When markets are seemingly quiet and rangebound, often the early clues to underlying sentiment can be found in price-action.

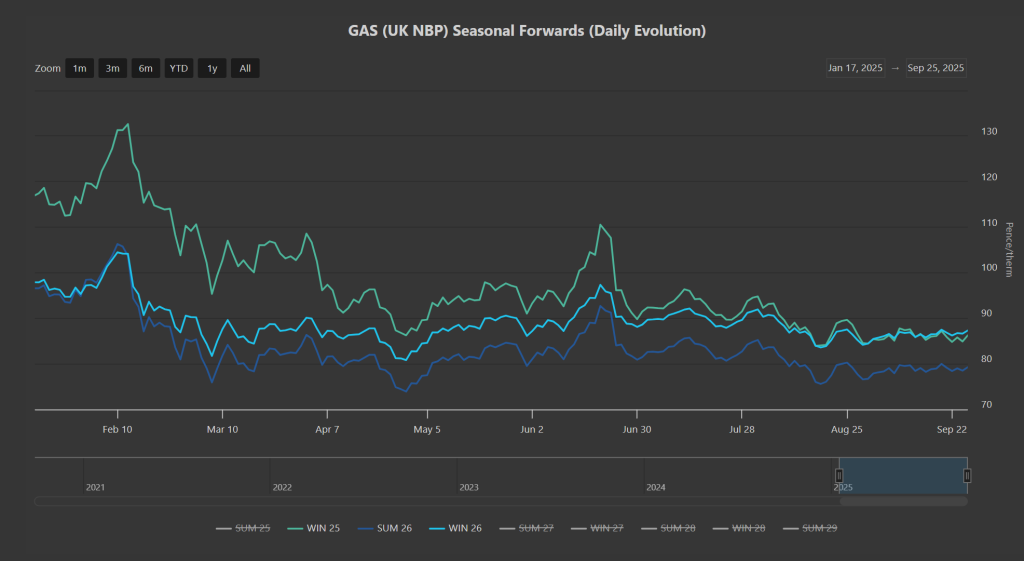

As per the below chart, Winter-26 prices have now consolidated their premium over Winter-25 delivery prices (having crossed above as recently as 2nd Sep) – reflecting lower short-term risk, and favourable conditions in the run up to the heating season.

European storage fullness is at 80% versus the 7-year average of 85% amid 21-day UK weather forecasts detailing a wet, mild start to next month, then wet, windy conditions therafter – none of which should put storage withdrawals under too much pressure.

Winter-25 delivery prices are at a 34% discount versus the high’s posted back in Feb ’25 (again, please see chart below).

For the last 3-months however, Winter-25 delivery prices have traded within a tight 7% range – reflecting low volatility, comparative geopolitical calm, benign weather conditions, and increasingly favourable key fundamental drivers.

The Norwegian scheduled maintenance season will very soon be coming to an end, and has had only limited impact on European storage levels (due to limited withdrawal amid low seasonal demand).

Looking at the bigger picture, our long-range forecast still predicts lowering commodity costs over the coming years – as more and more LNG terminals come online, resulting in an inevitable gas surfeit across Europe and the UK.

Lower commodity costs will come as welcome relief to heavy Industrials, and should offset to some degree the incremental annual increases recently announced to UK non-commodity charges (primarily Nuclear RAB and TNUoS increases).

Looking further afield, M-o-M Asian LNG imports are expected to rise in October – primarily Japan and Korea.

However, China’s declining industrial outputs means demand across North Asia is still down on the year – limiting competition for LNG cargoes.

As trailed last week, the nineteenth package of European Union sanctions against Russia over its full-scale invasion of Ukraine is set to close a loophole allowing Russia to bypass an EU ban for imports of liquefied petroleum gas (LPG) – so the Russia/EU trade relationship continues to deteriorate, and the war of attrition persists (with no sign that Russia’s gas will be headed to Europe anytime soon – more likely China).

Monthly Day-Ahead averages for September remain at 79p/therm (or 2.7p/kwh exc. non-gas), and have been for all but one day of the month so far – further proof, if it were needed, that markets have spent the month meandering sideways.

ELECTRICITY & CARBON

Winter-25 electricity delivery prices remain below those offered for Summer-25 at the culmination of Winter-24 – reflecting a falling market dynamic and improving value.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are teetering on the brink of rolling over into a downtrend (please see chart below).

If the observed rising trend-channel (in blue) breaks to the downside, we could see a retest of £44/tn.

However, we may be seeing the formation of a tight triangle pattern at the top of the range – reflecting a battle between bulls and bears with prices consolidating over the early part of next week before breaking out (most likely to the downside given the bearish divergence on the momentum indicators which we reported last week).

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 43%, thermal at 23% (gas and coal) and low carbon at 19% (nuclear and imports).

Monthly Day-Ahead averages for electricity are at £65/mwh (or 6.5p/kwh exc. non-energy) – so, still on target to be the lowest monthly Day-Ahead average we’ve seen all summer (again reflecting very low short term risk).