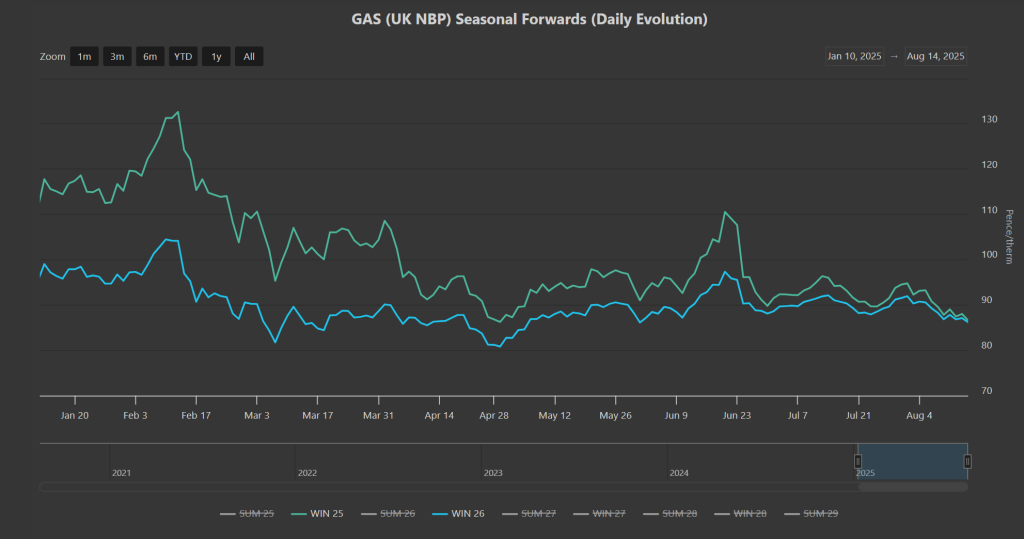

Notably, Winter-25 prices have drifted lower to near-parity with Winter-26 prices amid benign ‘summery’ conditions, and comfortable supply/demand dynamics – please see chart below.

European inventories are now at 73% versus the 7-year average of 77% – so last winter’s panic over missing minimum storage requirements in time for the heating season is but a fading memory.

Asian demand for LNG remains subdued, and vessels continue to enjoy higher profits delivering to European shores (which remains the primary supportive driver in this market – as our prices need to stay high enough so as to continue to attract arrivals to our shores).

If prices fall too far, our ability to replenish storage would be hampered, and prices would then spike accordingly to reflect potential scarcity/supply tightness.

For buyers, this summer has been about hedging on the right side of the trading range – but with 46 days remaining of Summer-25, the trading window grows ever tighter.

Late buyers for Winter-25 deliveries need to be mindful that for most of September, Norway’s annual scheduled maintenance climax will seeing significantly reduced pipeline flows to Europe (limiting storage injections).

Trump and Putin are due to meet in Alaska today after markets close, so the outcomes (if there are any) will not be felt until Monday’s open.

Russia remains understandably keen to resume gas exports (as do European bears!), but following this week’s optics of Europe and Kyiv expressing deep anxiety that a deal could be done without them, it looks unlikely that much will happen today (that is openly reported at least).

Monthly Day-Ahead averages for the month so far are at 79p/therm or 2.65p/kwh (all but unchanged from the start of the month, reflecting very low-short term risk).

ELECTRICITY & CARBON

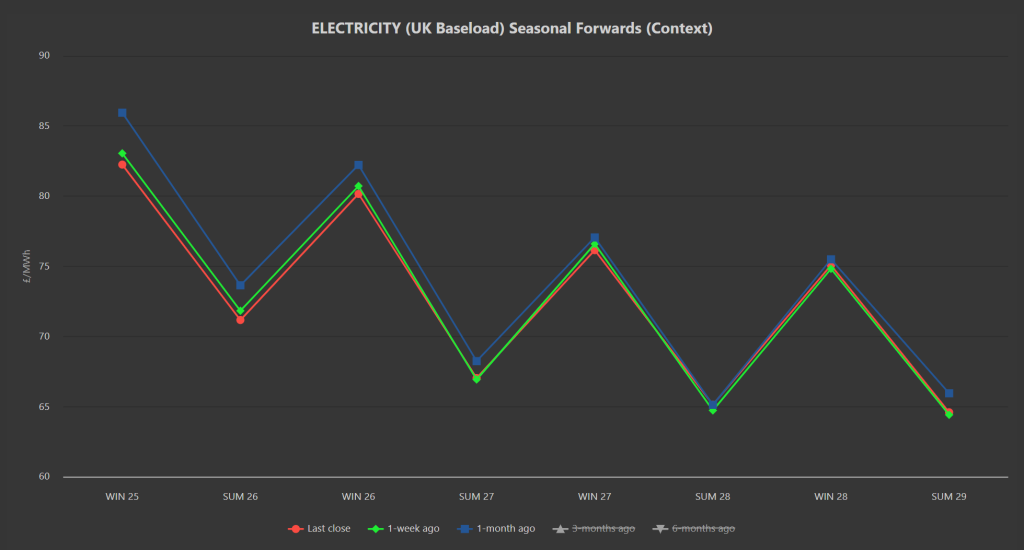

Seasonal Forwards are down on the week/month (especially front-end) – please see chart below.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are at £50.78/tn on the mid-price, and look to have broken below key support levels.

Today’s UK electricity generation mix is bearish in nature due to improved wind outputs – specifically, renewables are contributing 43%, thermal at 13% (gas and coal) and low carbon at 24% (nuclear and imports).

Monthly Day-Ahead averages for the month so far are at £67/mwh or 6.7p/kwh exc non-energy (so, on target to be the lowest month so far this summer, reflecting overhelmingly bearish fundamentals and very low short-term risk).