A ceasefire agreement between Putin/Zelensky looks increasingly unlikely – as such, focus is starting to shift toward the coming heating season and European storage.

European inventories are now at 76% versus the 5-year average of 81% – so we’re on track to reach dry land before injections stop and withdrawals begin (usually November).

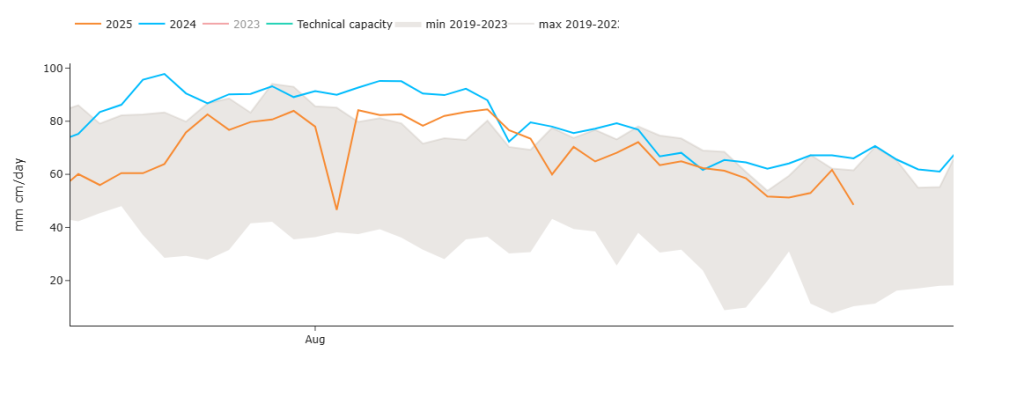

Norwegian outages are ramping up, with import in to the UK beginning to fall accordingly (please see chart below detailing declining Norwegian imports into the UK) – several facilities are now under maintenance, including the giant Troll field (though supply interruptions aren’t as bad as initially anticipated – yet).

Any late buyers of Winter-25 delivery are still advised to get in BEFORE the 2nd week of September at the very latest.

Warmer weather is forecast to spread across Europe over the coming fortnight – which should help to keep a lid on gas-for-power burn.

Monthly Day-Ahead averages for the month so far are at 79p/therm (or 2.7p/kwh exc. non-gas) – all but unchanged throughout the month, reflecting very low-short term risk.

ELECTRICITY & CARBON

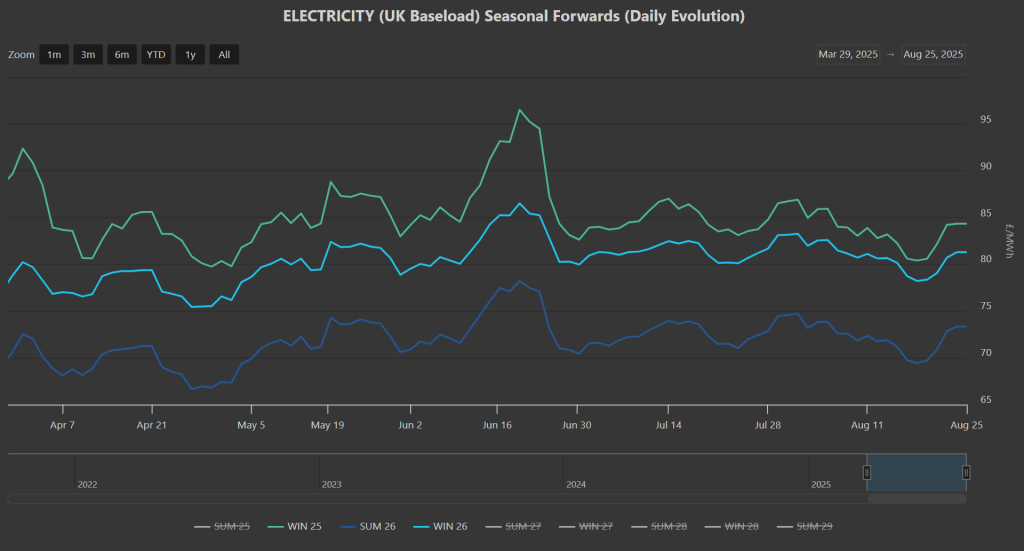

The front 3-Seasons (Winter-25/Summer-26/Winter-26) remain toward the bottom of the rangebound price action we’ve seen this summer (please see chart below).

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are at £51.65/tn on the mid-price, having fallen below support to start the week but now retesting resistance – in short, it’s rangebound price action with prices having traded within a 15% bracket since the onset of Summer-25 (1st Apr).

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 54%, thermal at 10% (gas and coal) and low carbon at 20% (nuclear and imports).

Any late buyers of Winter-25 delivery are still advised to get in BEFORE the 2nd week of September at the very latest.

Monthly Day-Ahead averages for the month so far are at £73/mwh (or 7.3p/kwh exc. non-energy).