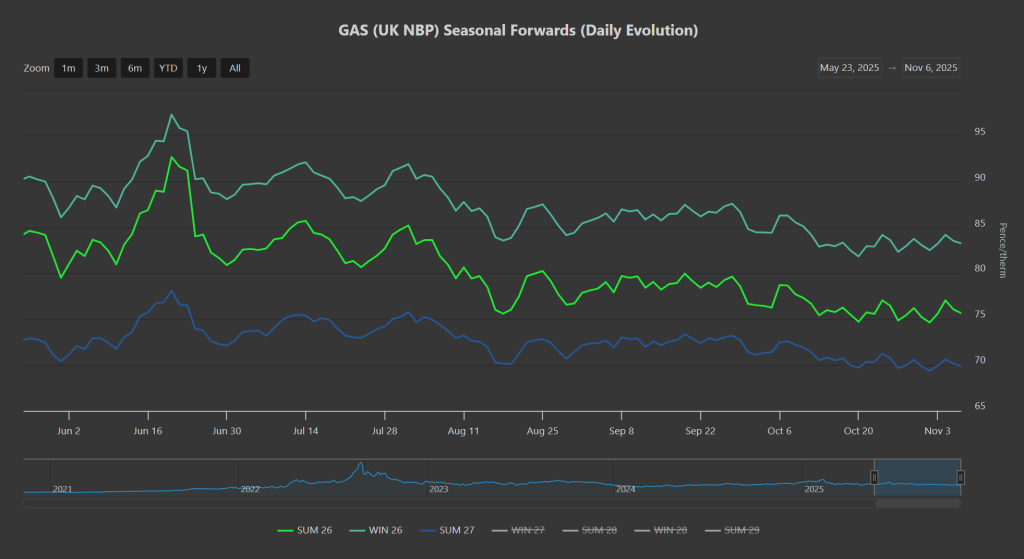

Overcooked fear (about replenishing European gas storage in time for the Winter-25 heating season), peaked in Jun ’25 (please see chart below), but abated thereafter once it became clear that supply/demand dynamics would support sufficient storage injections throughout Summer-25.

Since the Jun ’25 highs, the front 3-Seasons (Summer-26/Winter-26/Summer-27) have traded within a tight 12% range.

Since Winter-25 began on 1st Oct’25, the front 3-Seasons have all traded sideways in a 3.5% range – reflecting a very balanced market, and an underlying confidence amongst market participants that European storage fullness (now at 83% versus the 7-year average at 89%) should be enough to get us through the heating season without too many problems.

On the weather side of things, temperatures are forecast to remain above seasonal norms over the coming weeks, delaying the bullish impacts of the heating season.

On the supply side, plentiful LNG arrivals and send-out, coupled with Norwegian pipeline flows comfortably above the 10-day moving average, are also helping to keep the winter bulls at bay.

Notably, the European LNG imports 30-day moving average has been at was at 230k tonnes per day this week – 54% higher than the five-year seasonal average!

As cited in previous bulletins, this “glut” of LNG into Europe can be attributed to new facilities (Russia’s Arctic 2 terminal and LNG Canada) servicing Asia’s requirement more specifically, whilst US supply is all but bound for Europe/the UK – so additional capacity is easing global supply/demand pressures as well as mitigating any bidding wars for cargoes (keeping price low).

Monthly Day-Ahead averages for November so far are at 75p/therm (or 2.56p/kwh exc. non-gas).

The heating season will undoubtedly arrive eventually, though speaking personally, we still have cosmos blooming in the garden!

As such, and given mid-range weather forecasts, it’s anyone’s guess when the heating season will begin in earnest (making for a shorter withdrawal period, another bearish driver).

ELECTRICITY & CARBON

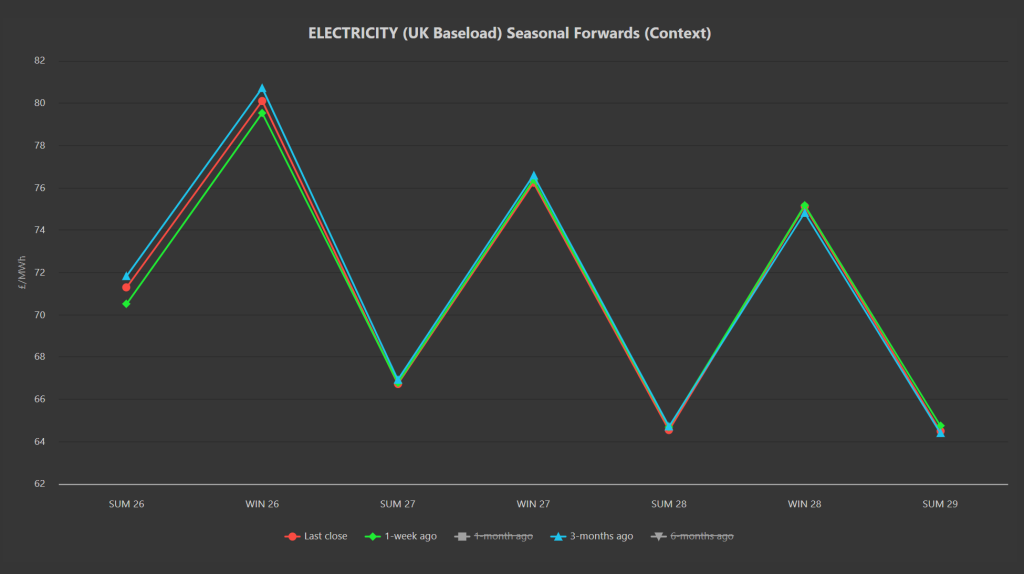

Electricity prices are mirroring gas moves.

Looking at the chart below then, we’ve removed the 1-month ago and 6-months ago lines revealing how Seasonal Forwards 3-months ago are all but identical to Last Close and/or 1-month ago.

This reflects of course how stable electricity Forward prices have been since mid-summer.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Whilst UKAs are retracing back to £55/tn following Monday’s speculative bull rally, they’re doing so at quite a clip – reflecting the reality that whilst speculators can drive the market up, it’s difficult for them to keep it there.

Today’s UK electricity generation mix is bullish in nature given patchy wind outputs – specifically, renewables are contributing 21%, thermal at 48% (gas and coal) and low carbon at 18% (nuclear and imports).

Monthly Day-Ahead averages for November so far are at £68/mwh (or 6.8p/kwh exc. non-energy).