, clients running flexible capability are watching from the sidelines as the Israel-Iran flare-up unfolds – in the near term, talk of Iran regime change is pervading the airwaves (so expect more volatility in the coming days).