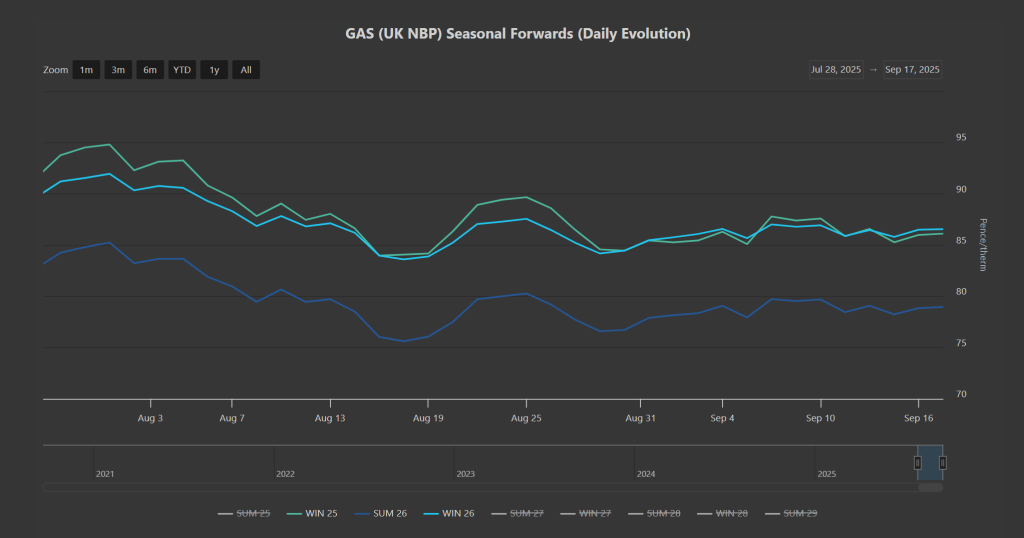

Notably, Winter-26 delivery prices have drifted above those for Winter-25 – reflecting low short-term risk versus higher Year-Ahead risk (please see chart below).

All clients are now heavily hedged for Winter-25 (the onset of which is only 12 days away).

Concerns over European storage levels persist, with fullness now at 81% versus the 5-year average of 93%.

Throughout the course of this afternoon, near-term delivery prices (Month-Ahead/Quarter-Ahead) are finding additional support off the back of forecasts of lower temperatures and poor wind outputs into next week (limiting storage injections/increasing the likelihood of storage withdrawals).

In short, Winter is coming!

On the geopolitical side of things, the market awaits updates on the EU’s nineteenth round of sanctions packages levelled at Russia.

Russian drones have breached two NATO countries’ airspace this last week, and the Kremlin looks intent on deepening the conflict – so talk of a ceasefire is non-existent across the news wires.

Trump continues to call on NATO members and the wider-EU to stop buying Russian oil so that sanctions can be put in place.

Coincidentally, over the weekend, Ukraine launched further offensives aimed at disrupting Russia’s oil infrastructure to hamper output.

In other news, energy efficiency initiatives and the development of renewable energy sources is bringing about a drop in Europe’s gas consumption – according to the think-tank, the Institute for Energy Economics and Financial Analysis.

Monthly Day-Ahead averages so far have been at 79p/therm (or 2.7p/kwh exc. non-gas) since the start of the month, and remain so – so, very low volatility persists with the heating season now clearly on the horizon.

ELECTRICITY & CARBON

Today, prices are marginally up (in-line with firmer near-term gas delivery).

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices continue their drift northward.

UKAs continue to observe an upwards trend channel, with the next meaningful resistance level at £59/tn – suffice as to say, speculators have taken Carbon on a bull rally at odds with corresponding gas prices (so increasingly uncorrelated).

As such, renewed political instability (and the likelihood of profit-taking) suggests we’ll see a correction downwards over the coming days (please see divergent relative strength index suggesting trend exhaustion on the chart below).

Monthly Day-Ahead averages for the month so far are at £59/mwh (or 5.9p/kwh exc. non-energy) – on target to be the lowest monthly Day-Ahead average we’ve seen all summer (reflecting good renewables outputs and low demand).