Supply is strong (LNG and Norwegian pipeline flows); demand remains sluggish and below seasonal norms; temperatures are above seasonal norms; renewables are strong (meaning gas-for-power burn is mitigated, as are storage withdrawals); and market-moving headlines are few and far between.

As such, prices for both near and far-term delivery continue to meander down.

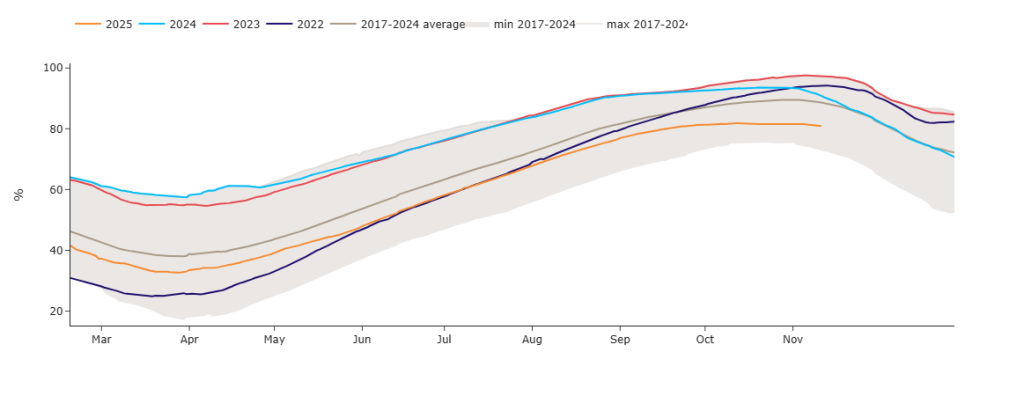

As per the chart below, whilst storage numbers are still 8% below the 7-year average (and below where they were in ’22/’23/’24), they’re nonetheless holding steady and yet to roll-over (reflecting a delay in the onset of the heating season).

As was the case in ’22 & ’23, the heating season can begin as late as the first week of December.

Right now, temperatures are forecast to fall below seasonal norms next week, but should be back up above seasonal norms to end the month – as such, it would seem likely that a condition of net storage withdrawal will not kick-in until December this year, too.

Notably, looking to Europe (and specifically the largest gas market, TTF), the fall of CAL26 (calendar year prices) below the €30/mwh level yesterday is surely a very big bearish signpost of the impact of a burgeoning glut of LNG supplies (as the world adapts to the absence of Russian flows into Europe).

This “glut” of LNG into Europe is of course attributed in part to new facilities (Russia’s Arctic 2 terminal and LNG Canada) servicing Asia’s requirement more specifically, whilst US supply is all but bound for Europe/the UK – so additional capacity is easing global supply/demand pressures as well as mitigating any bidding wars for cargoes (keeping price low).

Meanwhile, Asian demand is patchy and cargoes make more money heading to Europe.

Monthly Day-Ahead averages for November so far are at 73.8p/therm (or 2.52p/kwh exc. non-gas).

In other news, further to last Friday’s commentary, several clients have asked how my cosmos in the garden is getting on – I’m pleased to confirm it’s still blooming (reflecting a mild start to Winter-25)!

ELECTRICITY & CARBON

Electricity Seasonal Forwards remain down on the week, and the month.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

We predicted back on 5th Nov that UKAs would fall back to around £55/tn, then bounce (at the trend channel base) – however, we’d not expected that prices would fall back to the trend channel quite so steeply, nor bounce off it quite so acutely.

Instead, we’d expected a meander downwards pending the UKA Auction on Wednesday – however, what we’ve actually seen is an immediate bounce with no let-up since (reflective of increasing speculative positioning).

However, the trend is now presenting bearish momentum divergence and has run out of steam (please see chart below) – £55.50/tn is now a viable downside target.

Today’s UK electricity generation mix is bearish in nature given patchy wind outputs – specifically, renewables are contributing 52%, thermal at 21% (gas and coal) and low carbon at 17% (nuclear and imports).

Monthly Day-Ahead averages for November so far are at £70/mwh (or 7p/kwh exc. non-energy).